Housing Market Index

Are you a builder interested in being part of the HMI panel of respondents?

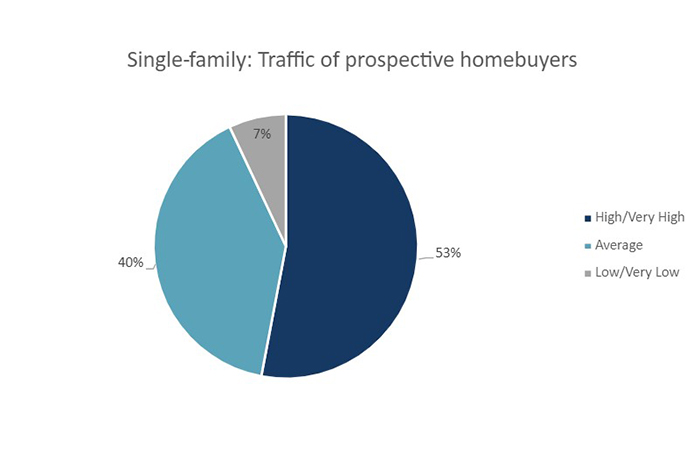

Single-Family

(includes single detached homes, semi-detached homes and row (townhouse) homes)

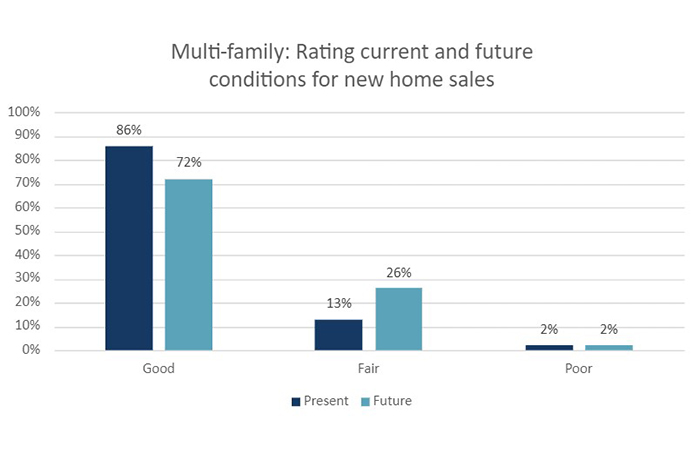

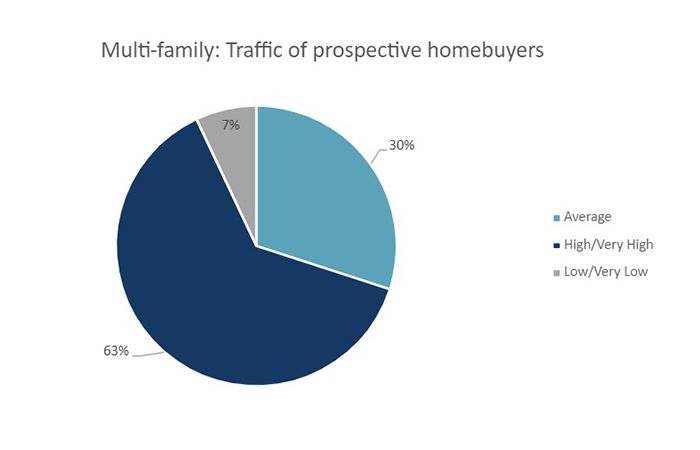

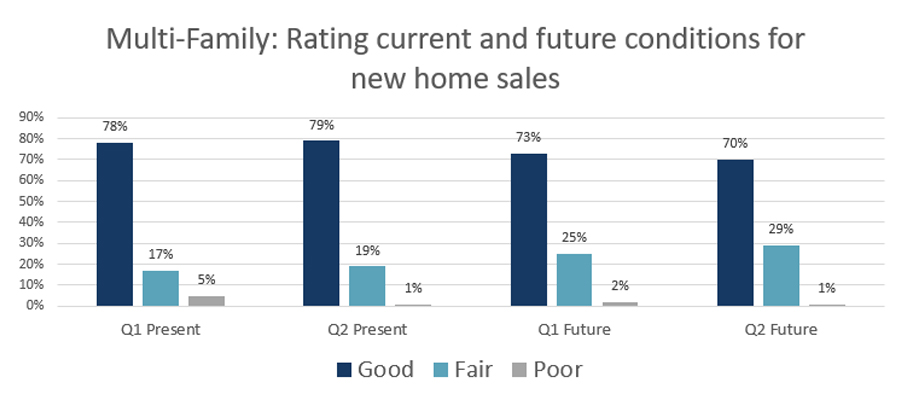

Multi-Family

(includes stacked townhouses, duplexes, triplexes, double duplexes and row duplexes, and low and high-rise apartment buildings)

Properties of the HMI

(i.e. how to read the number)

- The HMI is on a scale of 0 to 100

- It's 0 only when everyone says conditions are "poor"

- It's 100 only when everyone says conditions are "good"

- It's 50 when the % saying "good" = the % saying "poor"

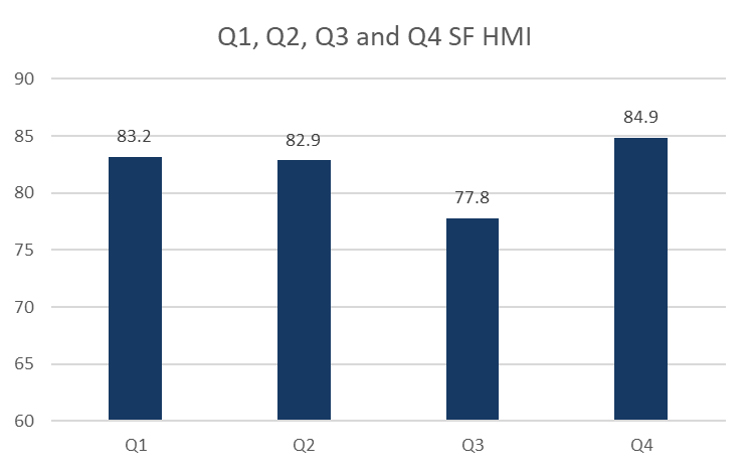

2025 Q1 HMI

This page outlines the Q1 2025 results of CHBA’s Housing Market Index (HMI). This informative research and economics product provides a much-needed leading indicator about the current and future health of the residential construction industry in Canada with respect to housing units for ownership (freehold or condominium). The HMI is a sentiment indicator, assessing current selling conditions, expectations for selling conditions over the next six months, and the level of sales office traffic (or other measures of prospective buyer interest), and as such is a proven indicator of housing starts that can be expected in six months and beyond.

The data for the CHBA HMI comes from a panel of CHBA homebuilders and developers from coast to coast. Every quarter, this panel – created in collaboration with our local and provincial home builders’ associations across Canada – responds to a series of questions about market conditions. CHBA then uses proprietary statistical analysis to prepare the quarterly HMI. In addition to the standard HMI questions, each quarter CHBA asks “special questions” that allow the Association to gather data and insights into current issues affecting the industry across the country.

CHBA’s HMI was modelled on the National Association of Home Builders’ (NAHB) very successful and influential US version. The NAHB version is used regularly by financial analysts, the Federal Reserve, policymakers, economic analysts, and the news media, given the importance of the health of the residential construction industry to the overall economy. Through the CHBA HMI, CHBA has done the same for Canada, where it is being used and followed by similar Canadian agencies (e.g. Bank of Canada, Statistics Canada), government policymakers, economists/analysts and media.

If you have any questions or feedback about the CHBA HMI, please contact hmi@chba.ca.

Summary for Q1 2025 HMI

Tariffs, Uncertainty and Sticky-High Mortgage Rates Keep Buyers Sidelined

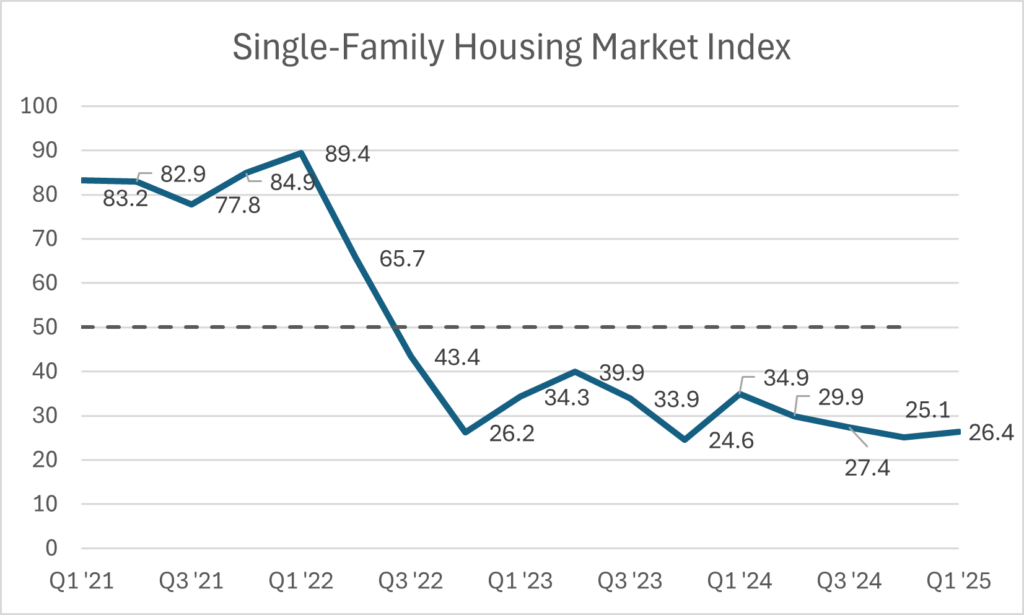

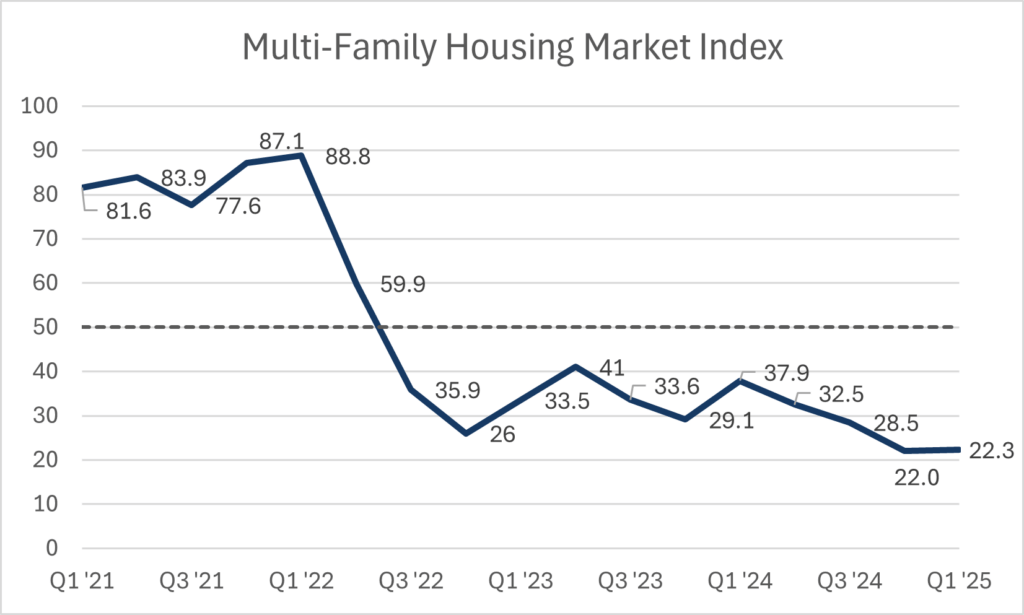

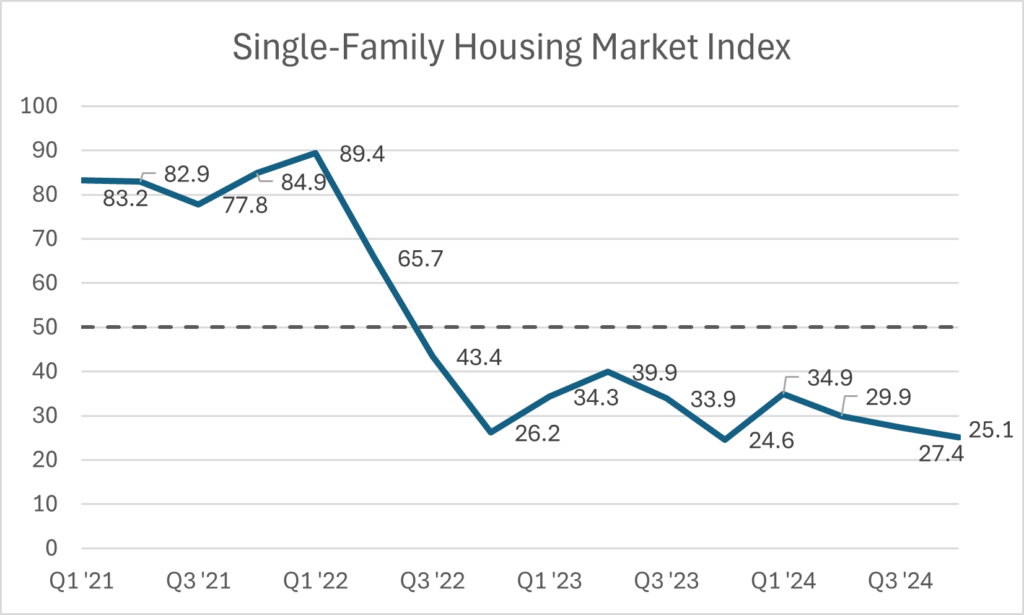

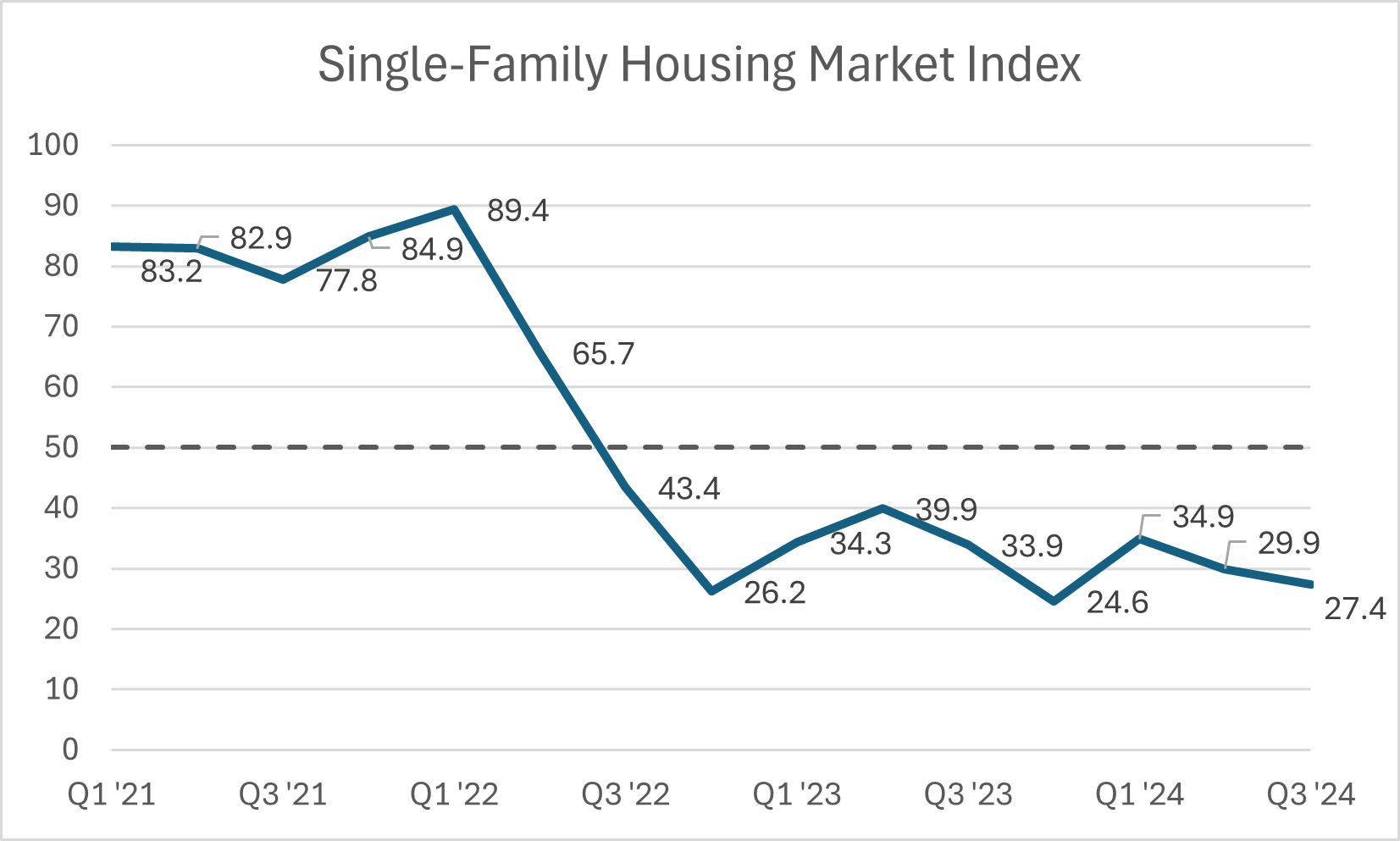

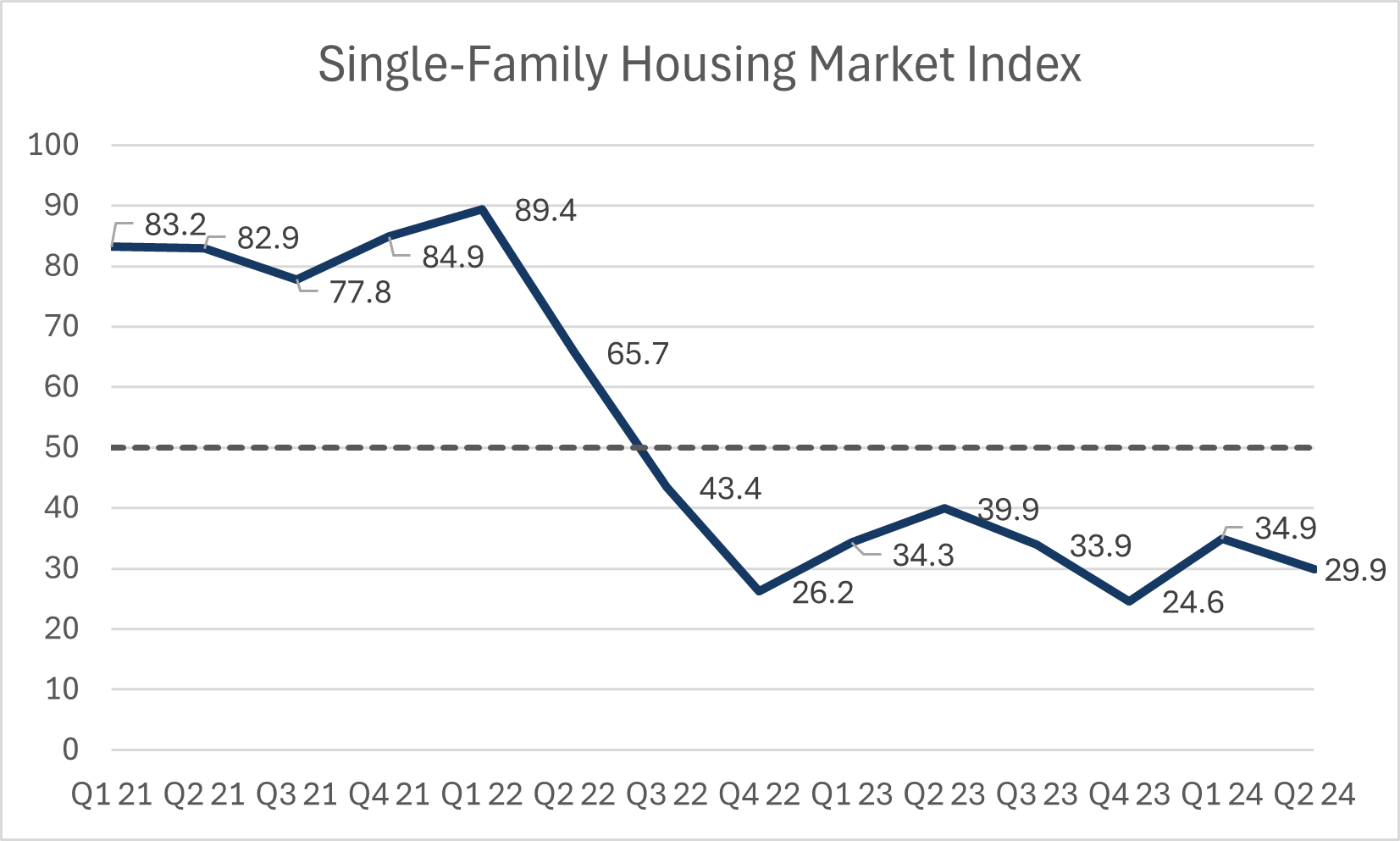

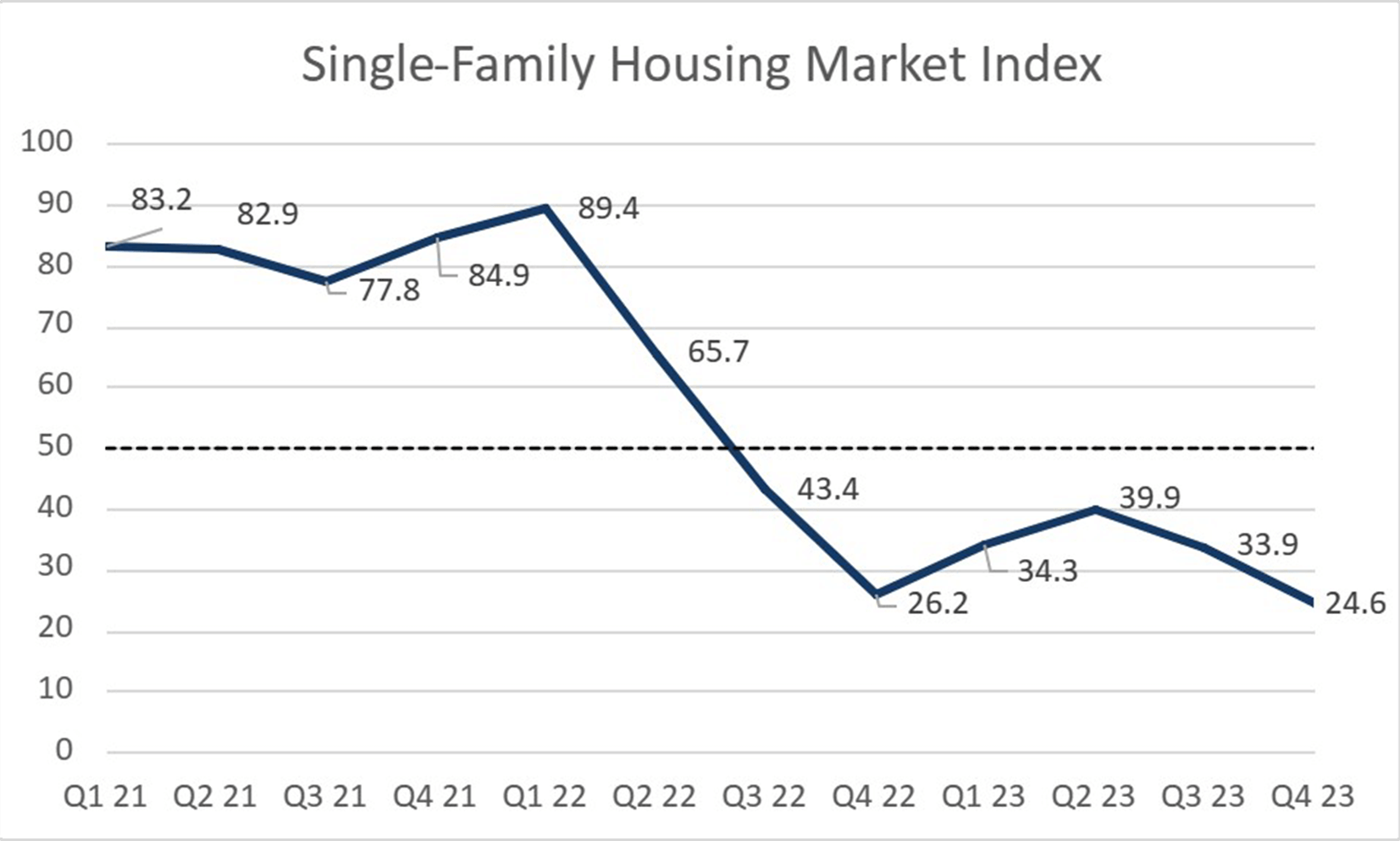

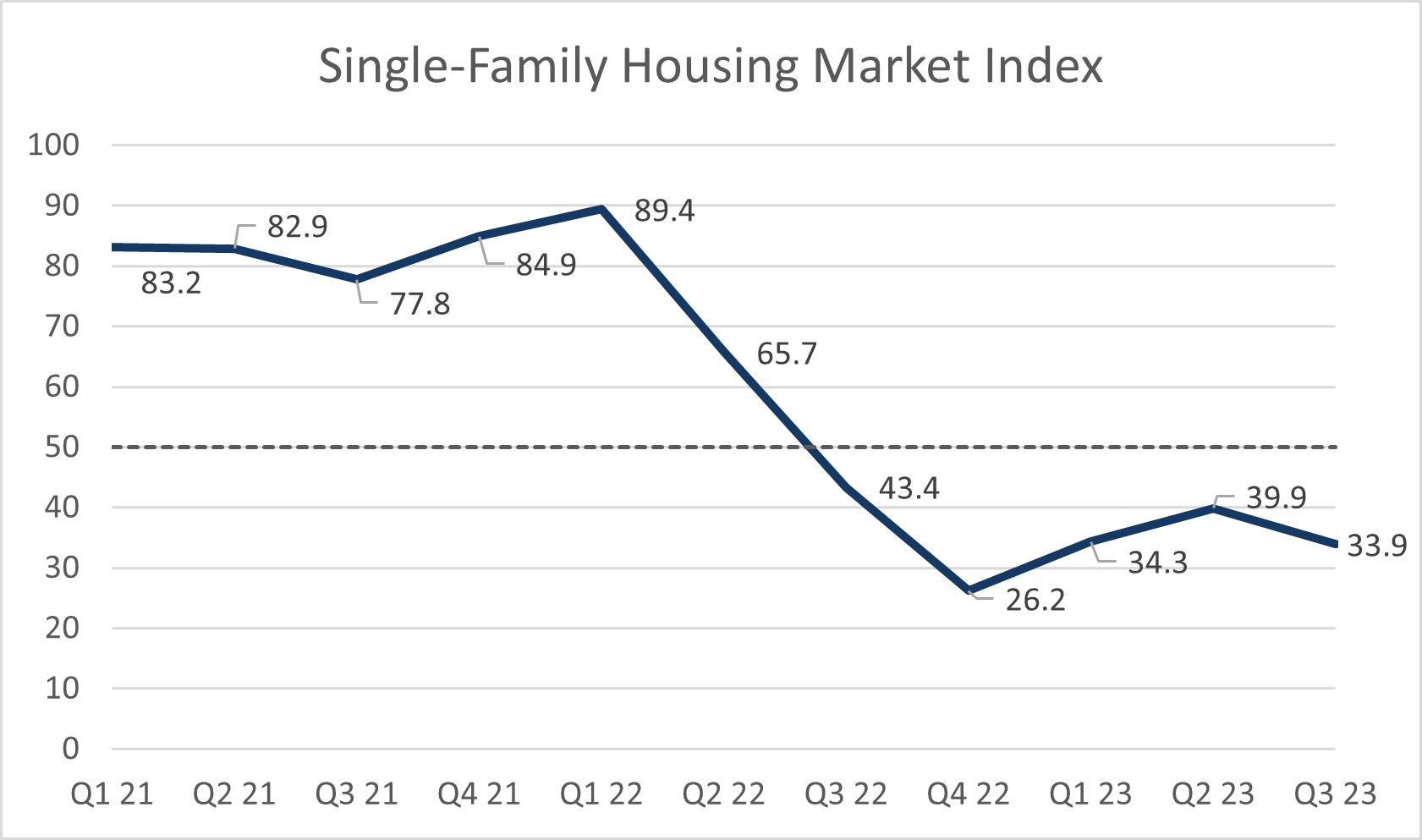

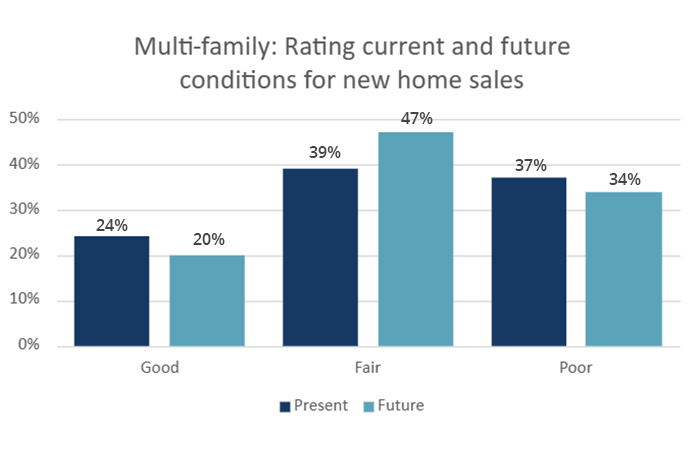

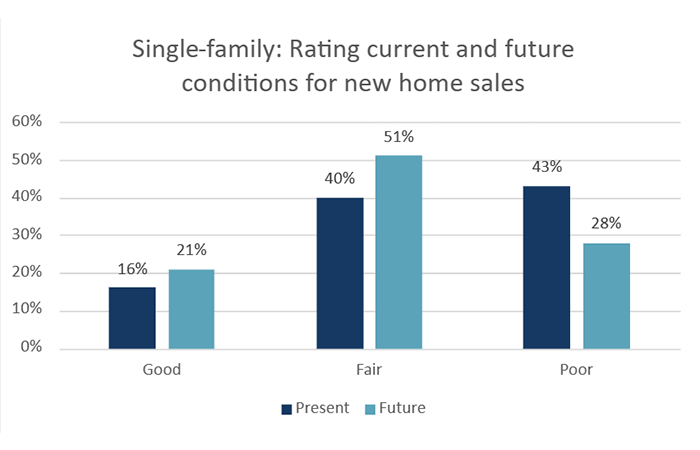

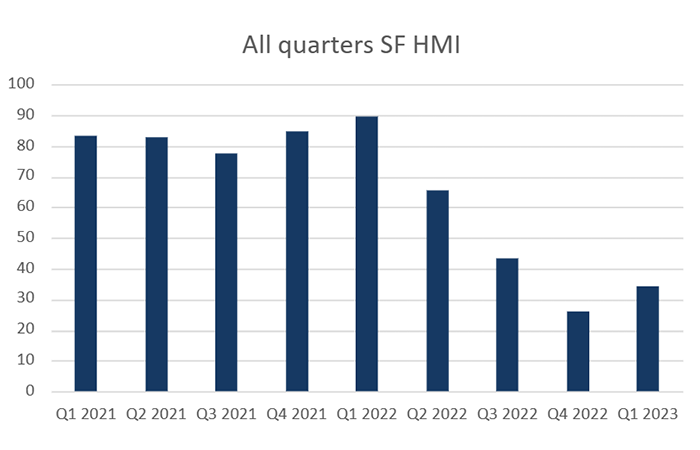

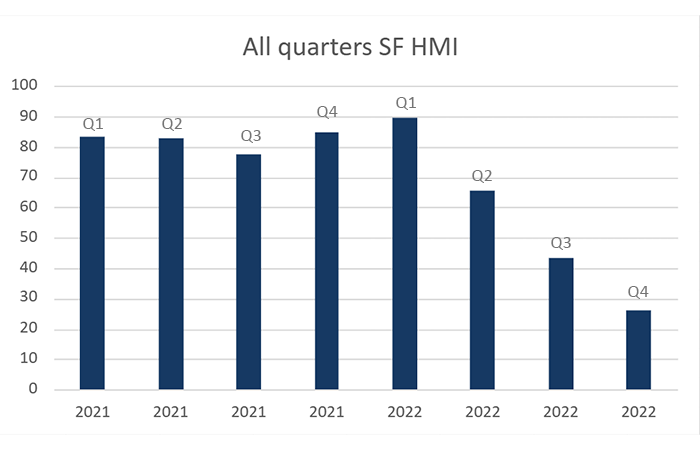

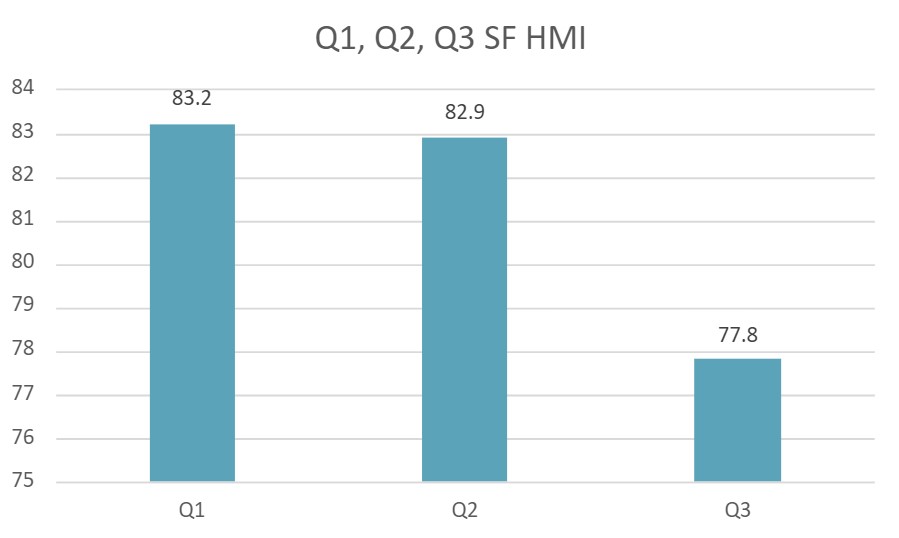

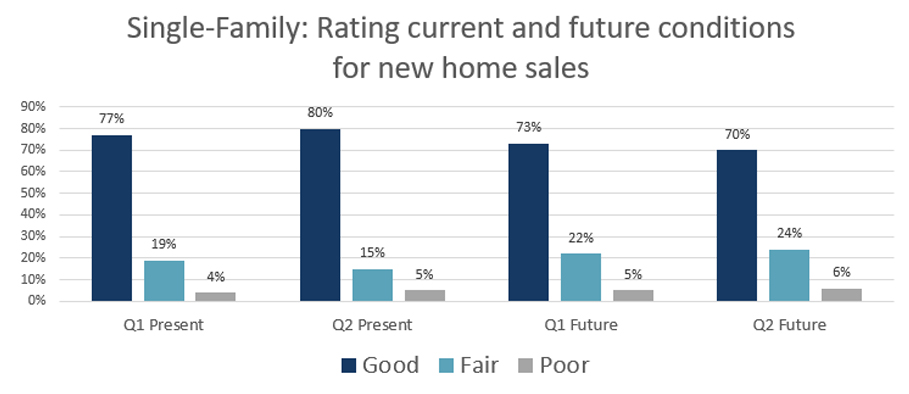

Both the single-family and multi-family Housing Market Index (HMI) once again reflected overtly pessimistic builder confidence in relation to new home sales during the start of 2025. CHBA’s single-family HMI was 26.4 for Q1 2025. This score remains close to the index’s record low of 24.6 in Q4 2023 and down 8.5 points from the score in from the same time last year. The multi-family HMI was 22.3, which remains essentially at its record low score of 22.0 from Q4 2024. Both the single- and multi-family index were held down by builders’ expectations for future sales conditions this quarter. Over the past two years, builders’ expectations tended to be higher than the measure of current sales sentiment. However, over 50% of both single and multi-family builders rated their expectations for future sales as Poor—the first quarter this has happened.

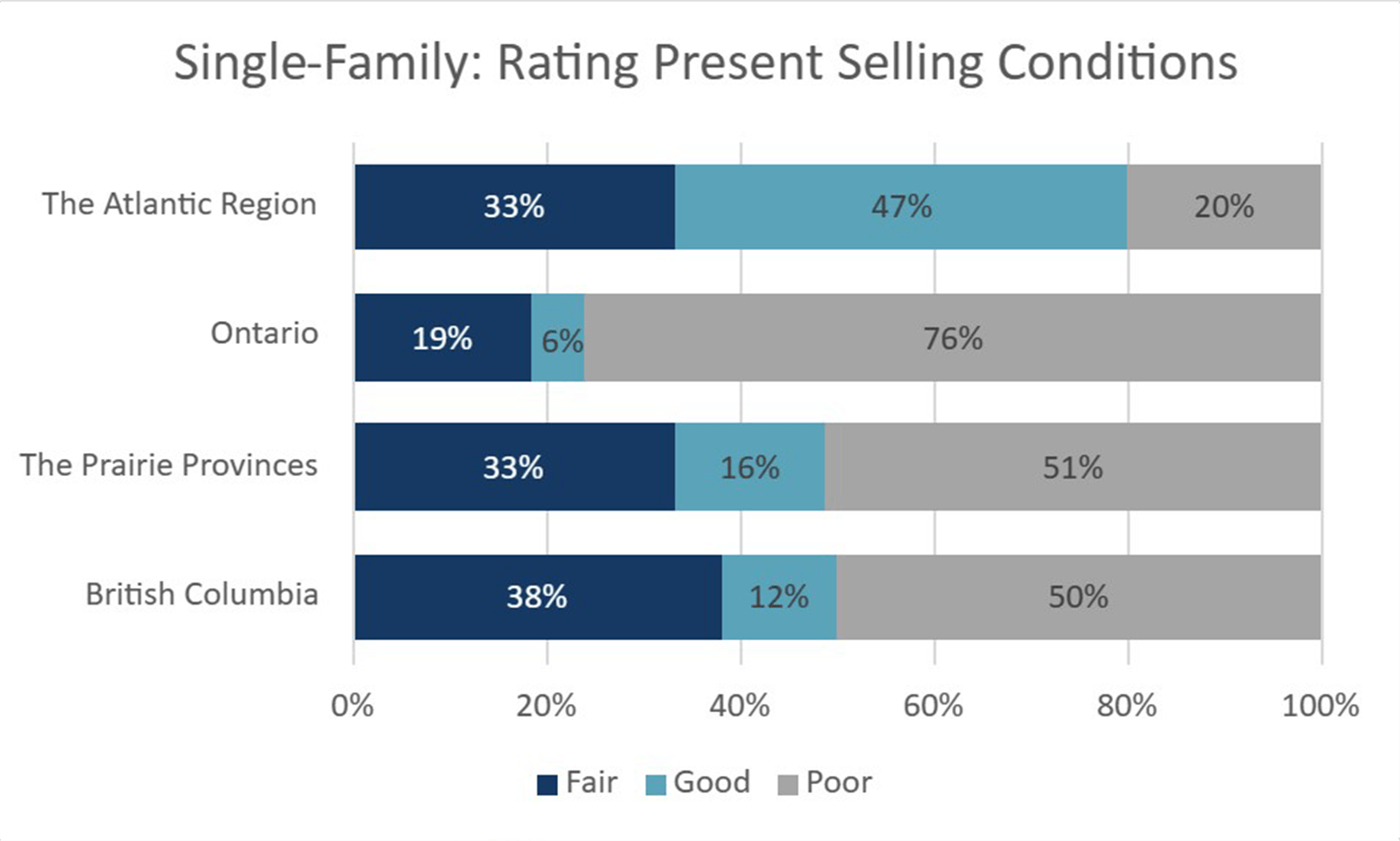

Regional differences in builder sentiment, highlighted in results from past quarters, largely continued in early 2025. Both single- and multi-family scores in Ontario were in the single digits and at record lows, as the worsening expectations for future sales drove both indices down from the previous quarter. With the single-family HMI at 7.4 and the multi-family HMI at dismal 2.9, the future looks incredibly grim for starts in Ontario in the year ahead and beyond. Sentiment in British Columbia avoided declining further but remained at an abysmal level of 17.2 for single-family sales and 24.8 for multi-family sales. Providing uplift to the national index was the neutral score of 49.0 for single-family sales in the Prairie Provinces and moderately strong HMI scores in the 60s for multi-family sales in the Prairie Provinces and for single-family sales in the Atlantic Provinces.

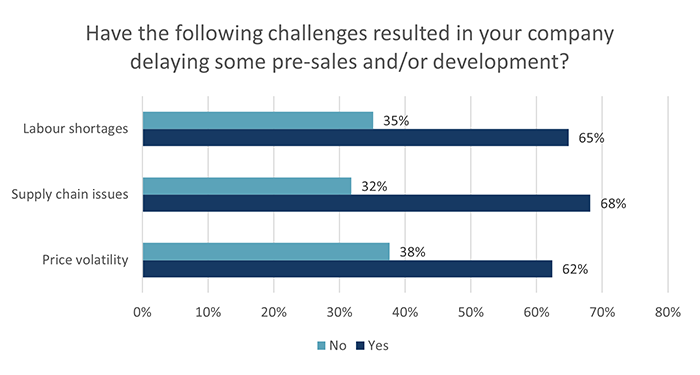

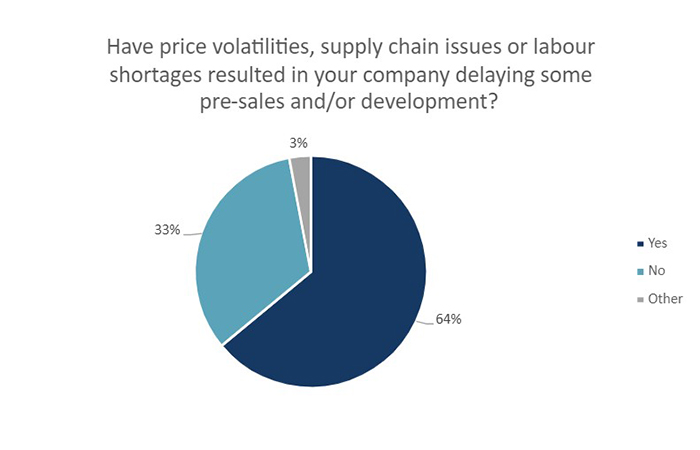

The escalating trade war threatens residential construction through both higher material prices and lower consumer demand. Despite the uncertainty and rapid changes in tariff threats and implementation, builders were asked about their exposure to U.S. imports as the survey was in field throughout March to early April. A 71% majority of builders said they had already received supplier notification of price increases. At the same time, 75% of builders estimated that American made materials constitute less than 30% of the total value of building materials per unit built.

While industry exposure to current and future counter tariffs is not extreme, the current total cost of construction is already above what many consumers can bear. Longstanding tariffs on a wide range of U.S. building material imports would be a huge setback to achieving housing affordability targets. And the even bigger concern is the impact of the market uncertainty that is keeping buyers on the sidelines and is reflected in the HMI scores. Additional results related to builders’ tariff exposure can be found in the special questions section below.

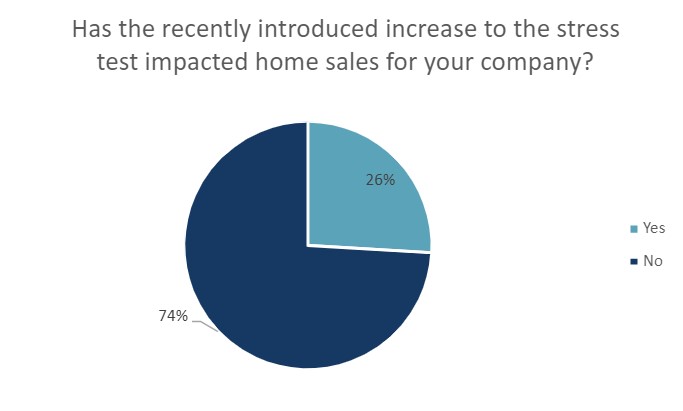

The continued negative sales conditions in Ontario and British Columbia place significant downward pressure on future housing starts intended for ownership and make it difficult to make progress on national housing affordability. Despite two additional rate cuts from the Bank of Canada in the first quarter, there has been limited material change to fixed mortgage rates, given the ongoing higher yields still prevalent in the bond market. Therefore, higher mortgage rates, compounded by the ongoing excessive stress test, are still supressing demand, as hard and soft construction costs continue to rise.

The pessimistic results of the HMI in recent quarters are also playing out as expected by CMHC’s housing starts data. Starts in areas with at least 10,000 population in the first quarter of 2025 fell 9% year over year nationally to 45,302 units, with the regional starts consistent with the HMI’s findings. Ontario saw the largest contraction, declining 38% over this time last year, falling 6,722 units, with Toronto falling 65% year-over-year for March. The decline in British Columbia was 30% or 3,234 units, with Vancouver falling 59% year-over-year for March. Atlantic Canada saw milder decline of 14% or 417 units. Prairies managed to a strong 24% increase or 2,727 units. These housing starts largely reflect sales conditions over the past three years or more, particularly of the multi-family high rises.

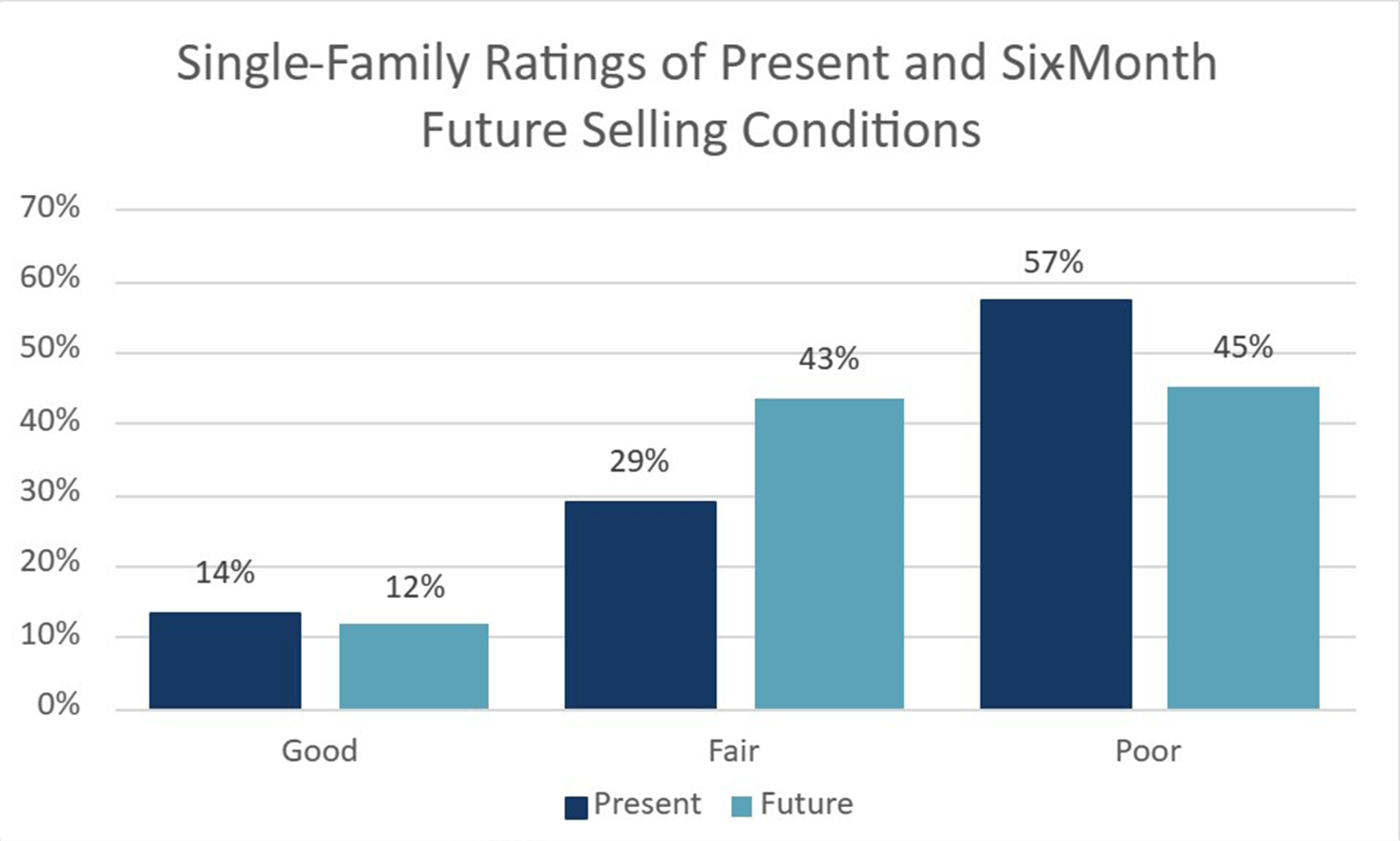

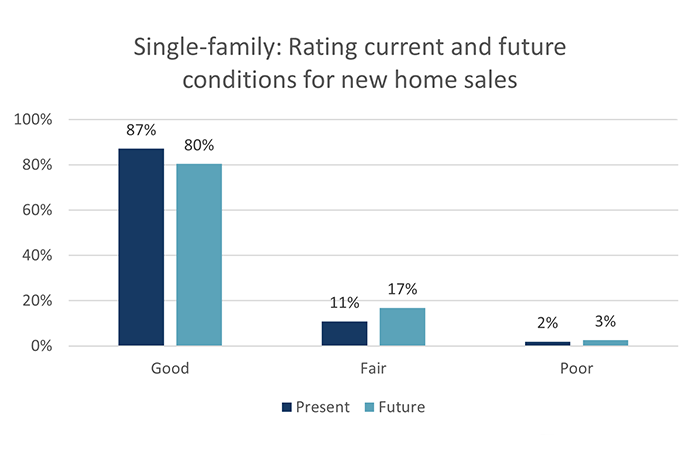

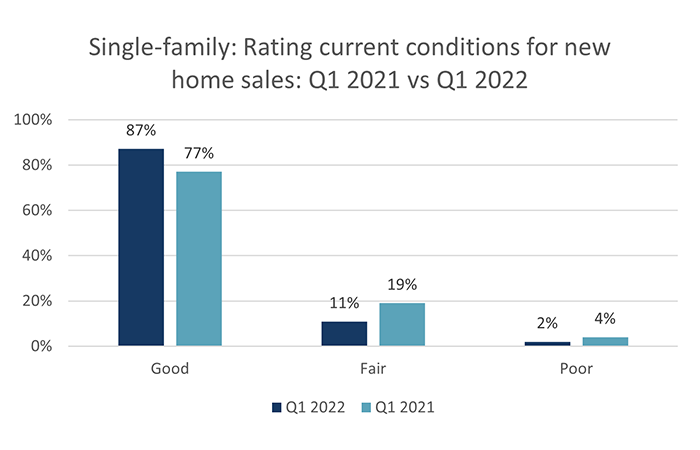

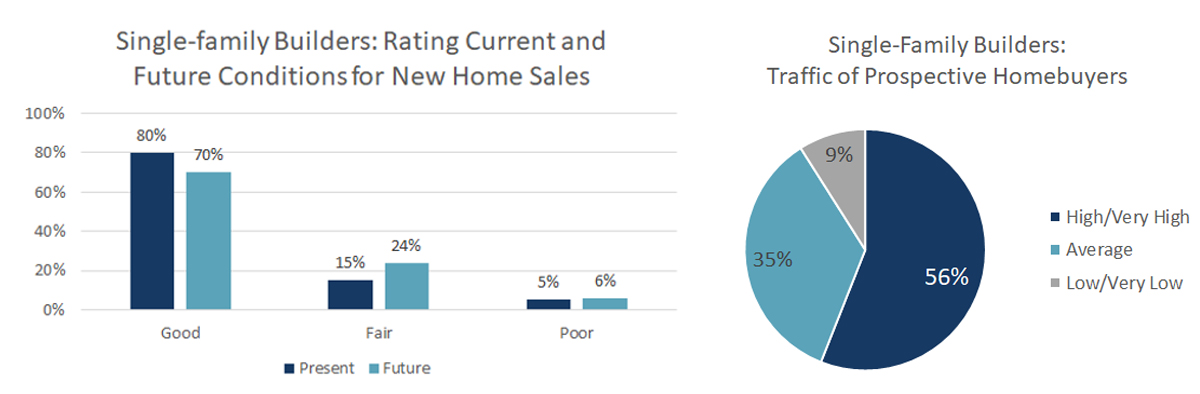

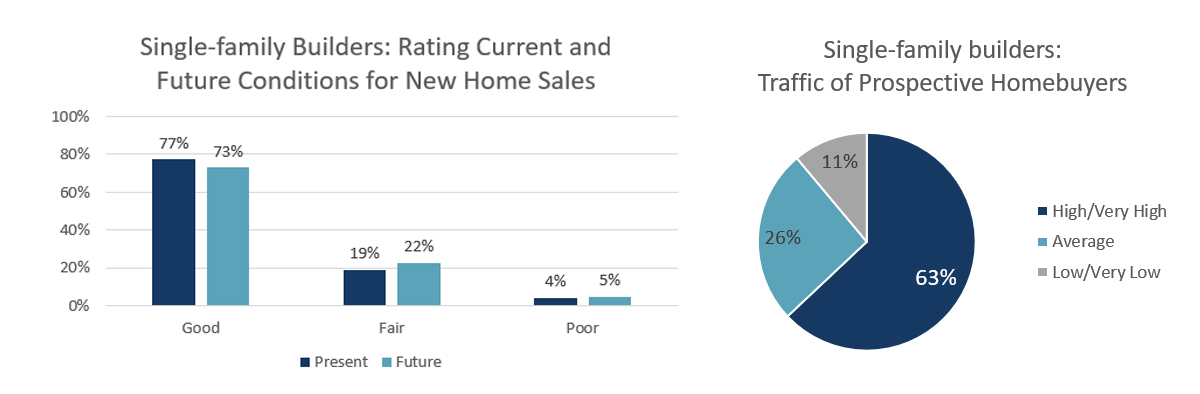

- Single-family builder confidence was 26.4 in the first three months of 2025. This is a small increase of 1.3 points over Q4 2024, but a decline of 8.5 points from the same quarter in 2024 and represents sentiment still within touching distance of the index’s all time low of 24.6 points recorded in Q4 2023—before the Bank of Canada started to lower rates.

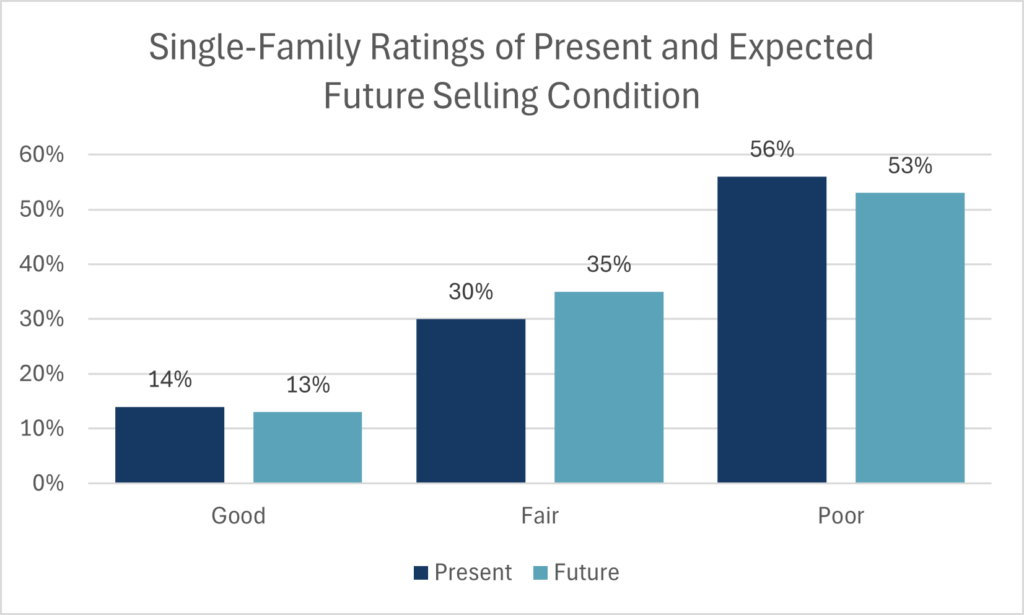

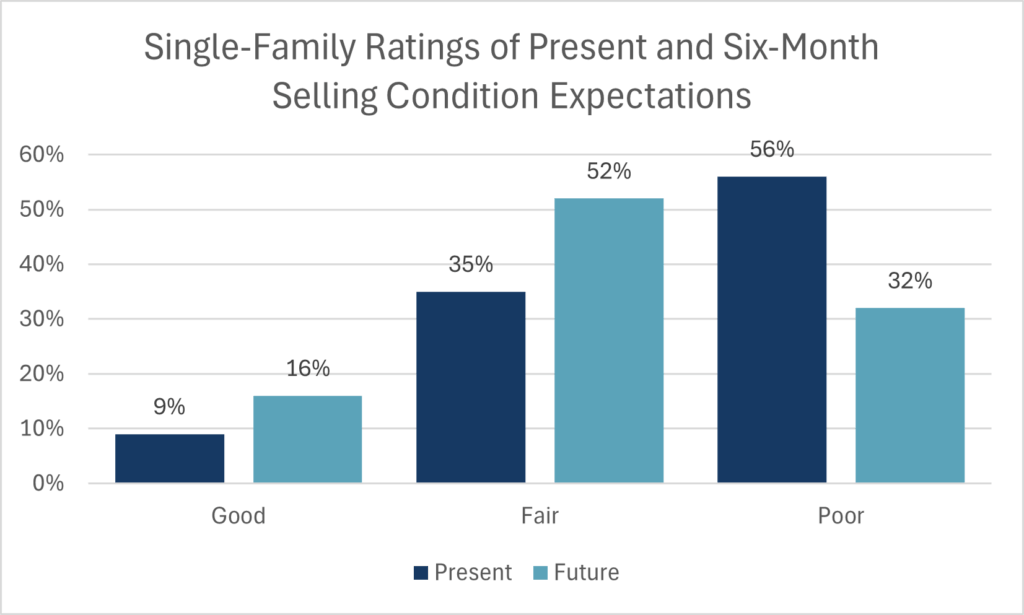

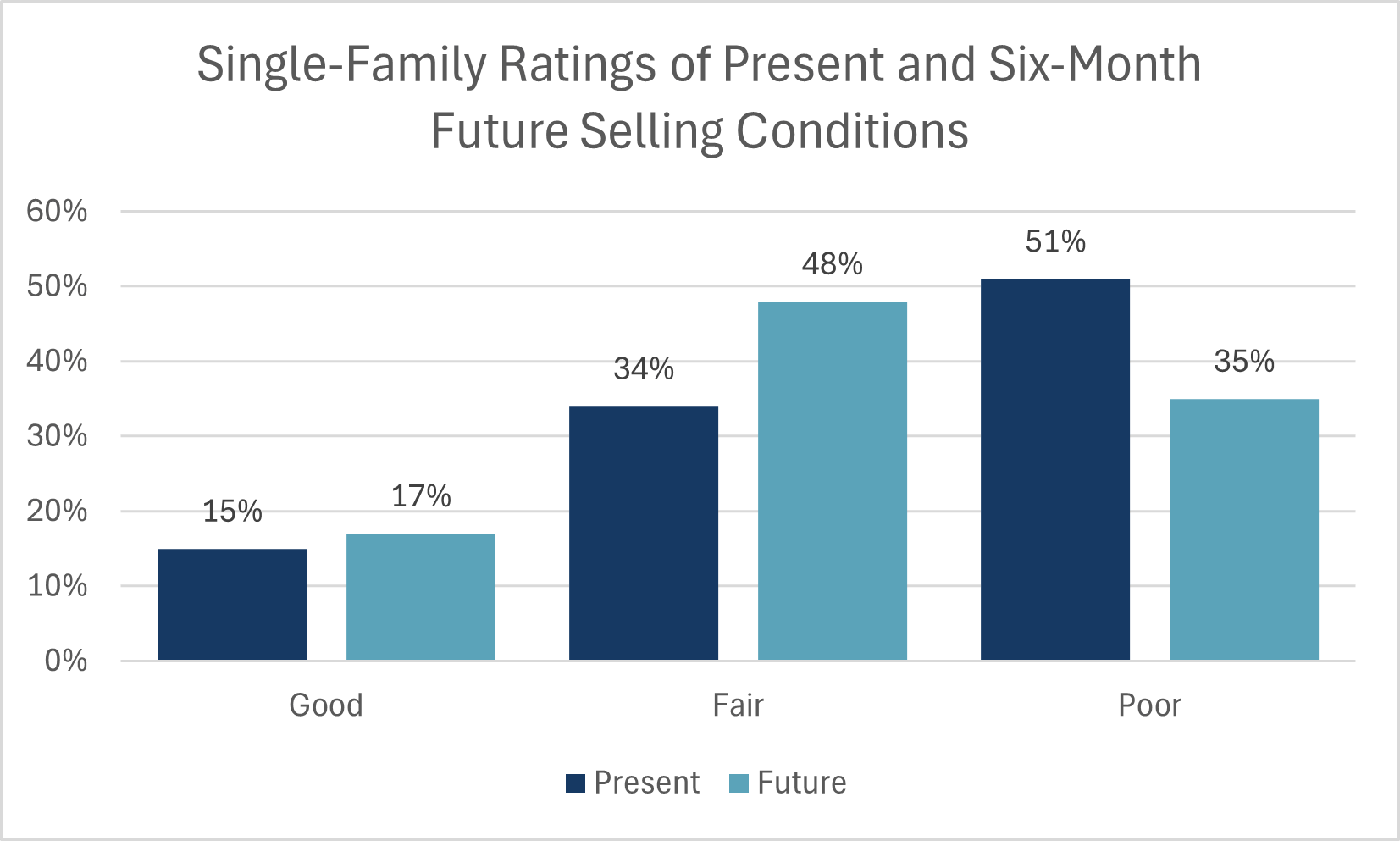

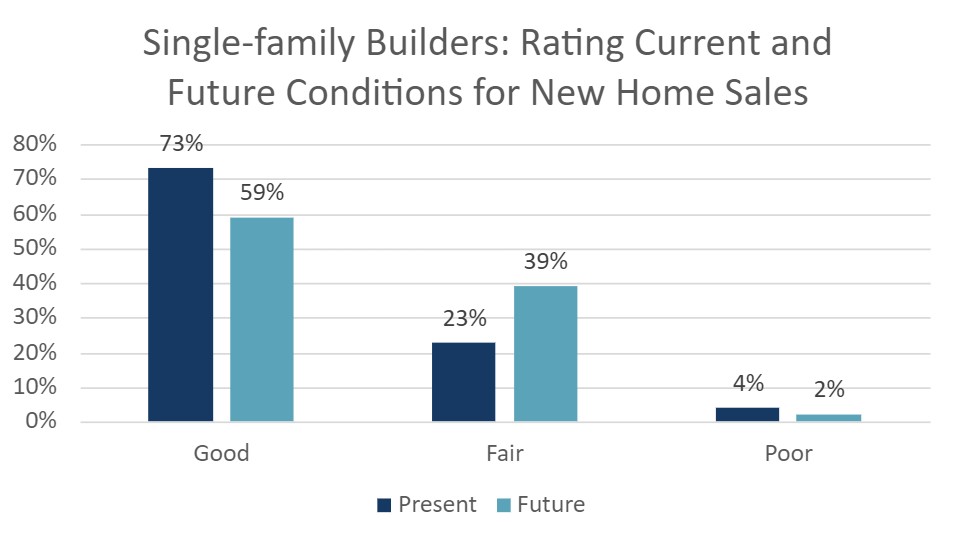

- 56% of builders rated present selling conditions as Poor. The majority of single-family builders have given a rating of Poor in five of the past six quarters.

- Likely related to the tariff situation, 53% expected future sales to be Poor. Since the start of 2023, builders have been hopeful that sales would improve to more normal conditions, however, this is no longer the case.

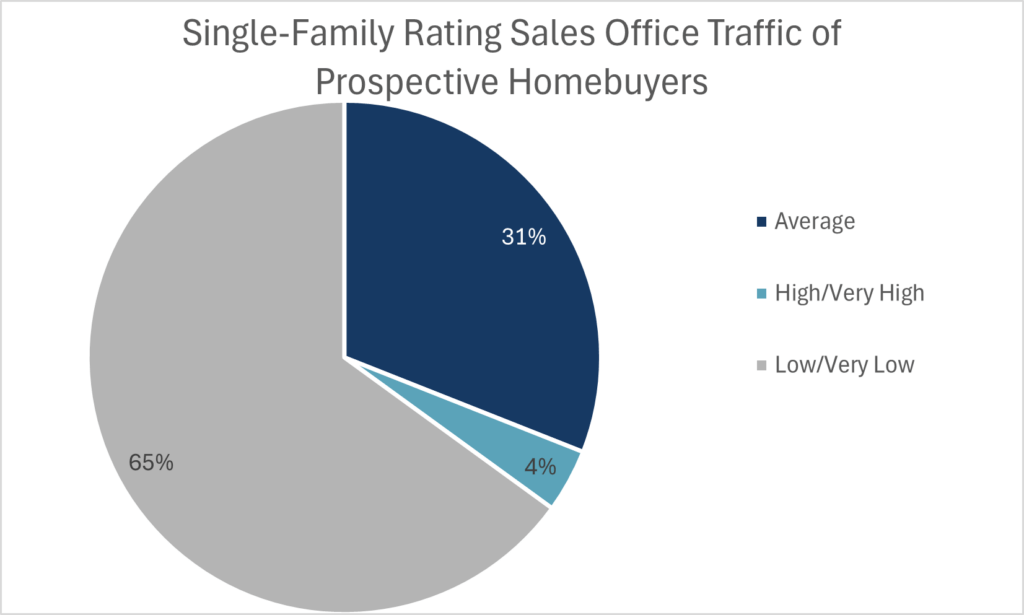

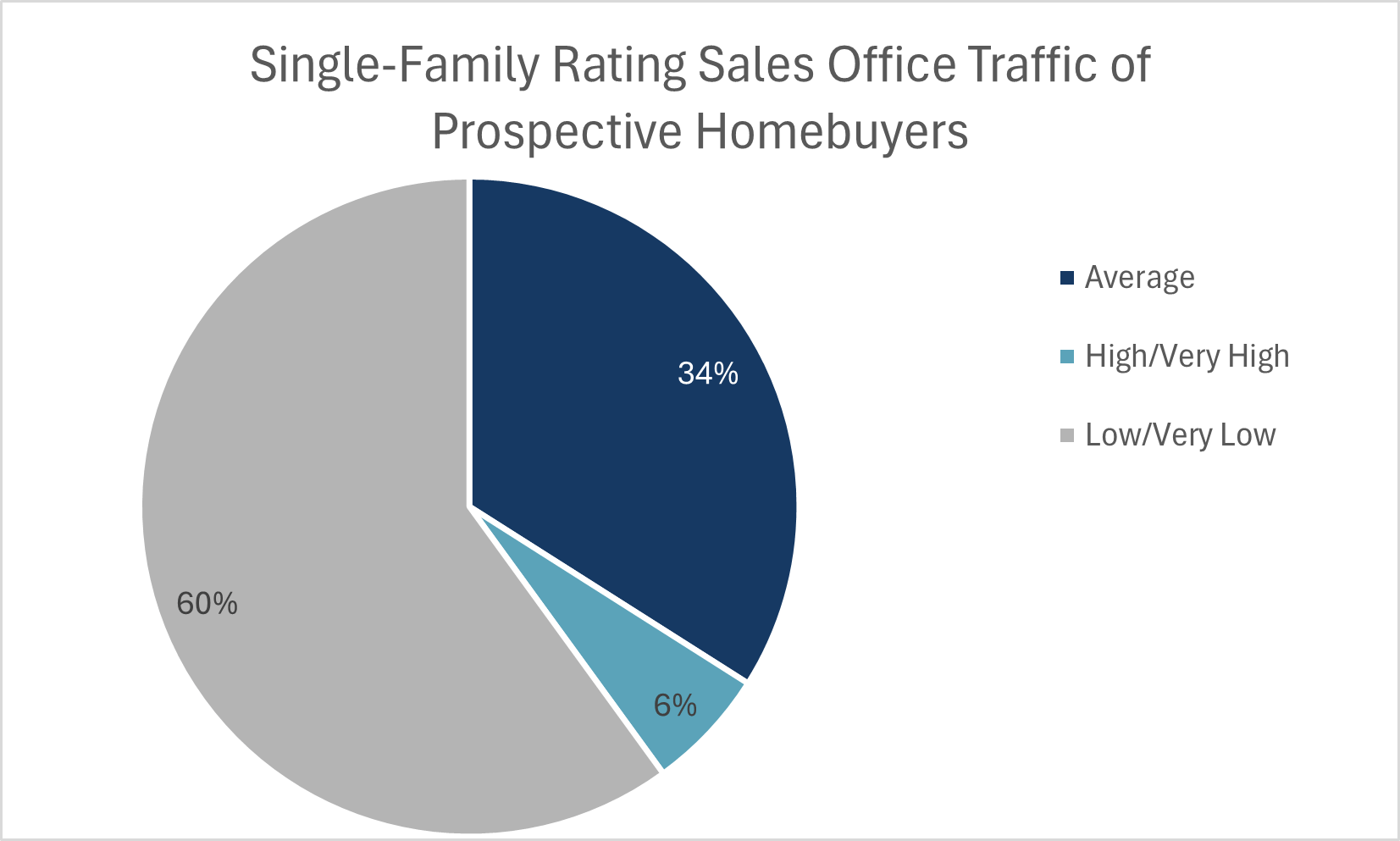

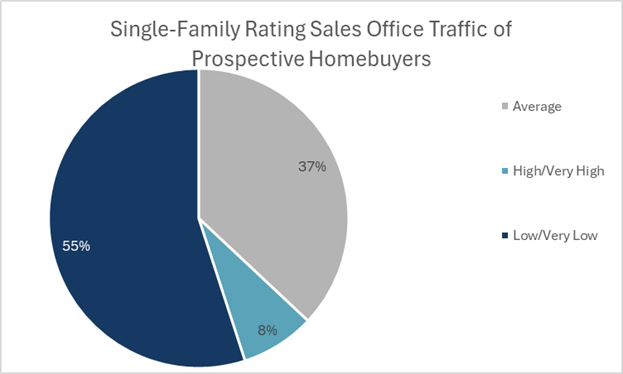

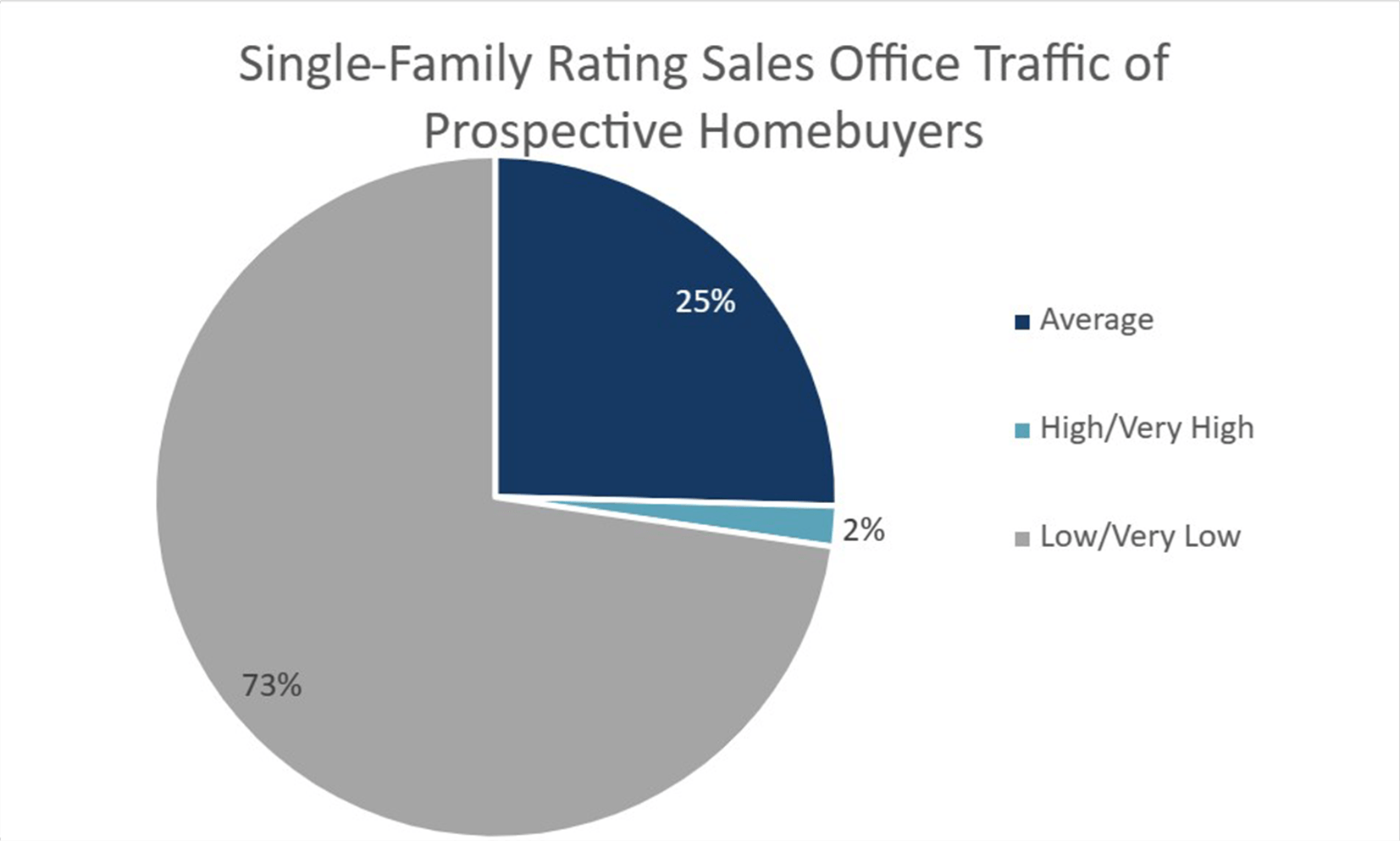

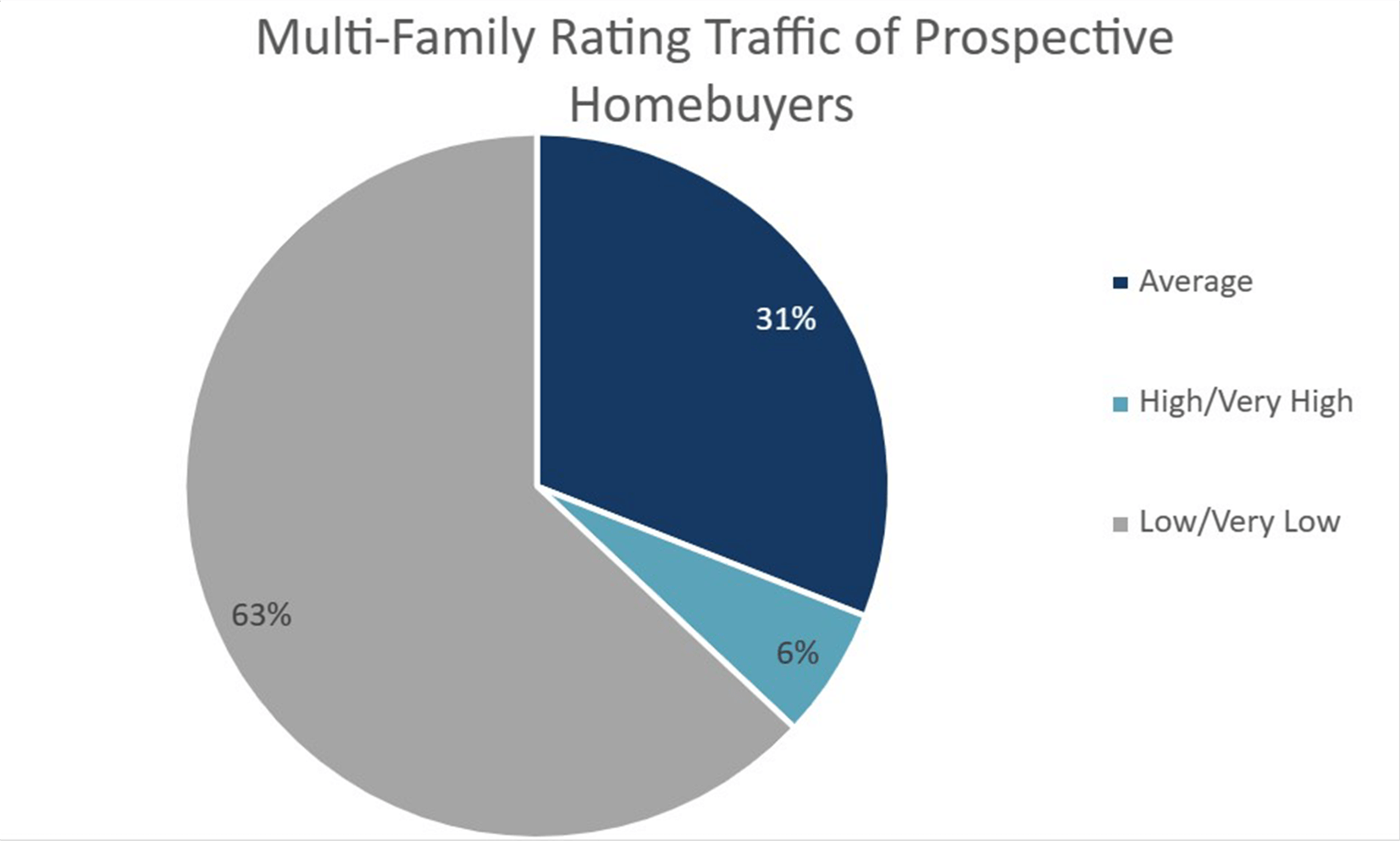

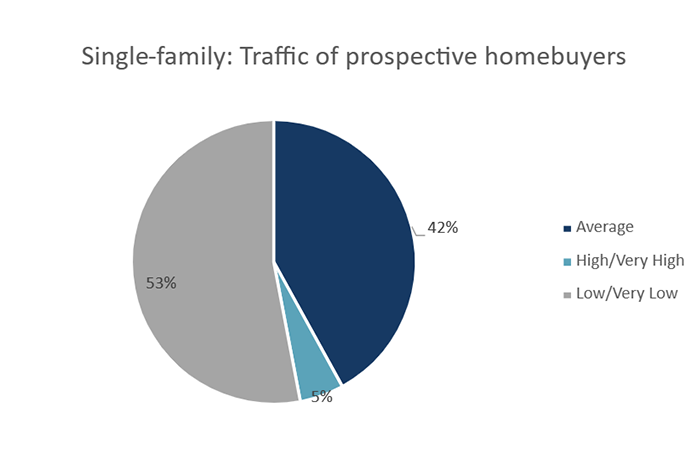

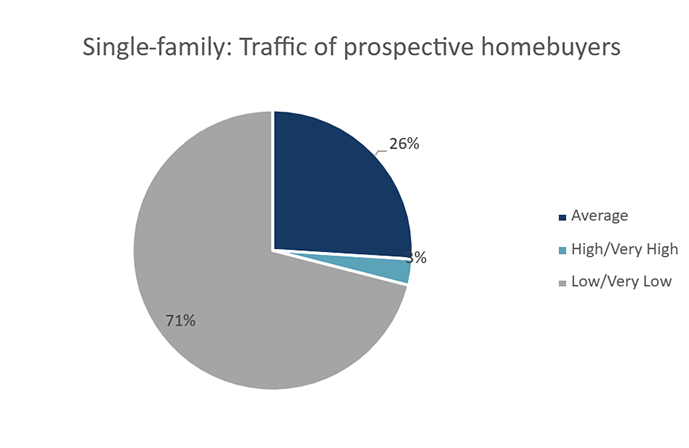

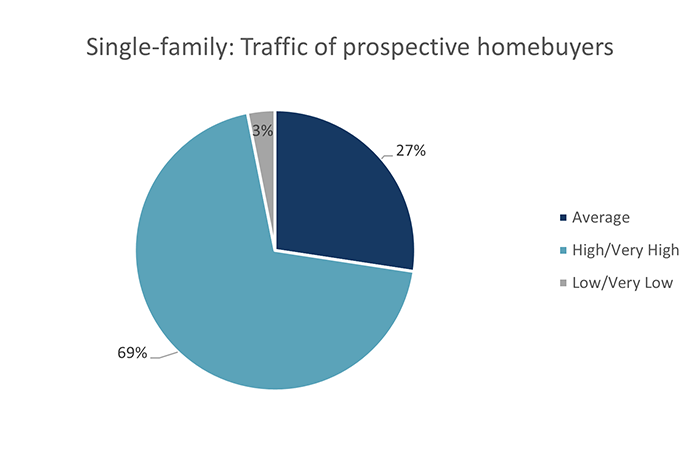

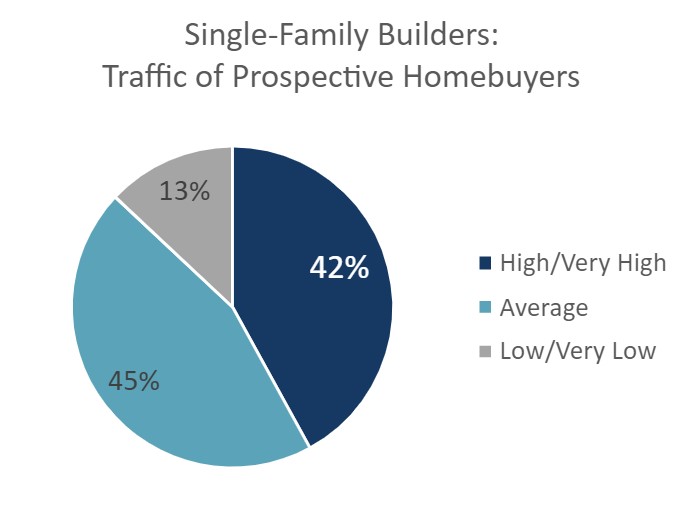

- Sales office traffic or general sales inquiries showed no signs of improvement, and 65% of builders rated conditions as Low or Very Low. The proportion of builders that rated traffic as High or Very High has remained in single digits since the third quarter of 2023.

- Regional trends showing Ontario and British Columbia faring much worse than builders in Prairies and Atlantic provinces continued this quarter. Builder confidence in Ontario fell to a record low of 7.4—recording single digits for the first time. Sentiment in British Columbia increased somewhat over last quarter but was still an abysmal 17.2. Sentiment in the Prairie Provinces was 49.0, remaining close to a neutral score for the past three quarters. Atlantic Canada was the sole bright spot for single family construction, rising 21.4 points over the previous quarter to 66.3—suggesting a strong start to the spring selling season.

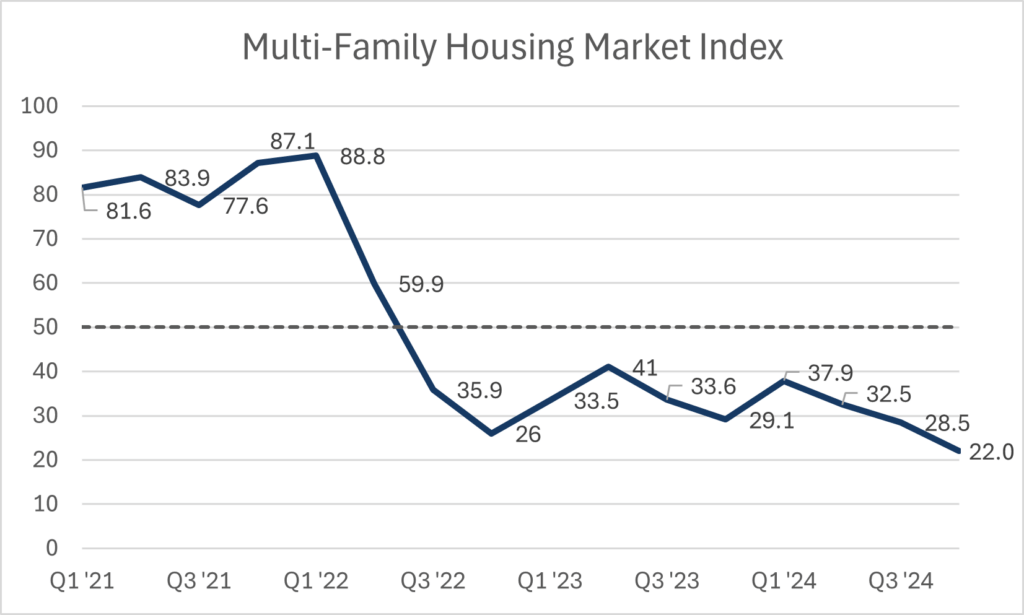

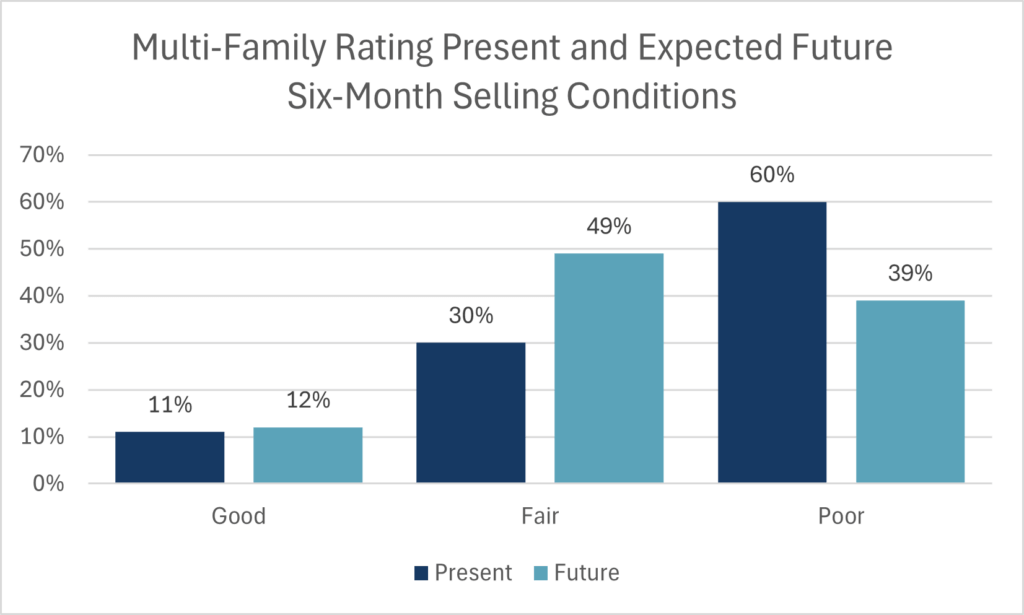

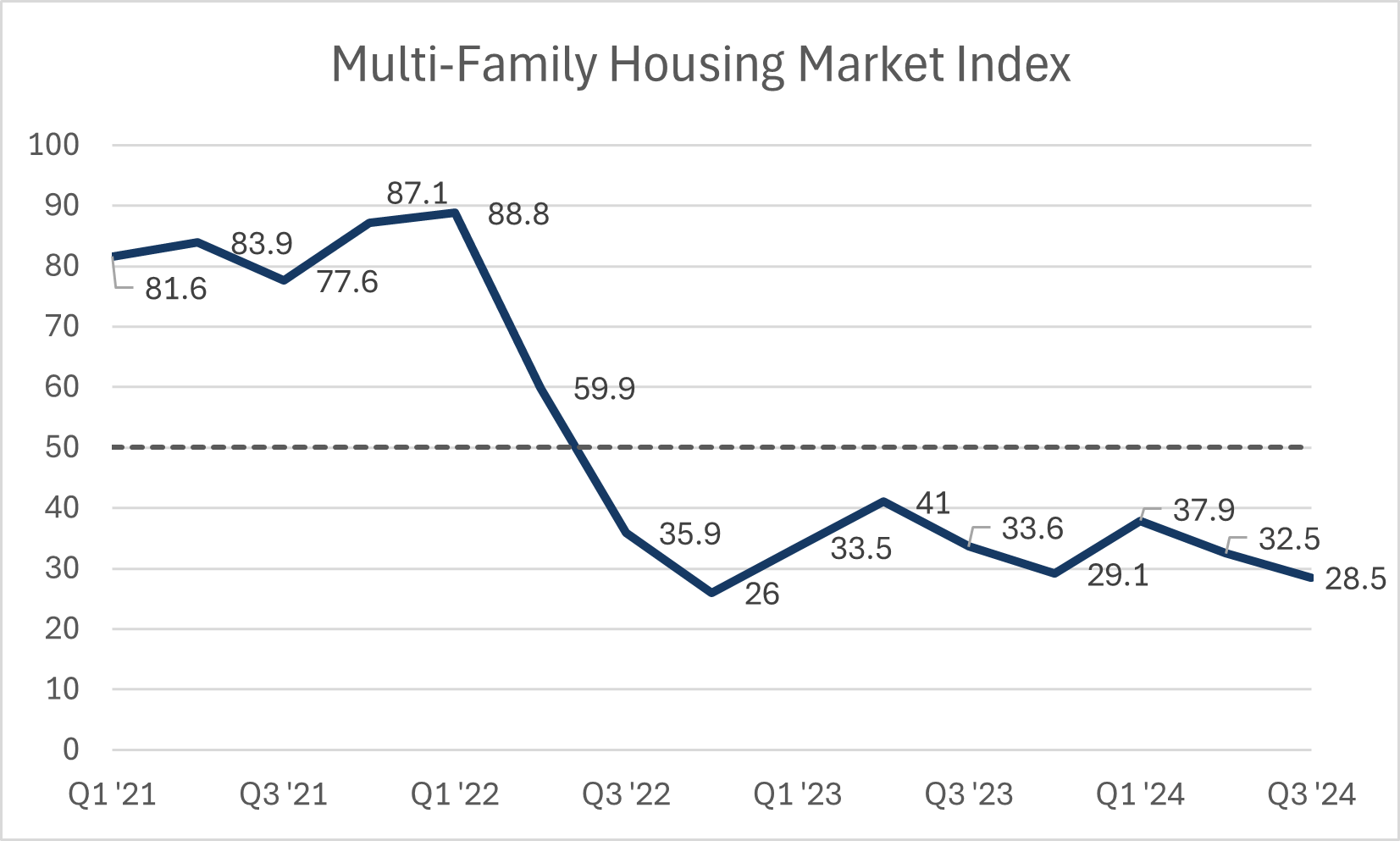

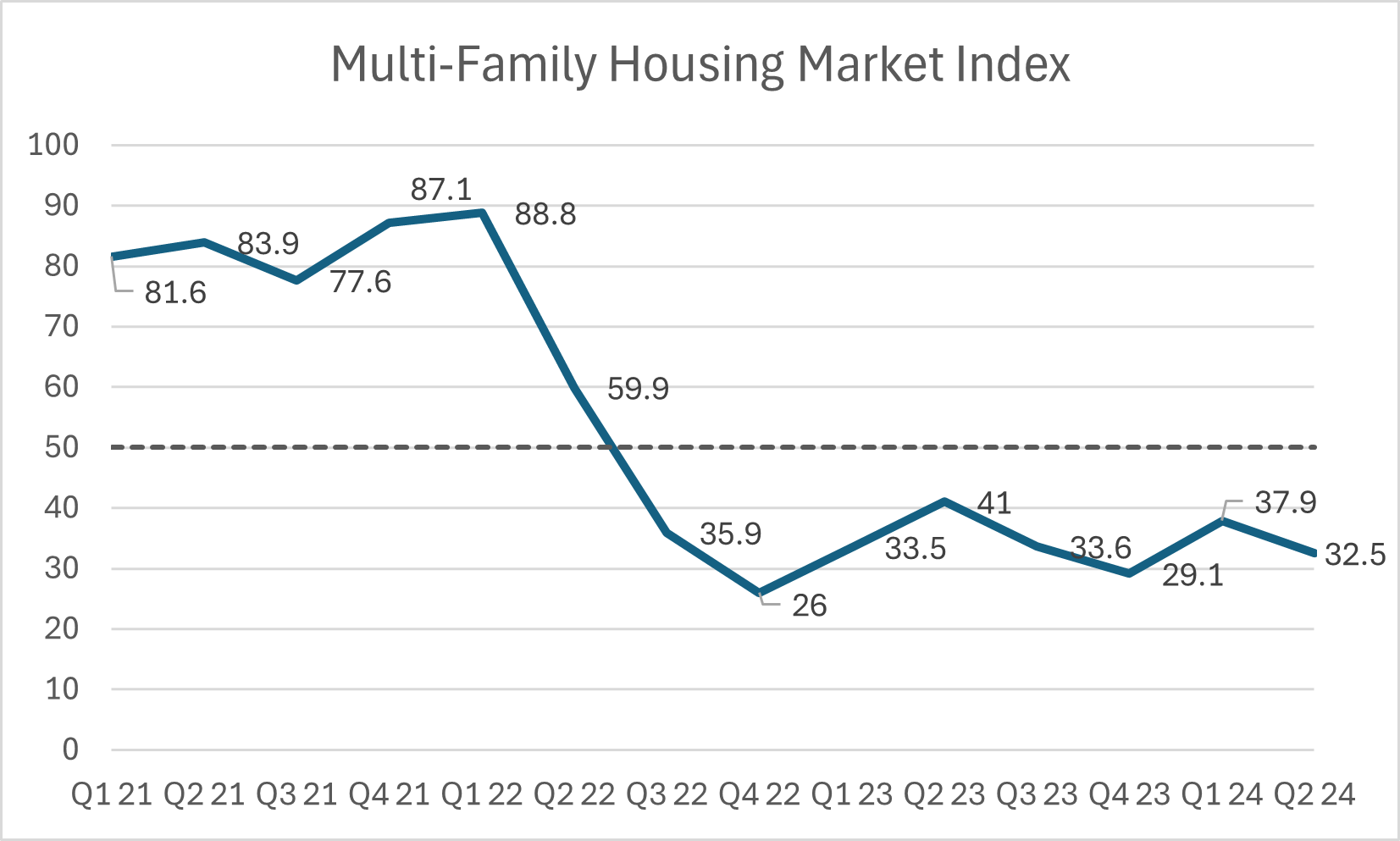

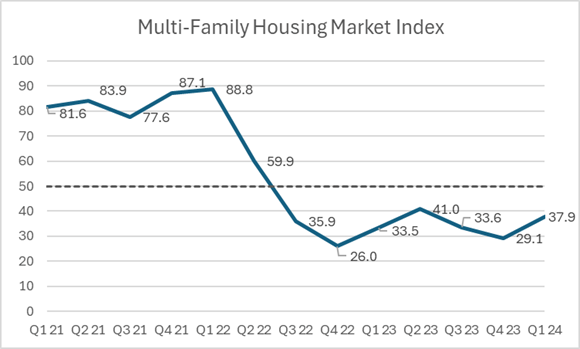

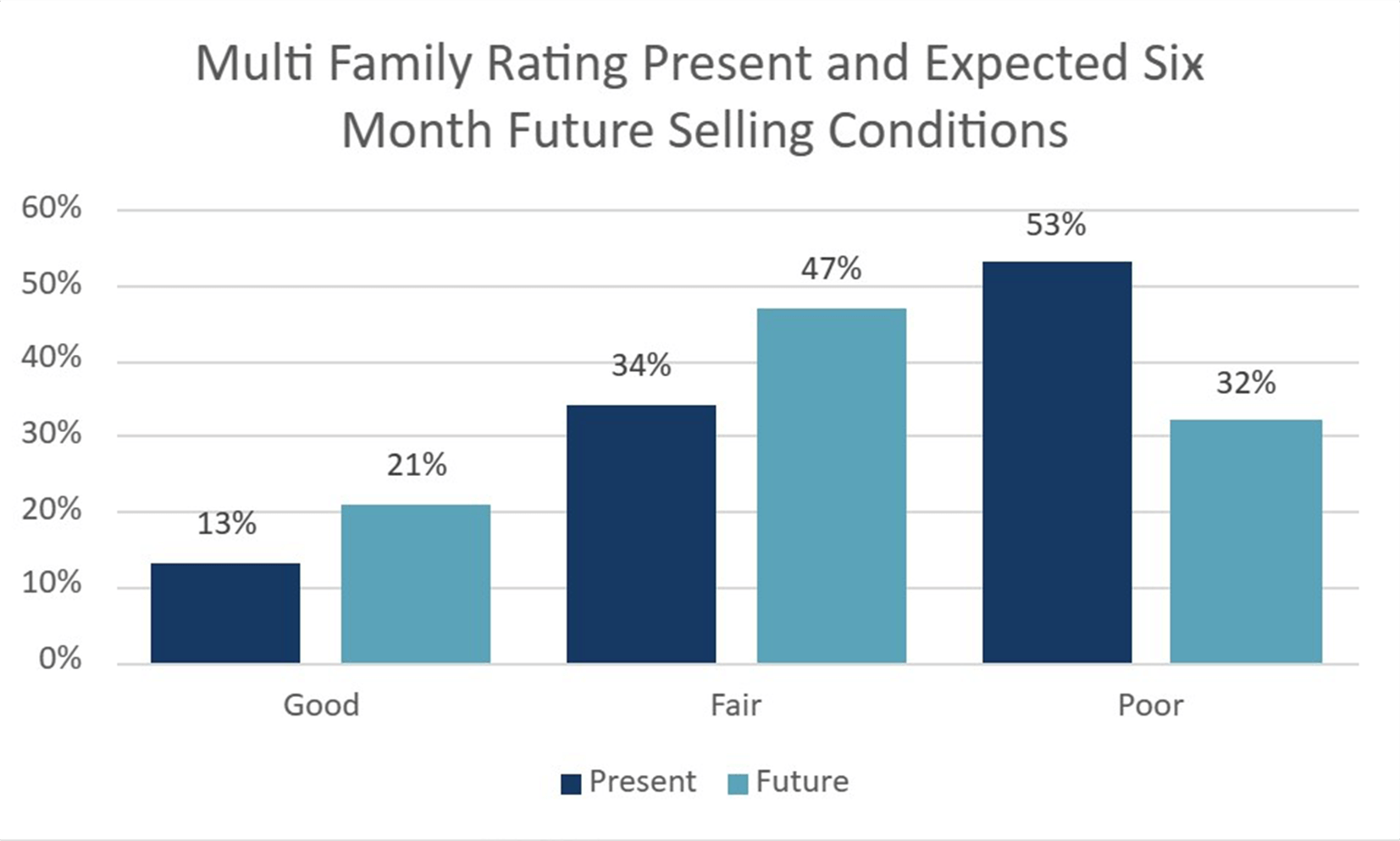

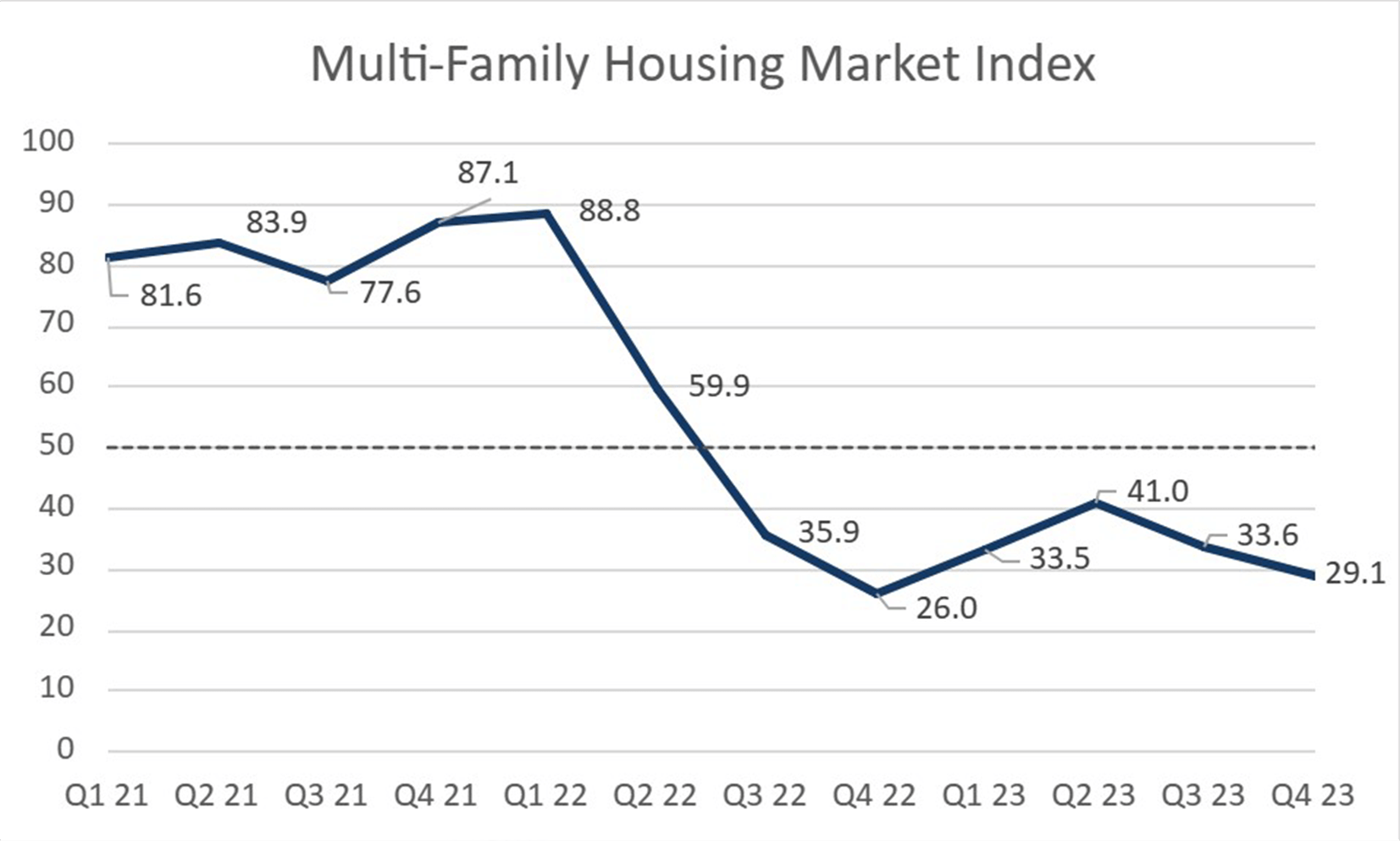

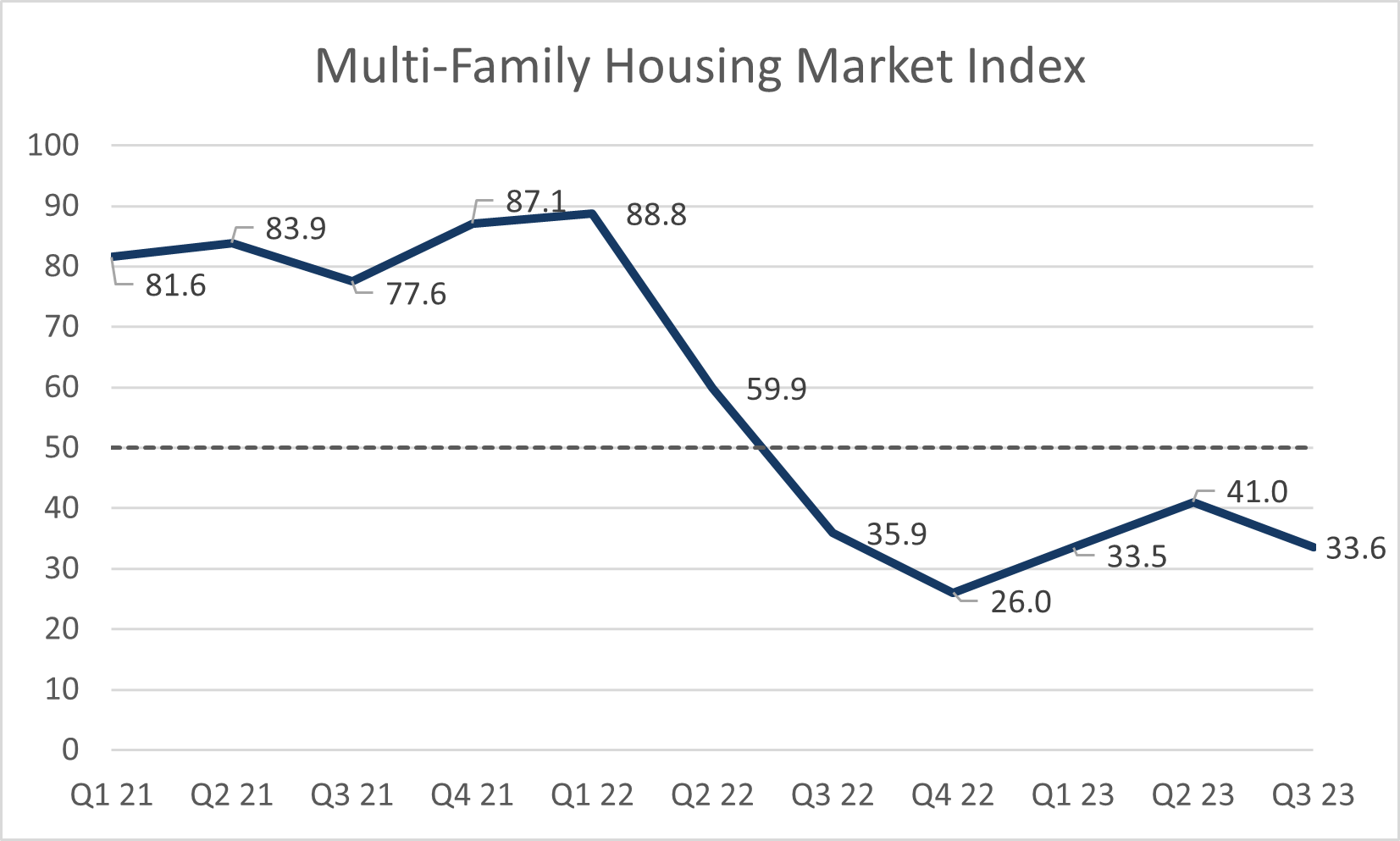

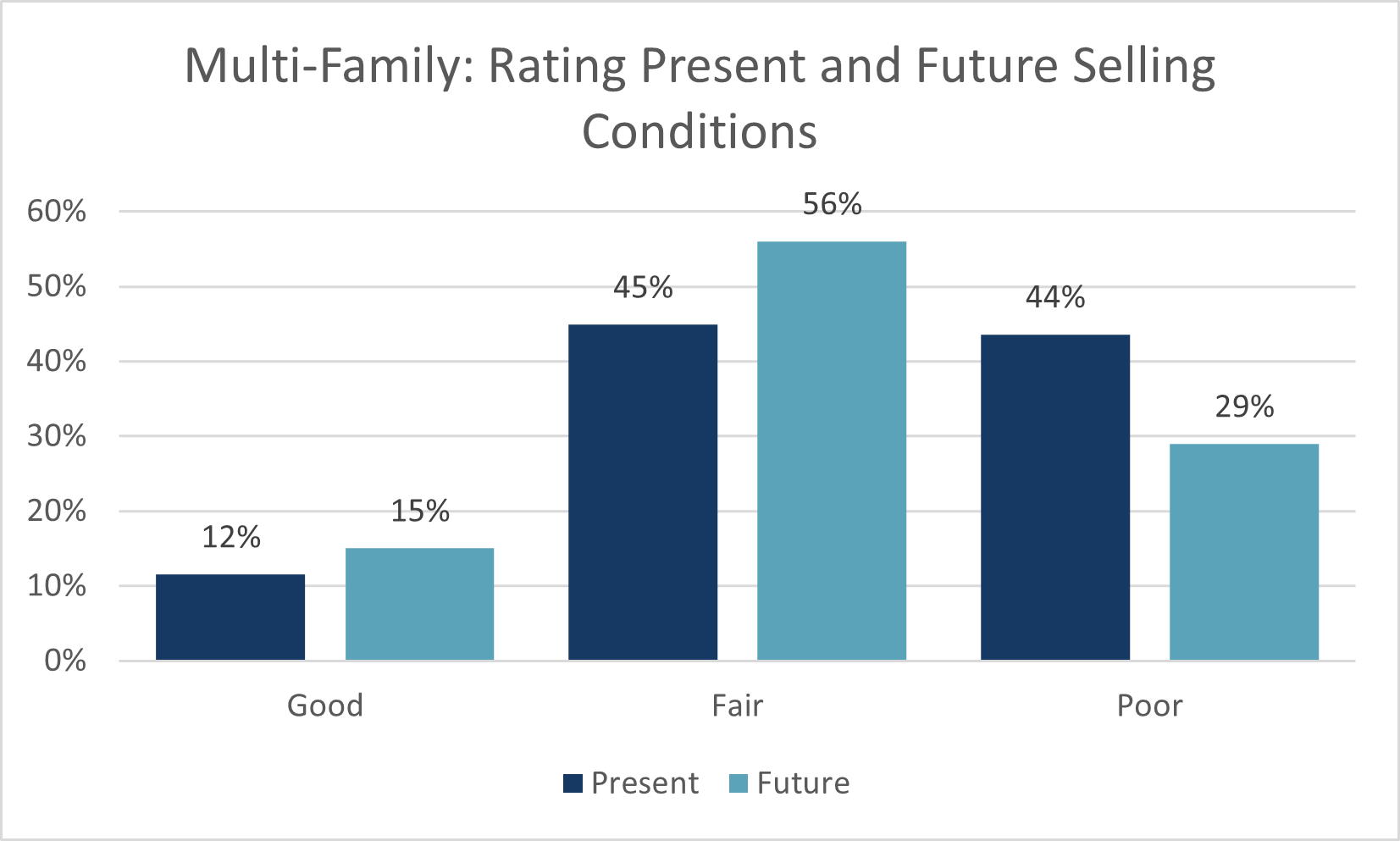

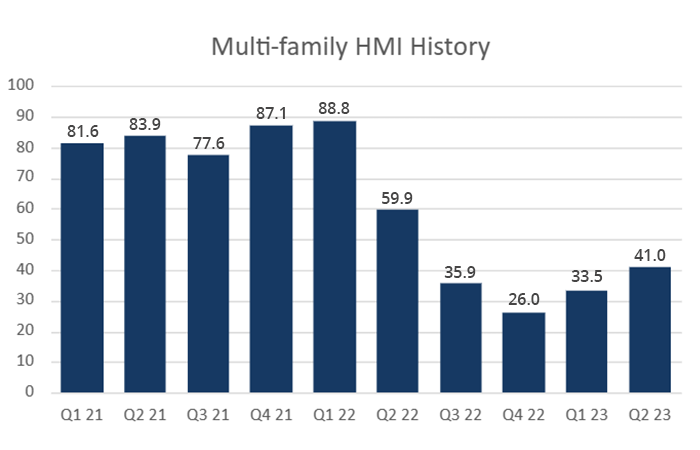

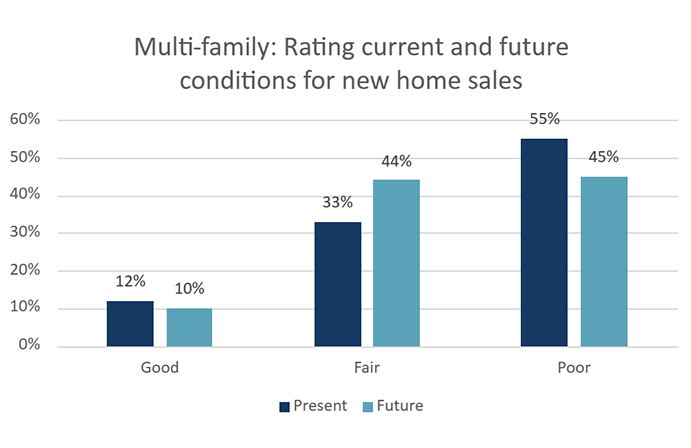

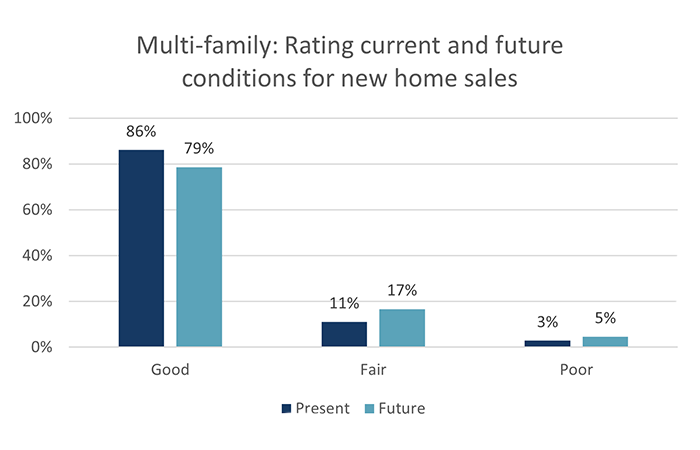

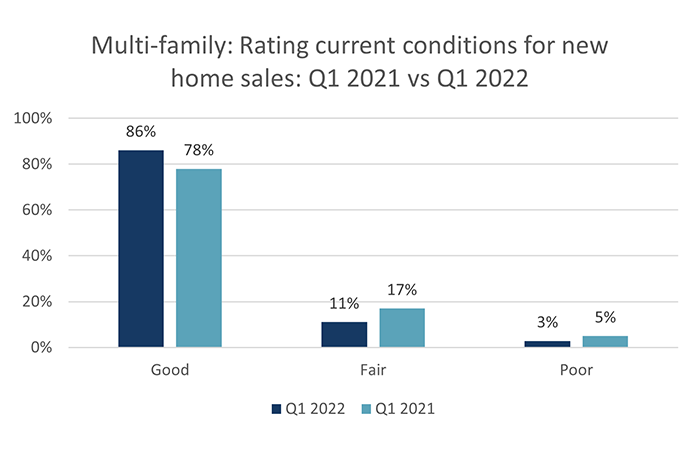

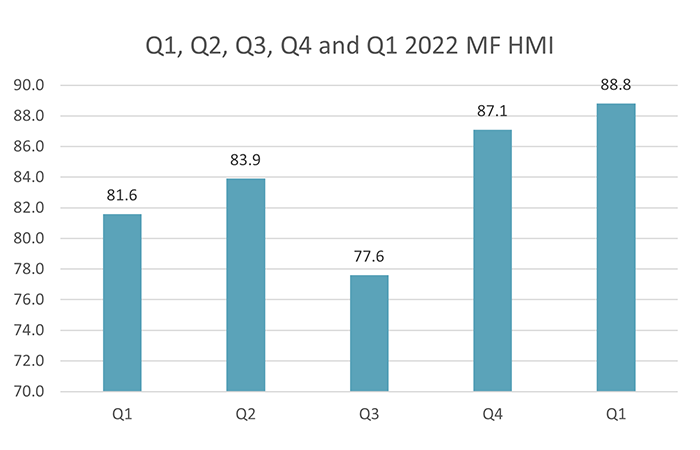

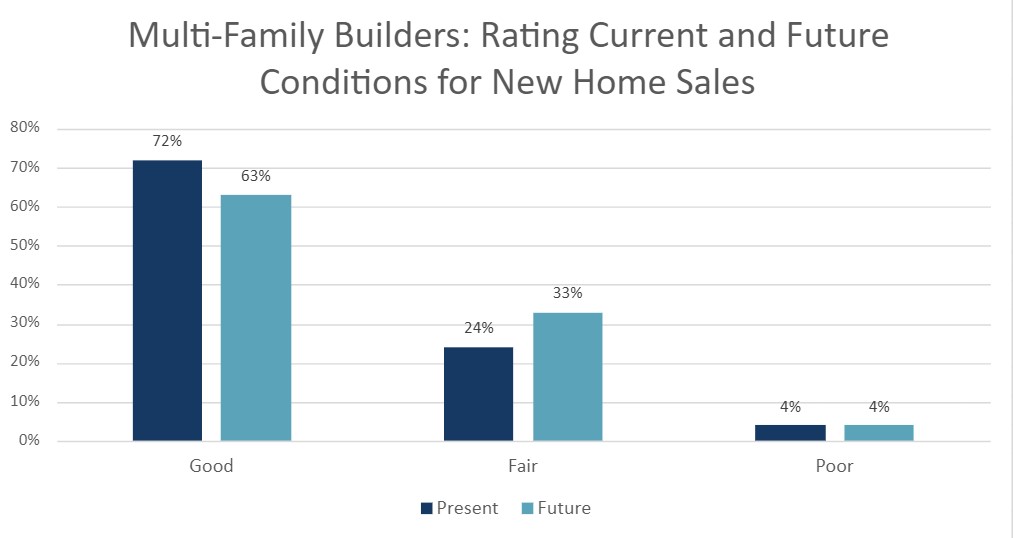

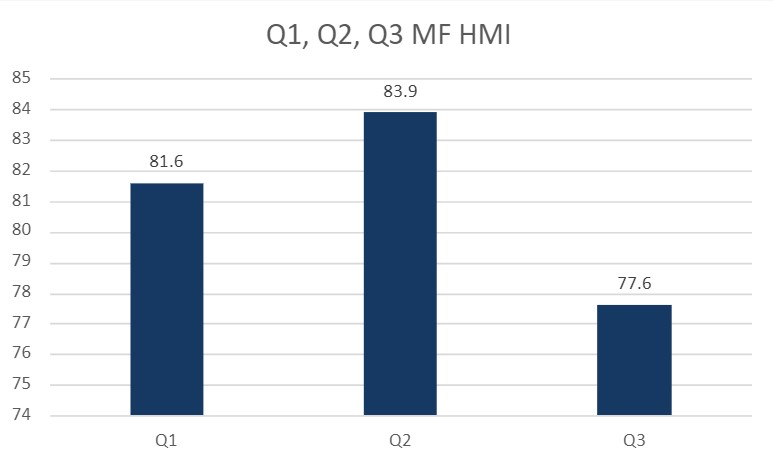

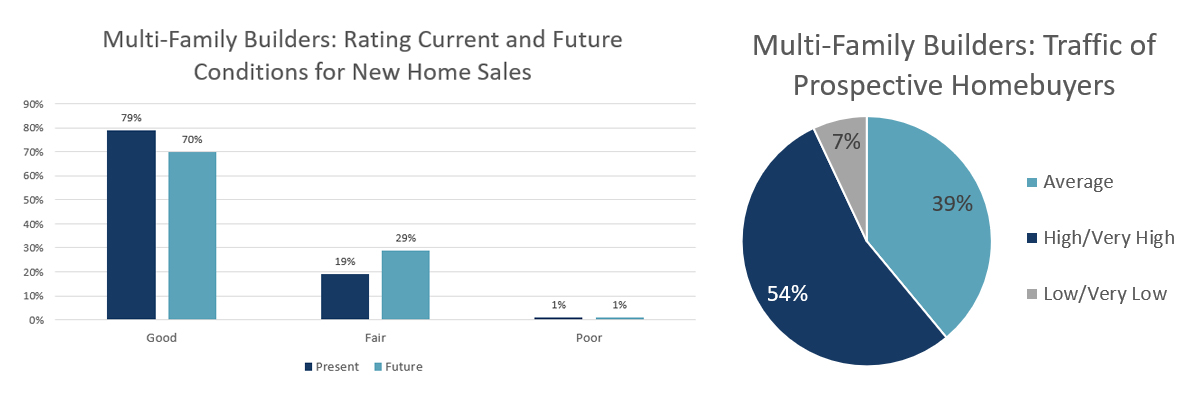

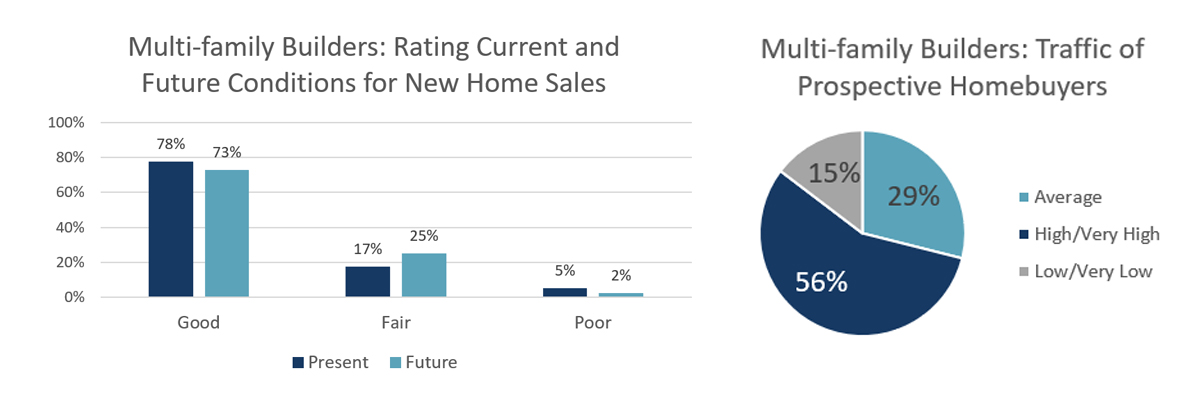

- The multi-family Housing Market Index was 22.3 in the first quarter of 2025, essentially unchanged from the record low of 22.0 recorded in the previous quarter. However, it is 15.6 points below the score recorded a year ago, suggesting that this year there is no seasonal boost from the start of the spring selling season.

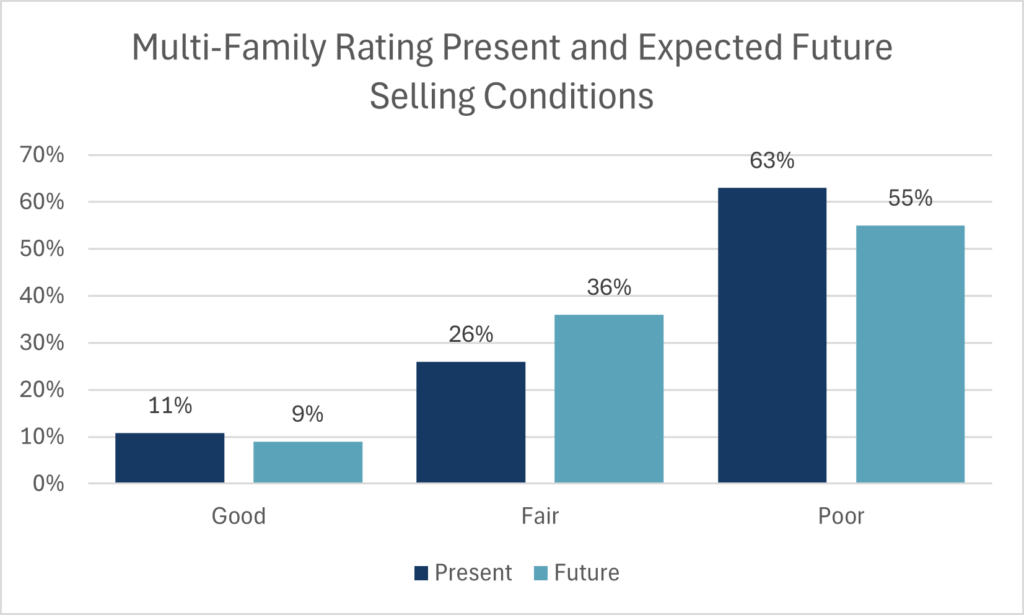

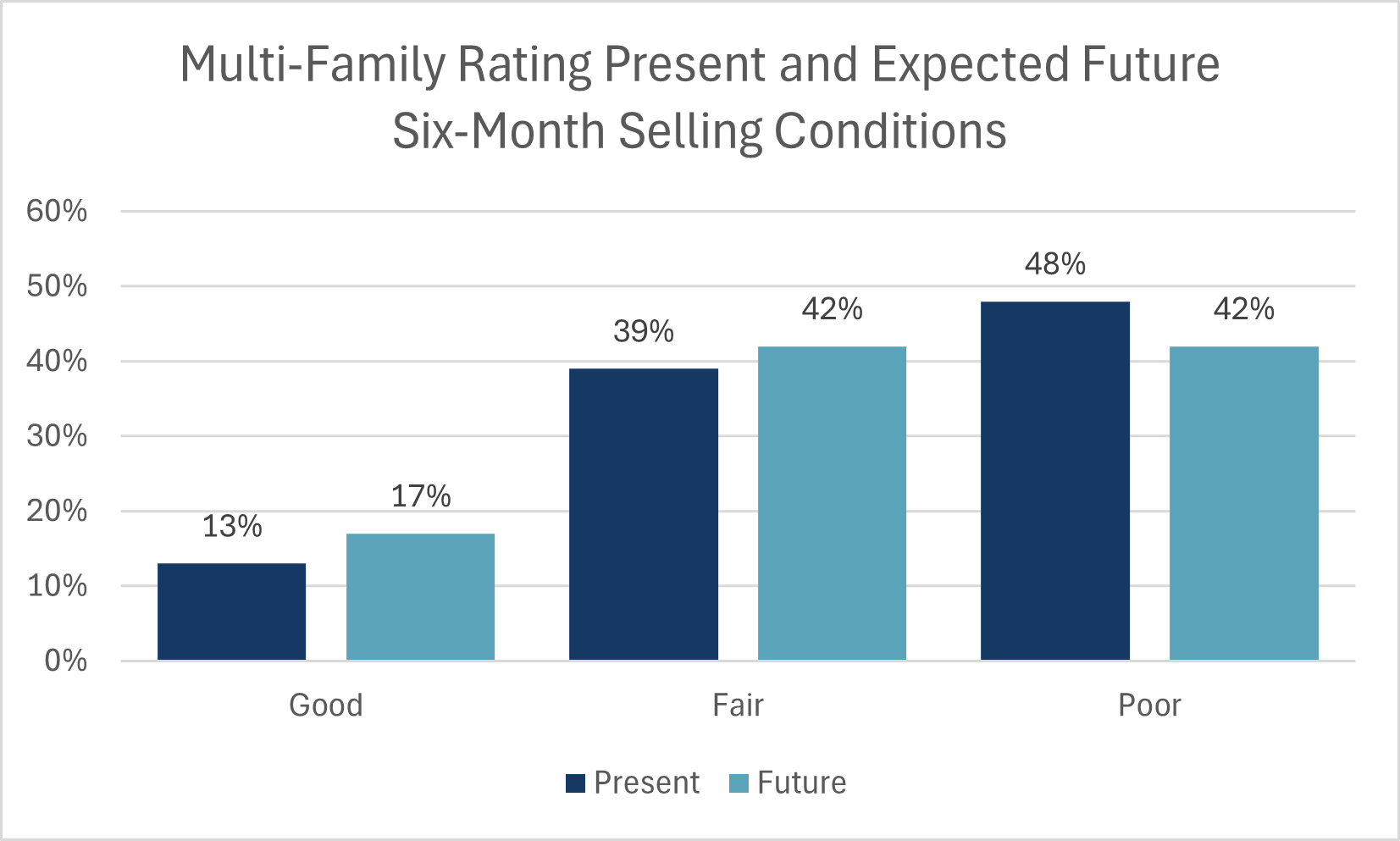

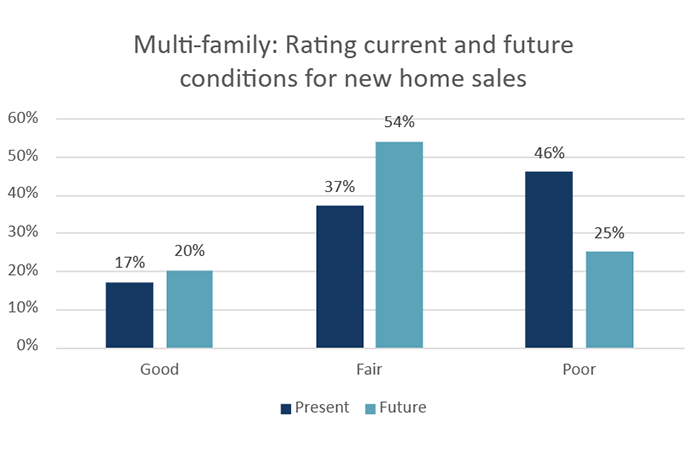

- Particularly concerning was the 63% of builders who rated current selling conditions as Poor. This was a record high in terms of the breadth of negative opinions. Only 11% rated sales as Good.

- Like the single-family HMI, in the past, multi-family builders have tended to expect improvement to average selling conditions in the near future. Bucking that trend, a record high 55% of builders rated their expectation for future selling conditions as Poor. Prolonged weakness in the market and the threat of tariffs have reduced this optimism.

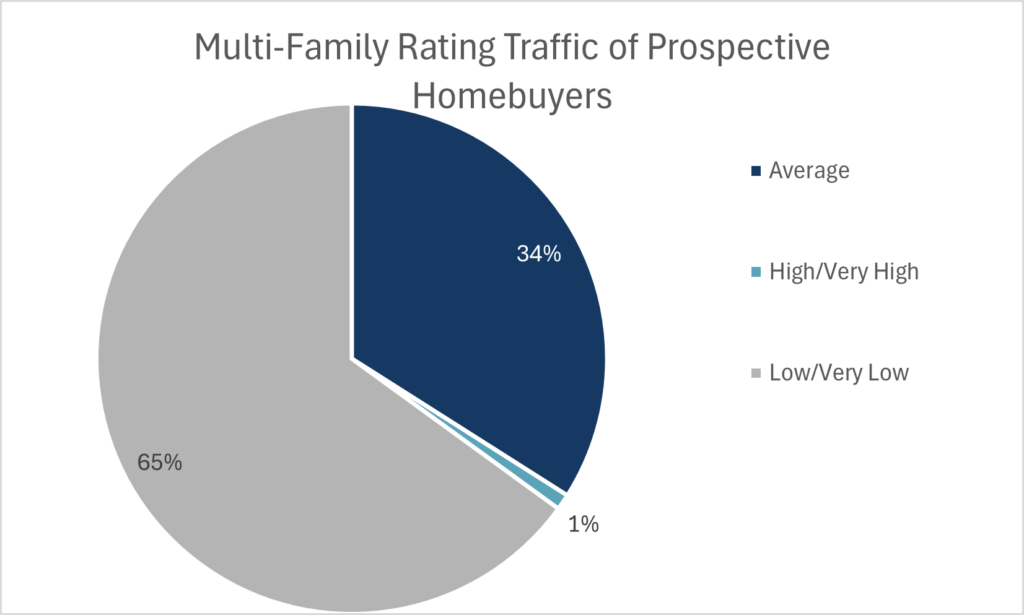

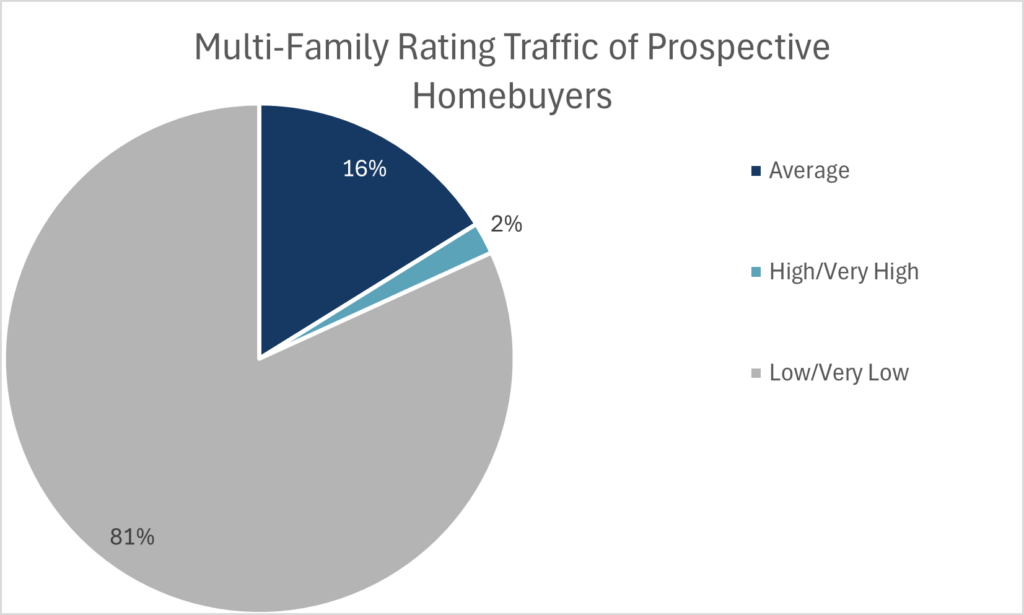

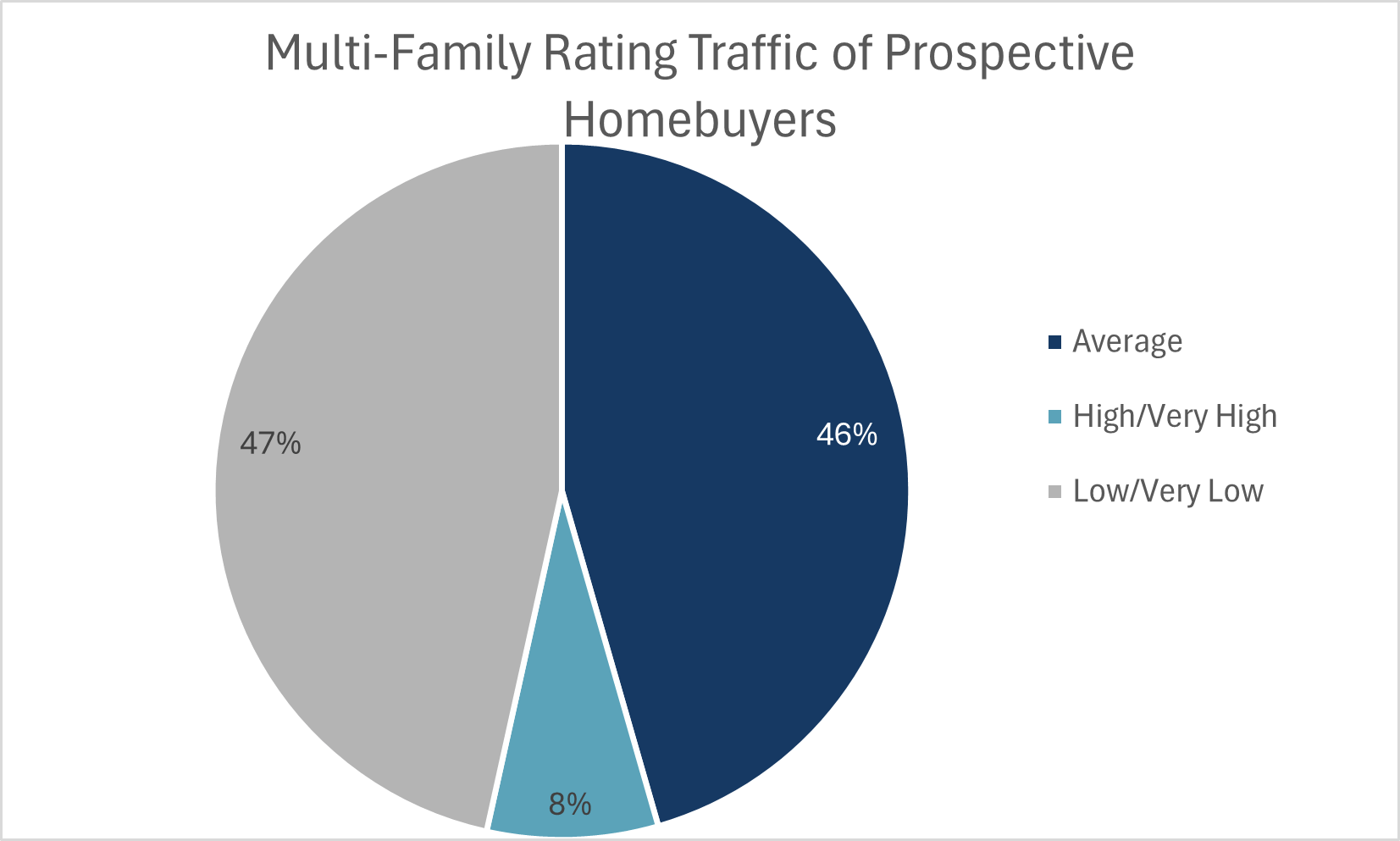

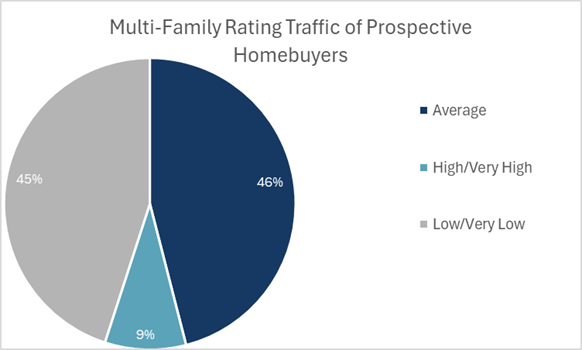

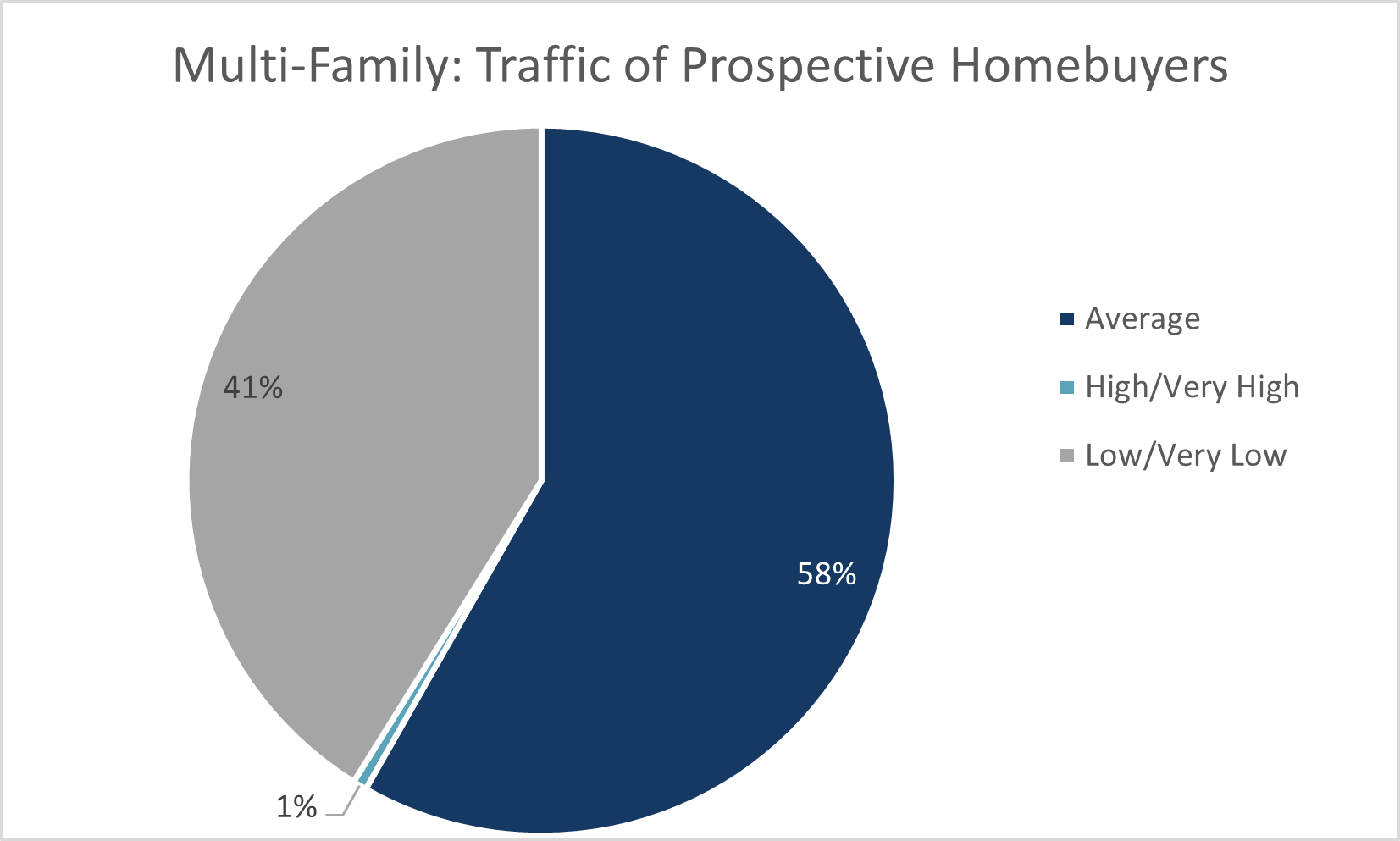

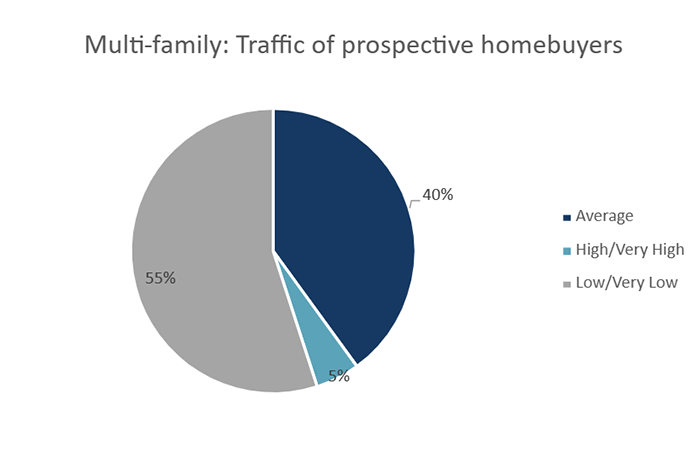

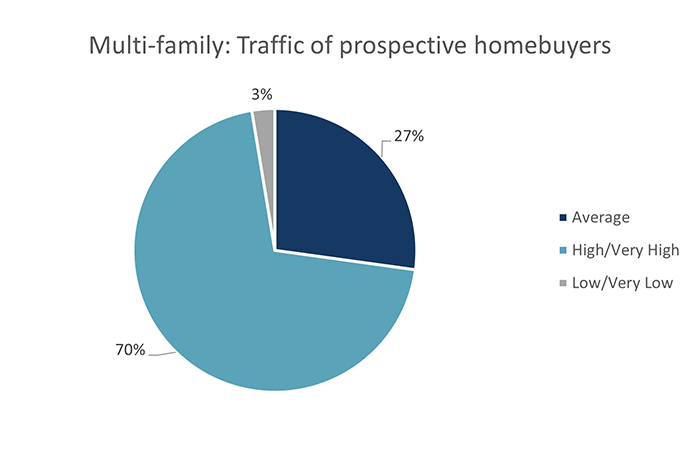

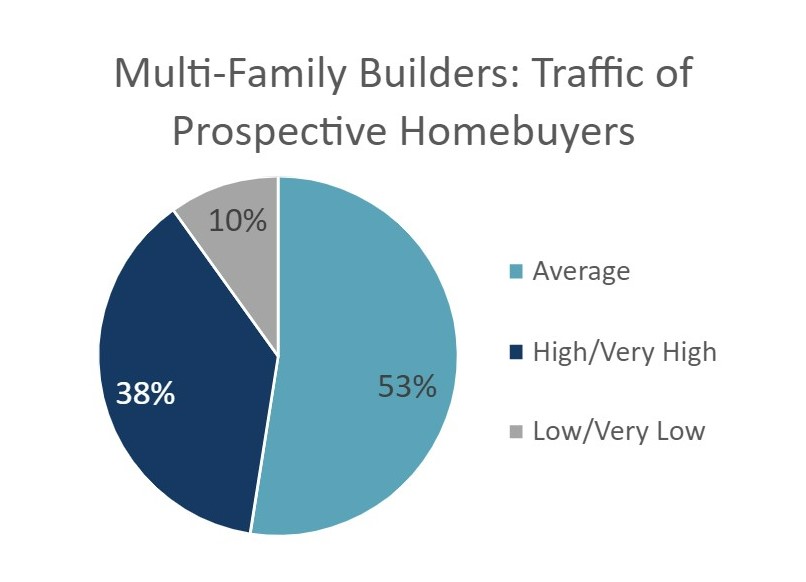

- Sales office traffic remained weak, as 65% of builders rated conditions as Low or Very Low. Surprisingly, this improved over the 81% that gave this rating the previous quarter, which could be related to seasonal factors. This improvement helped the overall multi-family HMI avoid setting another record low in builder confidence.

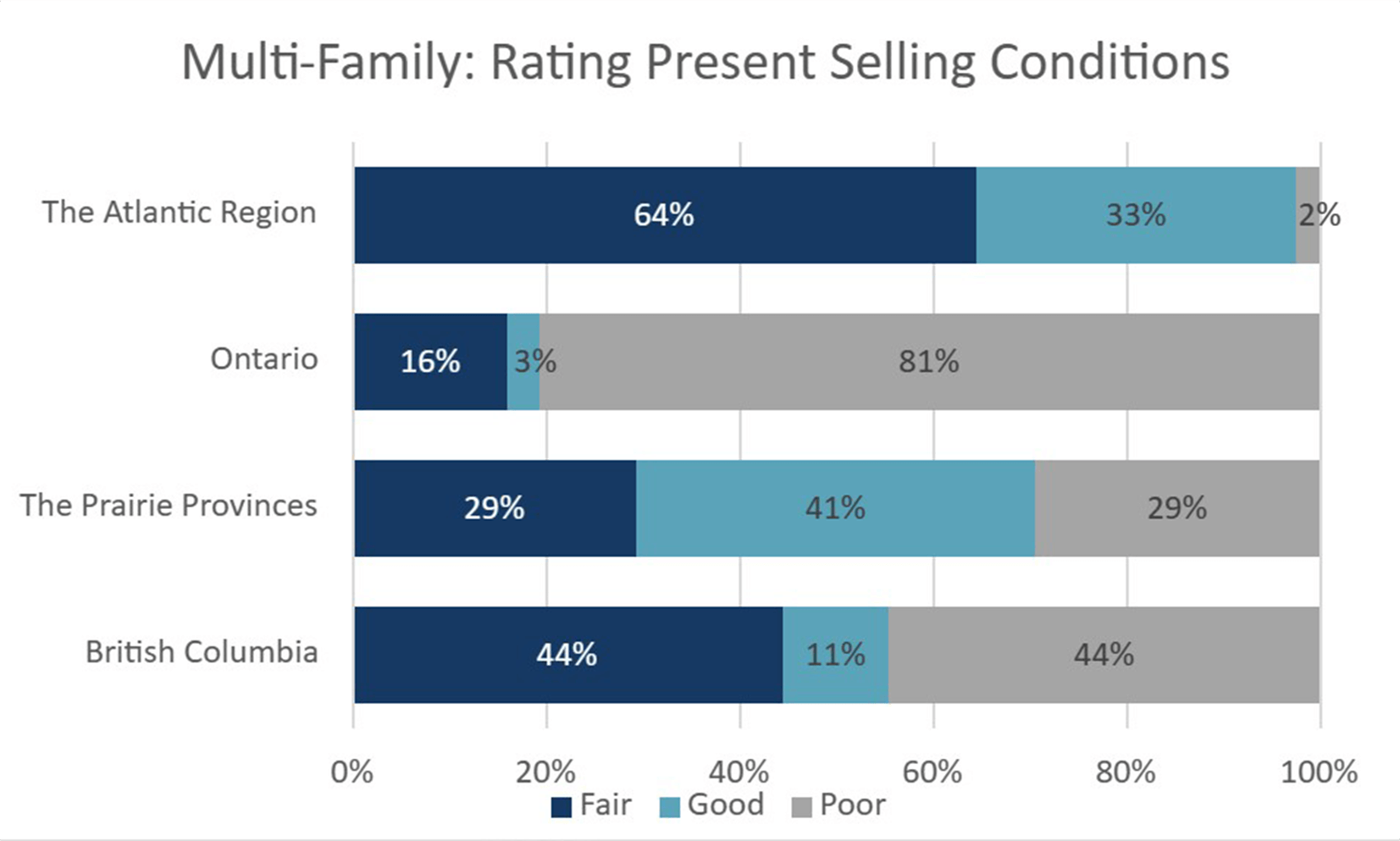

- Regional trends re-enforce how dire markets conditions are in Ontario, with an HMI of 2.9, falling from a score of 6.2 in the previous quarter. British Columbia remained pessimistic with a score of 24.8, down 18 points from a year ago. The Prairie Provinces maintained their position as the sole bright spot, with a score of 61.3, rising 6.8 points from a year ago.

.png)

.png)

.png)

Each quarter, CHBA asks a set of topical questions to understand the HMI results better as well as other industry issues. This quarter, the questions were largely focused on the threat of tariffs. While Canada’s phase II list of counter tariffed products was not implemented on April 2nd, it has not been officially removed as policy consideration, pending what the U.S. does moving forward.

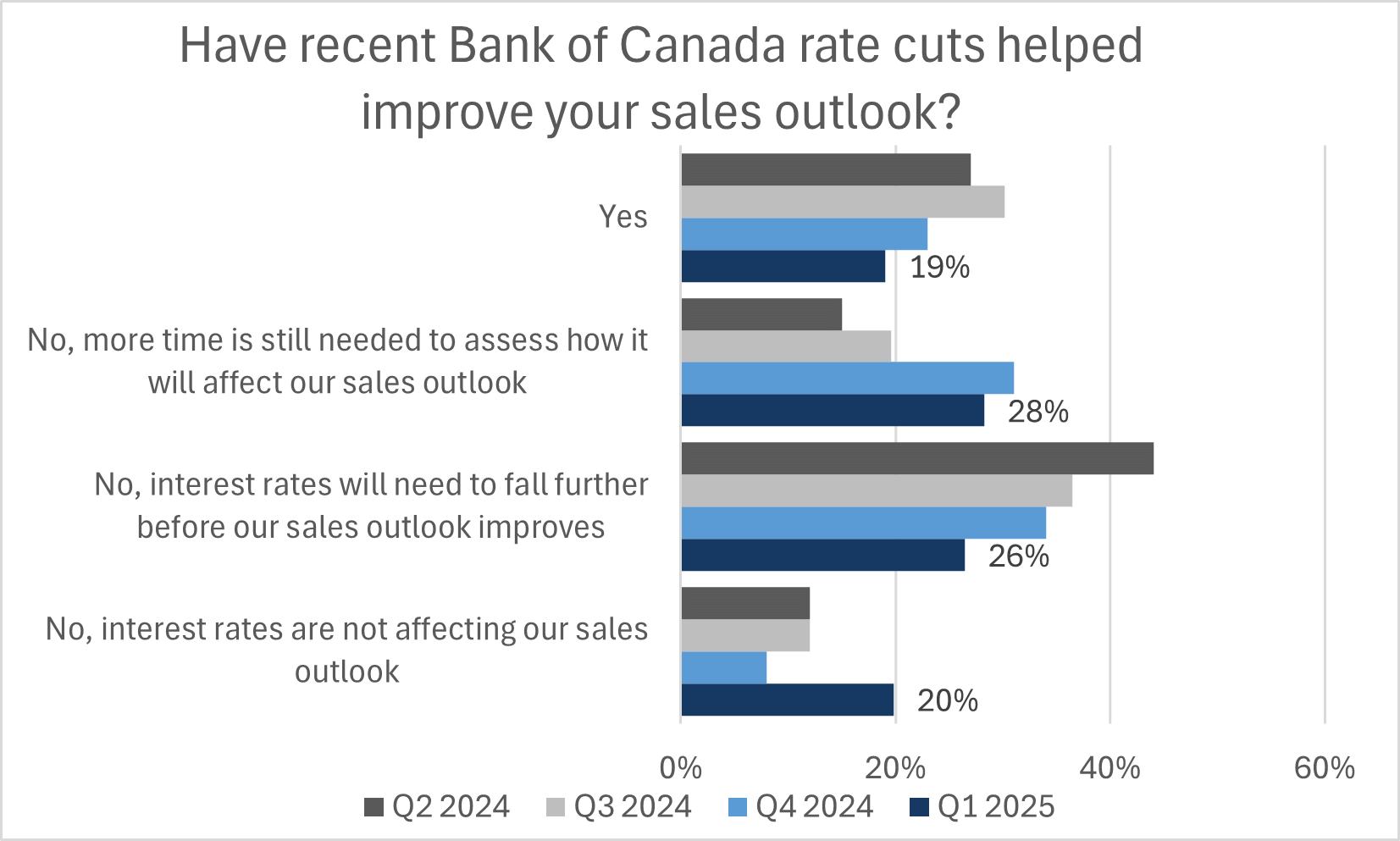

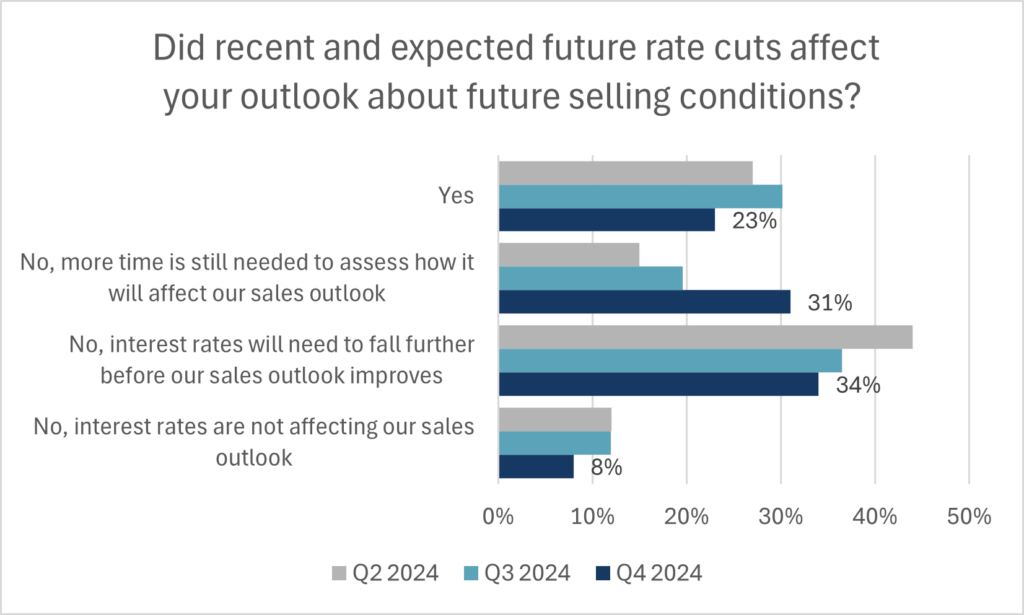

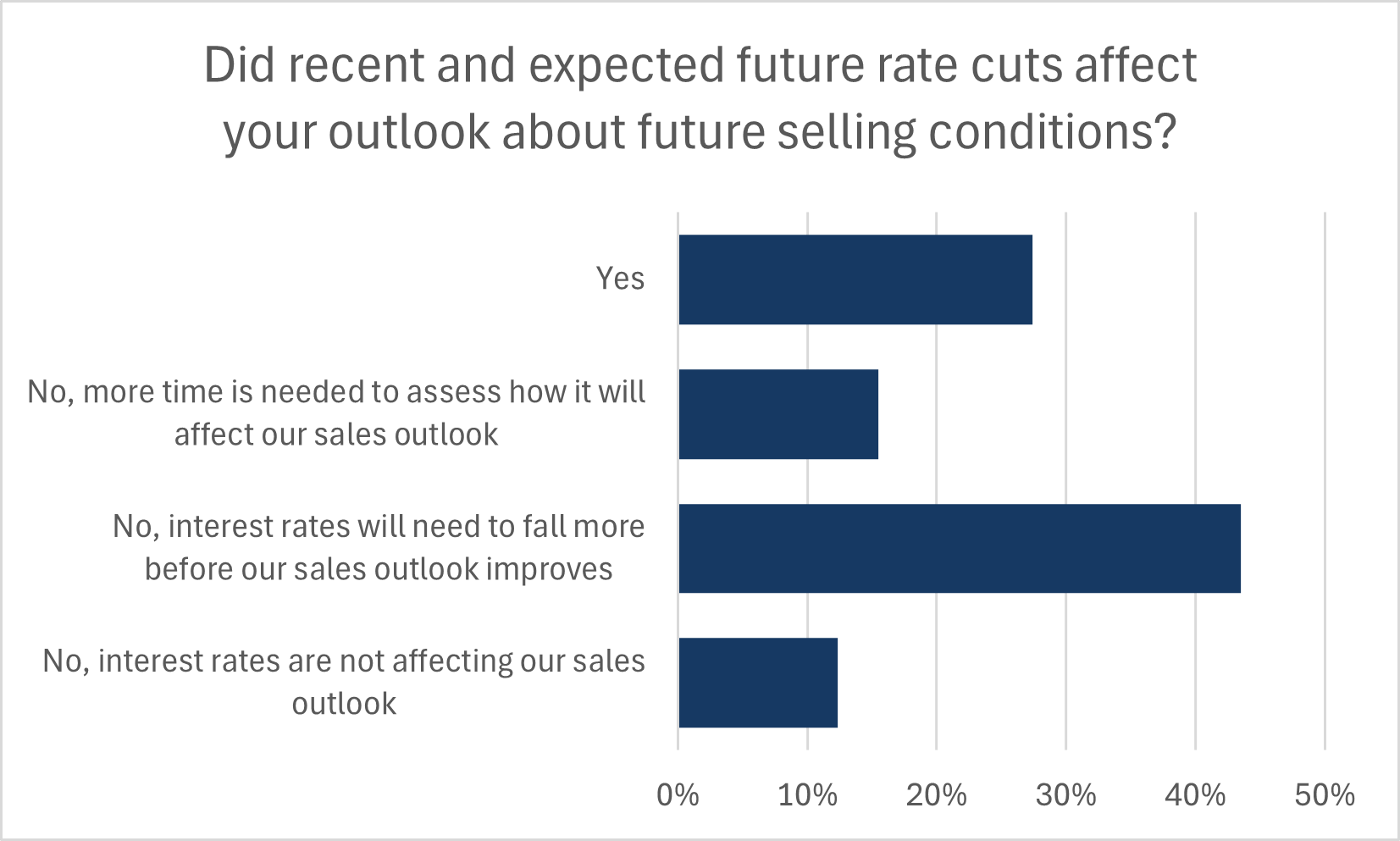

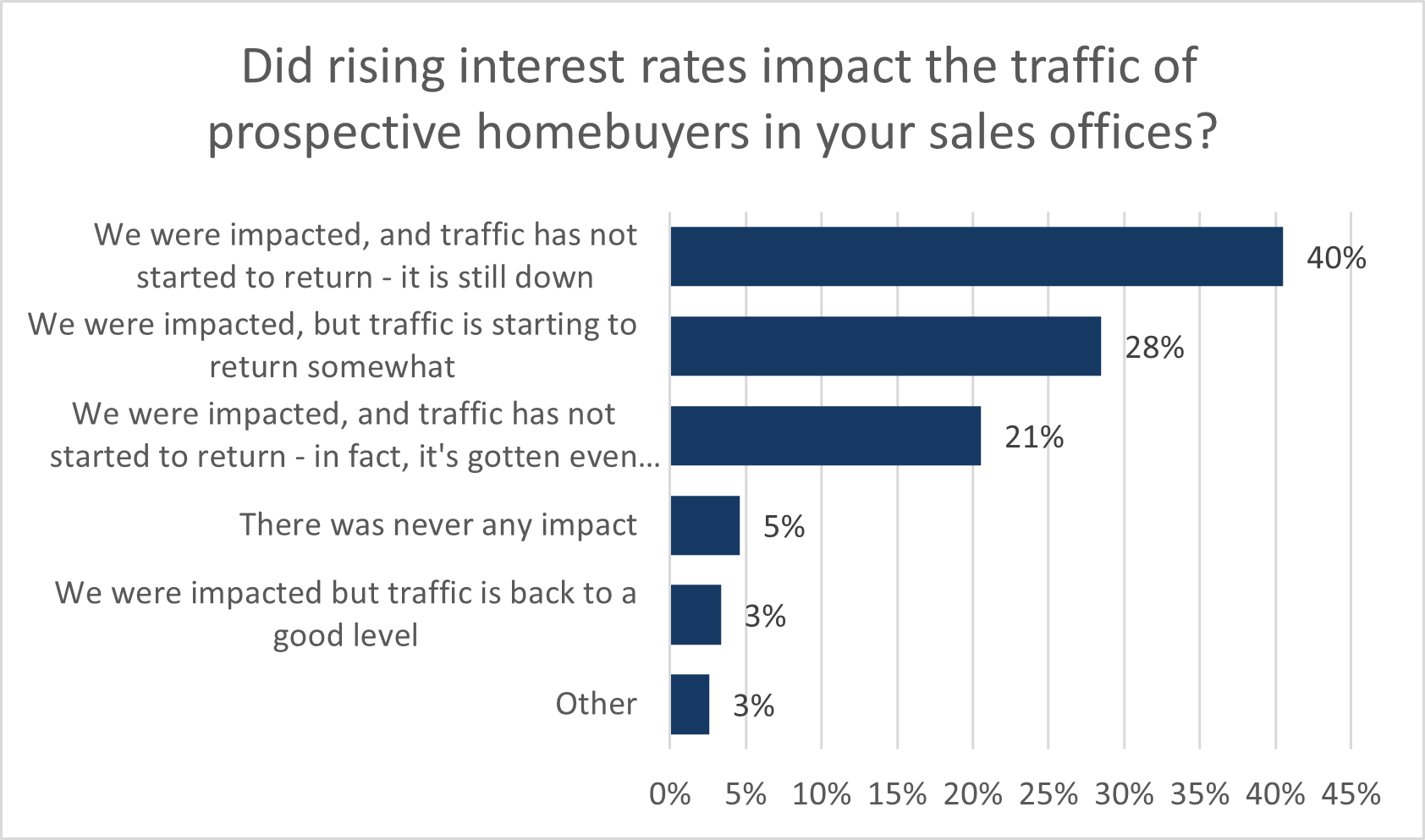

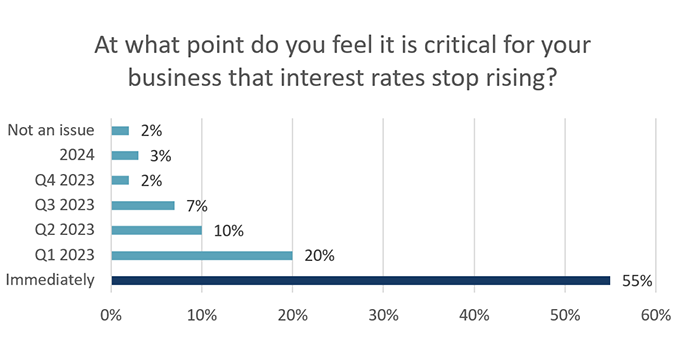

- Builders were asked if the Bank of Canada’s 25 basis point cuts in January and March helped improve their expectations for sales over the next six months. Just 19% stated that it did, notably lower than the three previous quarters. The biggest change from past quarter was in the 20% of builders saying that interest rates are not affecting their sales outlook, up from 8% last quarter and 12% in Q2 2024. This is reflective of the trade war, but also mortgage rates not lowering in tandem with the Bank of Canada rate.

- Builders were asked if they had already received a notification from a supplier about a cost increase in 2025—regardless of the reason. 71% of builders said they had, while 24% said they have not. The threat of tariffs threatens to increase the prices of a broad range of goods and likely includes items that are not listed under Canada’s counter tariffs.

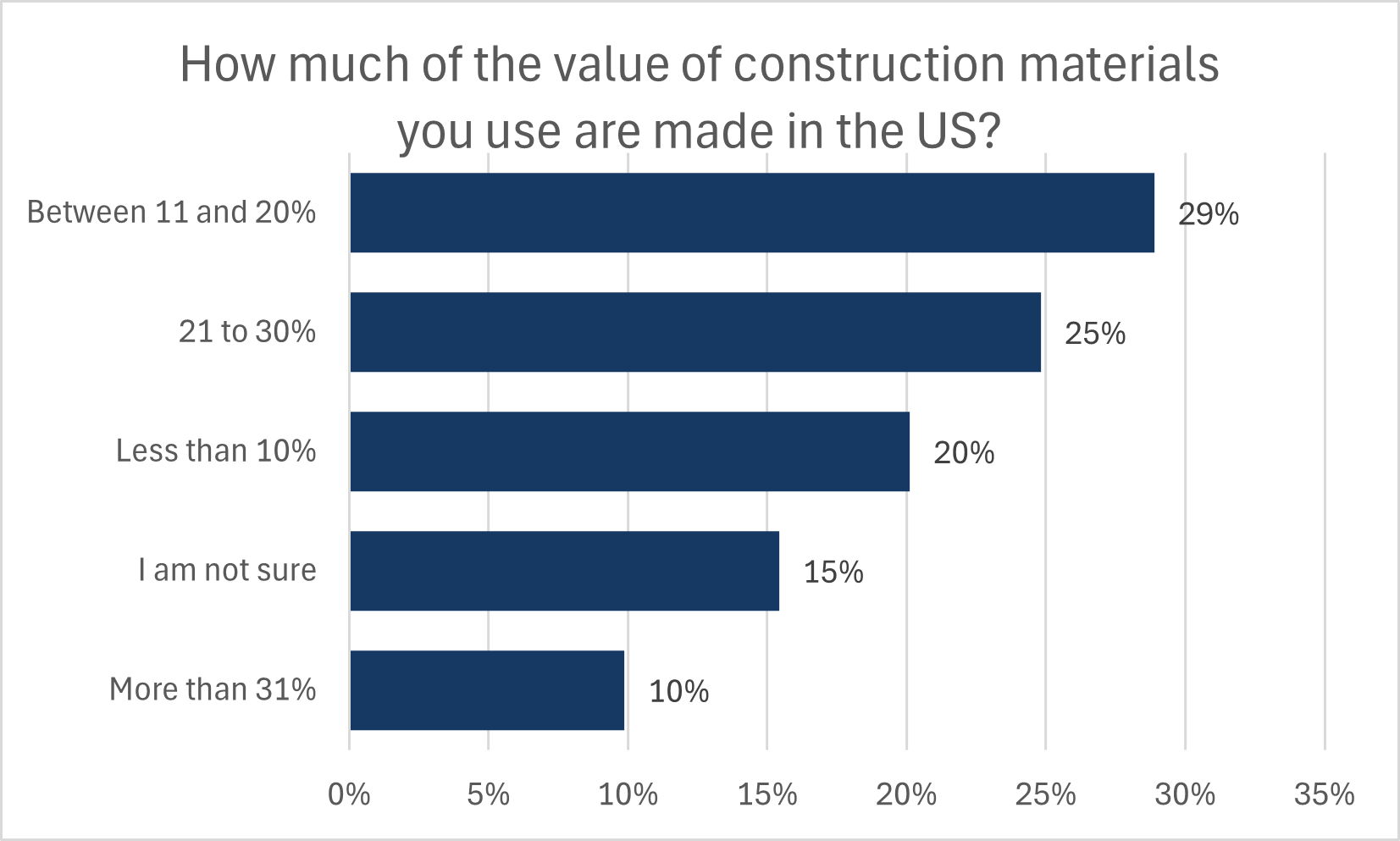

- To help judge the impact of tariffs on building construction, builders were asked to provide an estimate of the proportion of the value of total building materials that is made in the US. 29% of builders said that between 11 and 20 percent of the value of materials is made in the US, which was the most common answer. Just 10% said that more than 31% of the value of materials comes from the U.S. In general, most products can be sourced domestically or imported from non-U.S. trading partners. However, this is not a certainty, as country of origin has been less of a factor under free trade.

- Canada has implemented tariffs on $30 billion worth of U.S. product imports, including most large kitchen and/or laundry appliances. 75% of builders state that they supply these appliances in their purchase agreements, however a large portion of builders were not sure if these appliances simply came from the U.S. or were a product made in the U.S. After removing the builders who were unsure, on average, 53% of the large appliances supplied by these builders are believed to be subject to tariffs on U.S. products

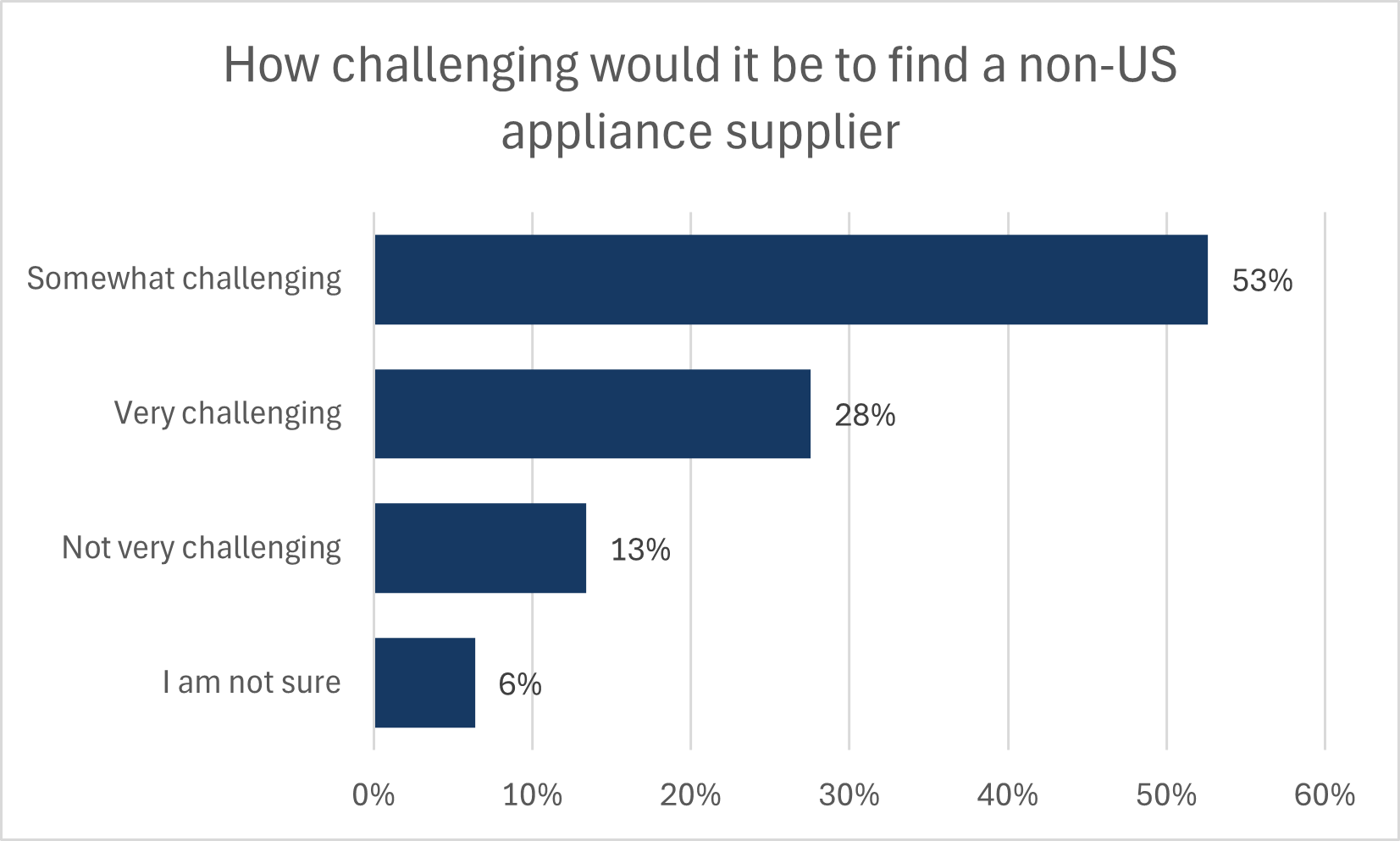

- 53% of builders believed finding non-U.S. appliance suppliers will be somewhat challenging and a further 28% believe it will be very challenging. CHBA has advised government officials that additional overseas production is often geared towards smaller standards of Europe and Asia, making additional sourcing problematic.

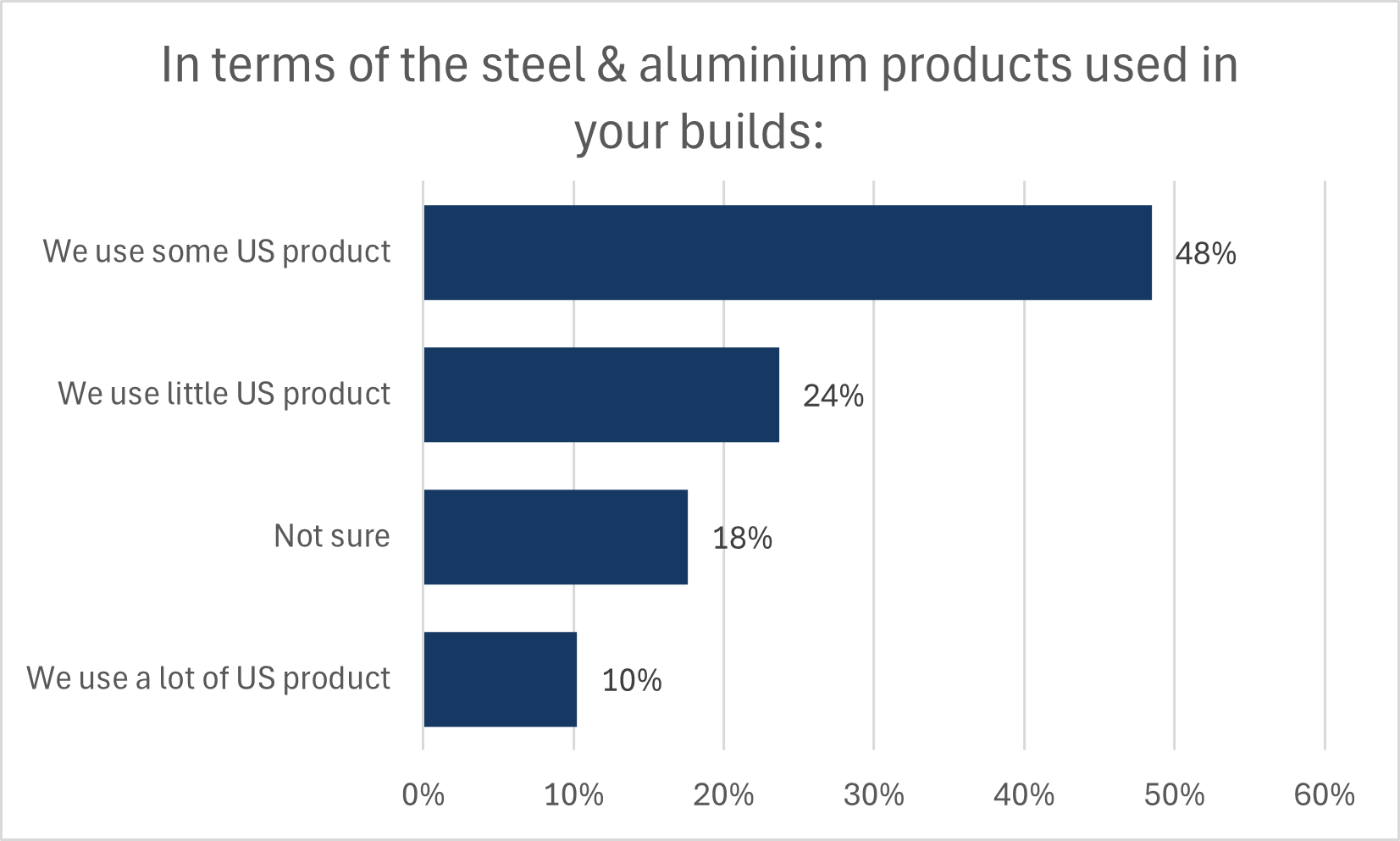

- In response to the U.S.’s global tariffs on steel and aluminium as well as products made of these materials, Canada has implemented counter tariffs on these goods in return. Understanding the difficulty in estimating the level of U.S. product, builders were asked to subjectively judge how much U.S. steel and aluminium they use in construction. 48% of builders stated that they use some U.S. product and 24% said they use a small amount of U.S. product.

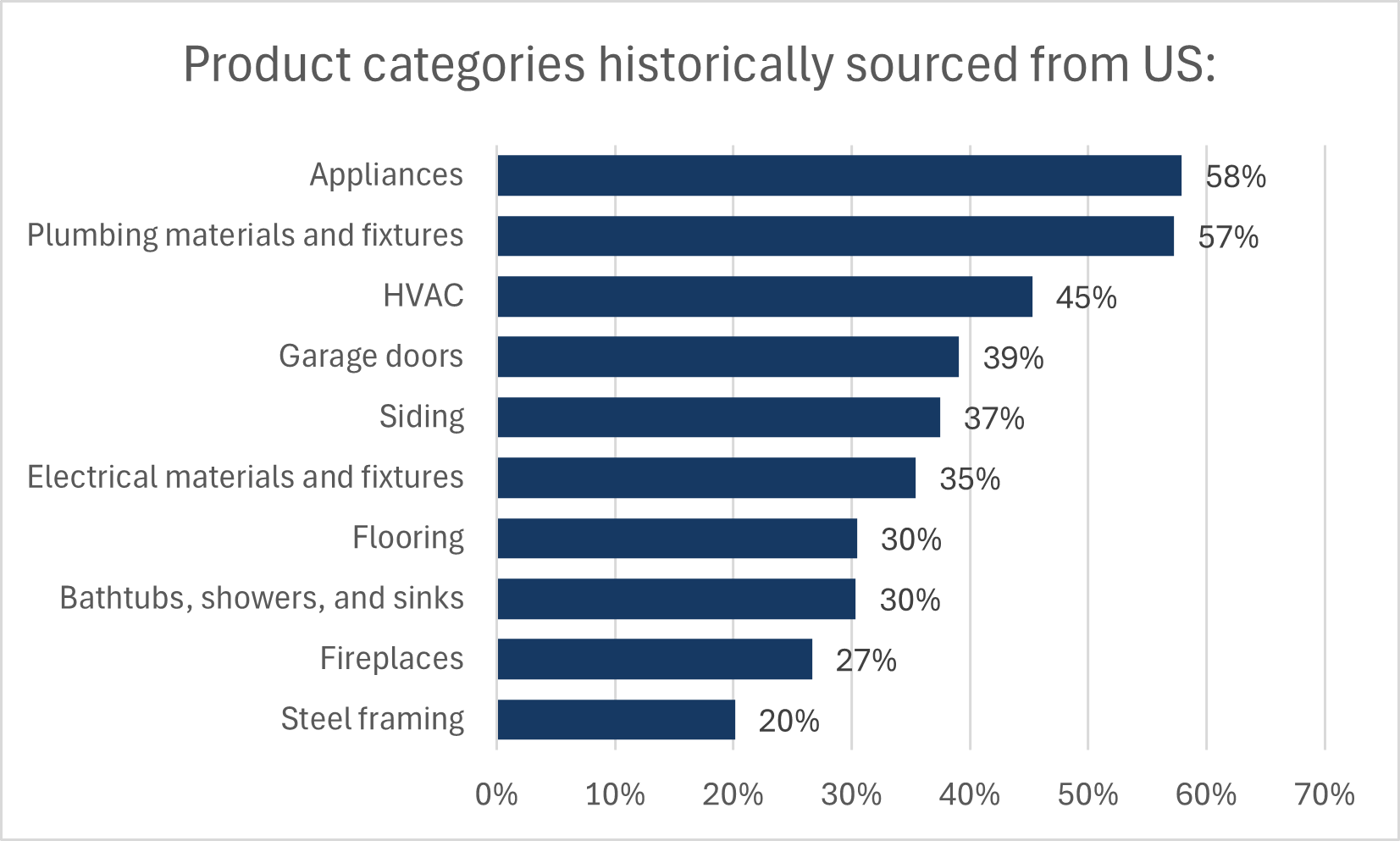

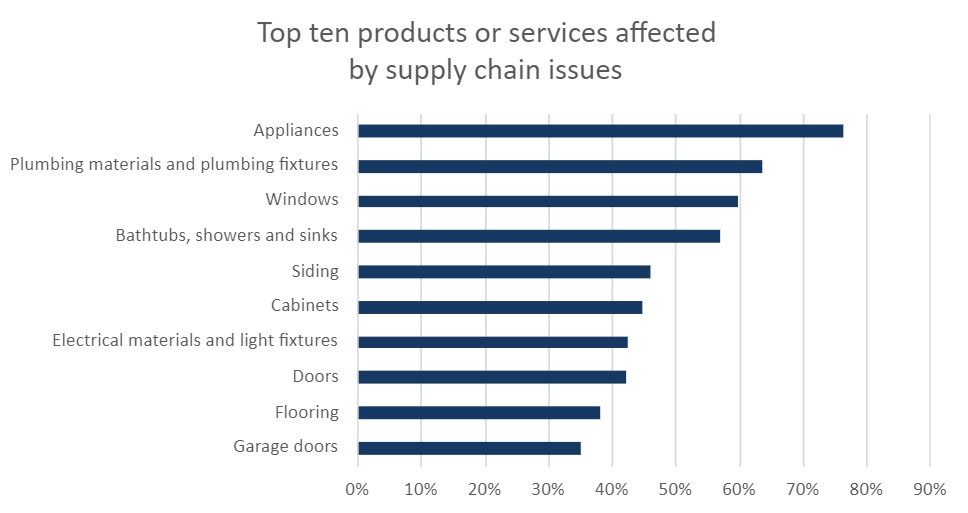

- Many other building materials are contained within the $125 billion Phase II list of counter tariffed goods, which could still be implemented, depending on U.S. tariff announcements going forward. Builders were asked to identify any broad building material categories that they have historically sourced from the U.S. Among the most exposed product categories to U.S. imports, according to builders, were appliances and plumbing products at 58% and 57% respectively.

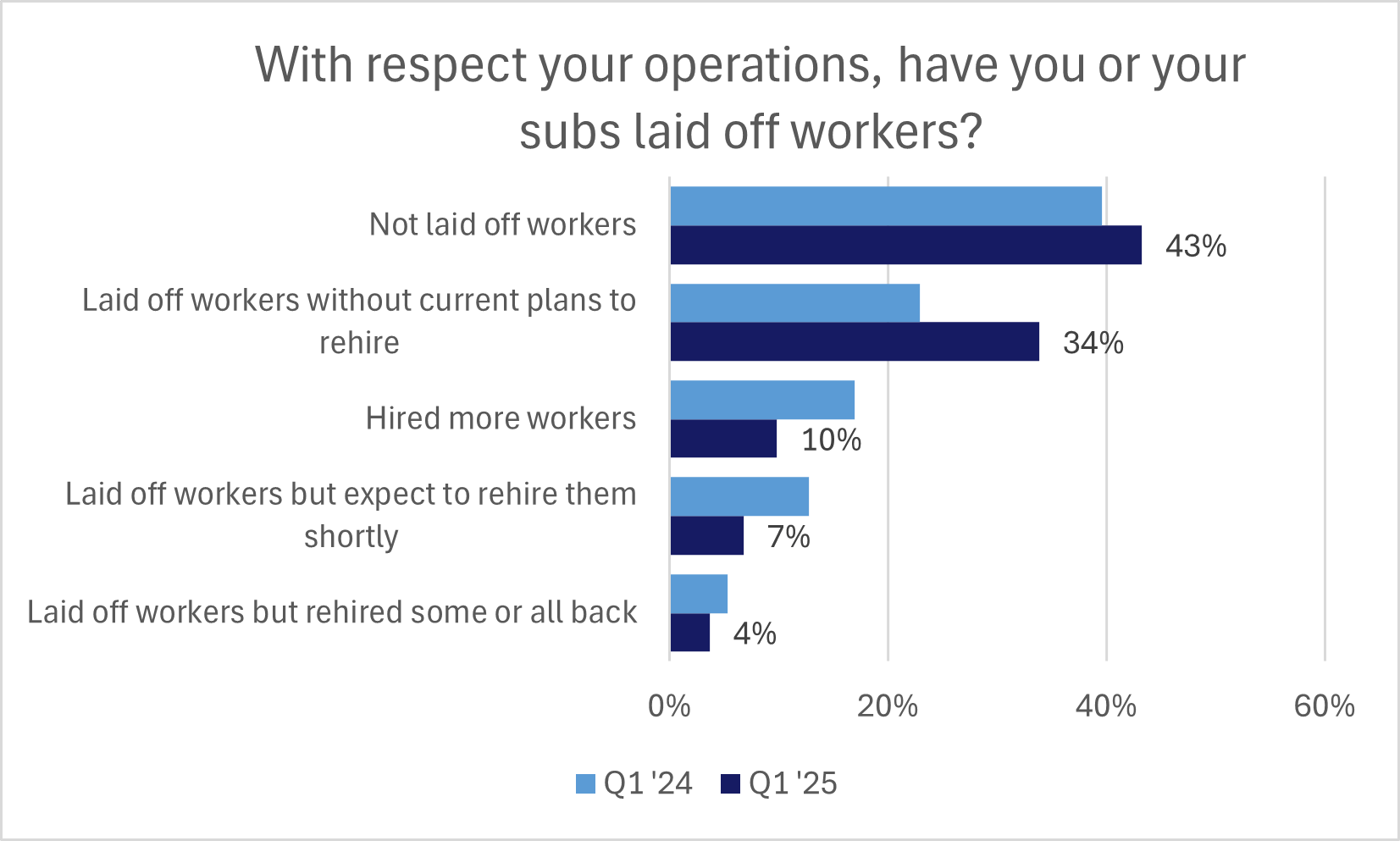

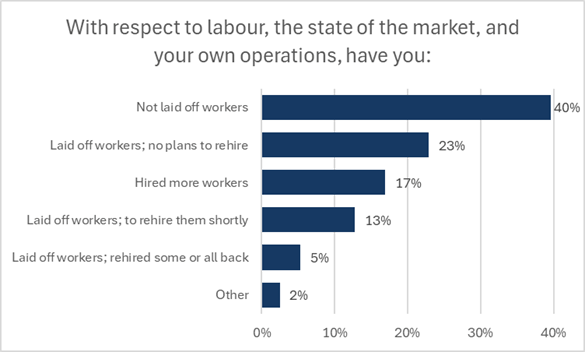

- CHBA remains concerned about the risk that the global trade shock will lower economic growth in Canada and weaken new home buying demand further. While builders prioritized keeping staff through the period of high interest rates, Q1 shows signs that a lack of sales has begun to necessitate layoffs. While 43% have still not laid off workers, 34% have, with no immediate plans to rehire, a proportion that is 11 percentage points higher than the response rate from a year ago.

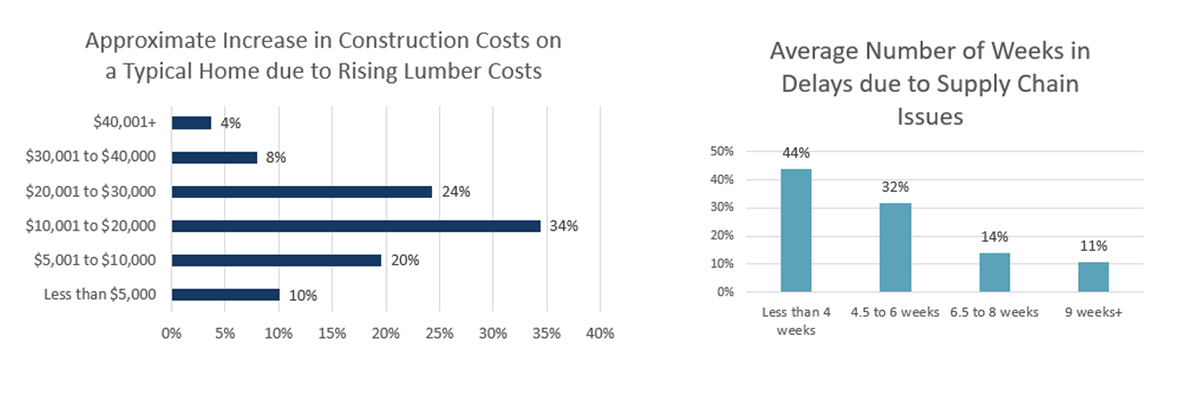

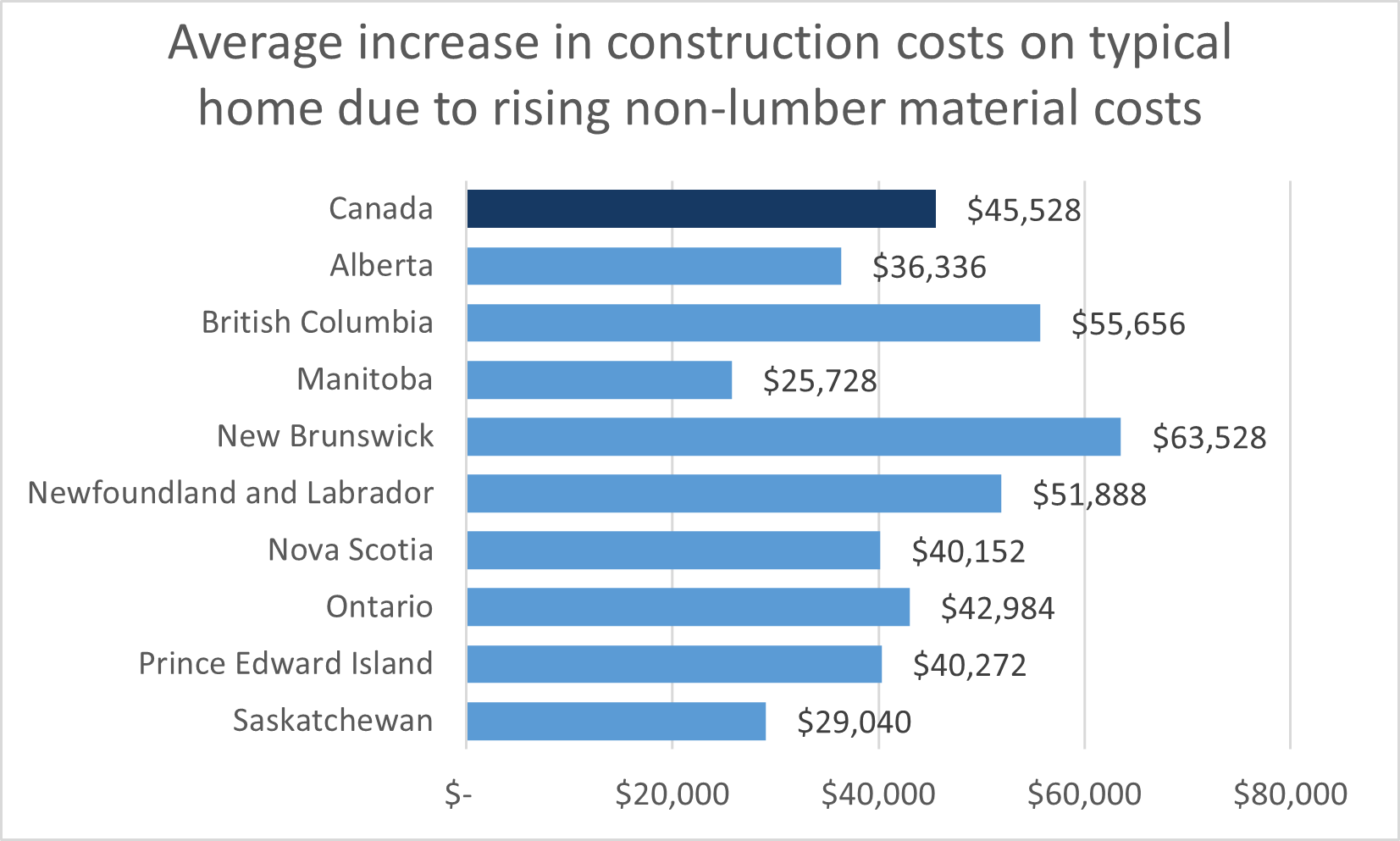

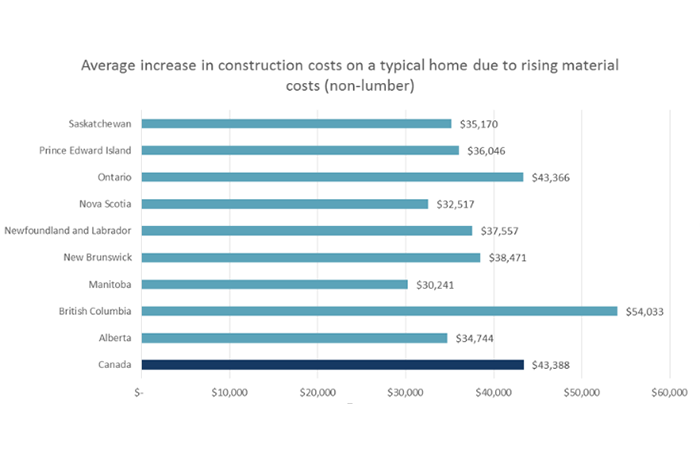

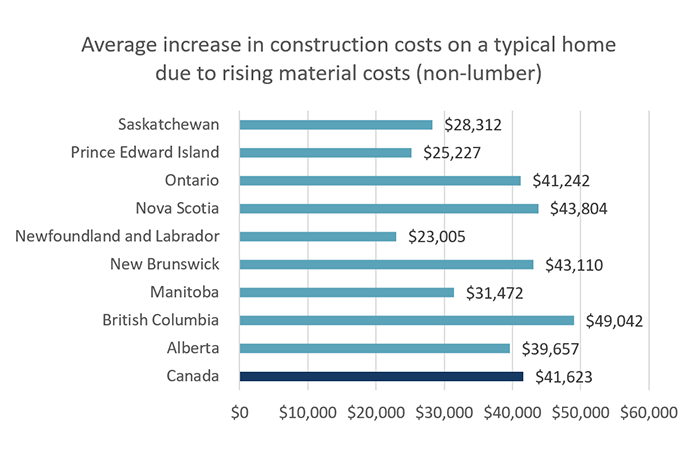

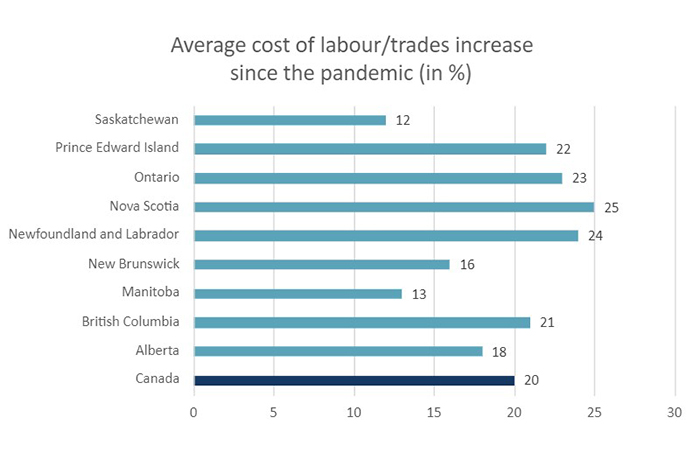

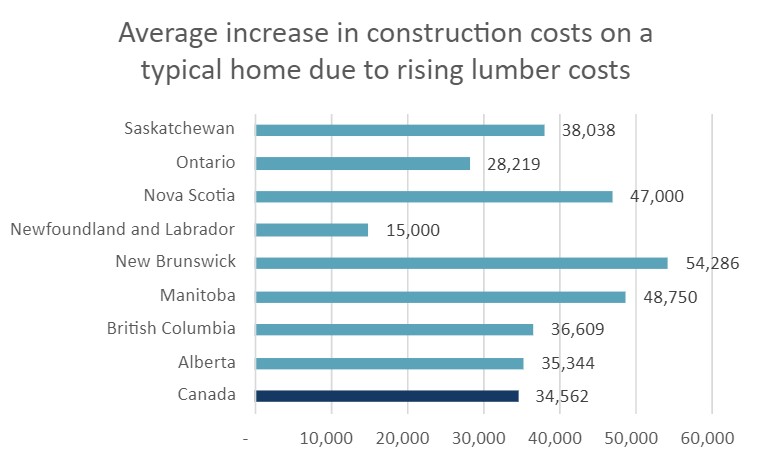

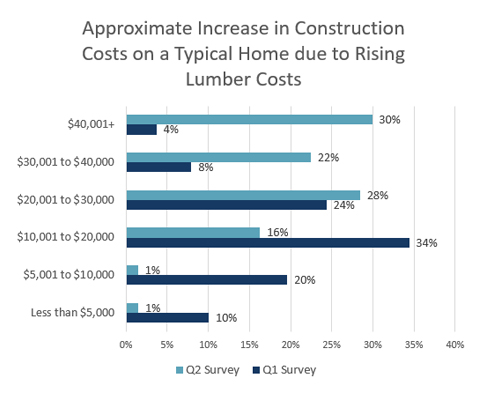

- The rapid and compounding rise in building costs have also worked against affordability, which will be exacerbated by tariffs directly on building materials. Builders were again asked to estimate the increase in cost of non-lumber construction materials over the past year. Based on this, the average non-lumber material cost to build a 2,400 square foot home has risen over $70,000 since the start of the pandemic in 2020. When including cumulative lumber cost increases, total material costs have risen by nearly $98,000 to construct a 2,400 square foot reference home relative to early 2020.

An explanation of CHBA's methodology for the HMI is below.

Conducted on a quarterly basis, the CHBA survey asks an expert panel to rate market conditions for the sale of new homes at the present time and in the next six months as well as the traffic of prospective buyers of new homes. Each variable allows the respondent to rate conditions as either “Good”, “Fair” or “Poor” or in the case of the traffic of prospective homebuyers “High/Very High,” “Average,” “Low/Very Low.” Each of these three variables creates a component index and the HMI is an average of the three component indices:

Component Indexᵢ = (% of Good responsesᵢ - % of Poor responsesᵢ +100)/2

HMI = 0.6xPresent + 0.1xFuture + 0.3xTraffic

The final number is weighted to ensure it is representative of CHBA’s membership by geographical location. The provincial weights leveraged 2024 Statistics Canada housing starts data for the breakdowns of single and multi-family markets to create the proportions of the single-family and multi-family markets in each province. This allows CHBA to create an accurate provincial representation while also taking into consideration that each province has very different single-family and multi-family proportions. Each local Home Builders’ Association (HBA) is also weighted to ensure proper representation by builder size (I.e., small/medium and large). In some cases, where local breakdowns for HBAs are not available, those HBAs are not weighted. The provincial weights are developed in a way to ensure the sample size is representative of the overall population of CHBA's membership of builders. The special questions presented above are only weighted at the provincial level.

For the Q1 2025 results, an online survey was conducted by CHBA from March 12th to April 4th, 2025, using CHBA's panel of builders. Some builders elected to speak to both the single and multi-family builds, resulting in 196 unique responses. Respondents from 36 different local HBAs participated in this survey.

CHBA’s HMI is modelled on that of the National Association of Home Builders (NAHB) in the US. The NAHB-Wells Fargo Housing Market Index is based on a survey of single-family builders that the NAHB has been running every month since 1985. CHBA is leveraging the NAHB's weights as the basis for CHBA’s HMI weights (see formula above). This is to ensure that CHBA is placing more weight on the Present conditions question. As CHBA collects more data, it is planning on developing weights for each of the component indices discussed above that will allow us to maximize the correlation with Canadian housing starts six months into the future.

Panel

The panel is made up of builders from constituent associations to ensure representativeness across Canada. Working together with the association’s local and provincial Executive Officers, CHBA was able to build a panel that is reflective of membership in each region. To ensure it remains up to date, CHBA is continually refreshing the panel. The HMI is weighted to ensure the panel is representative by both geographical location (i.e., national, provincial and local) and size (i.e., small, medium and large). For some smaller home builder associations (HBAs), the sample is not weighted. In those cases, CHBA leverages the HBA’s expertise to ensure the sample is representative of the region. Single-family includes single-detached homes, semi-detached homes and row (townhouse) homes. Multi-family includes stacked townhouses, duplexes, triplexes, double duplexes and row duplexes, and low and high-rise apartment buildings.

.png)

Archive

- Single-family builder confidence was 25.1 in the fourth quarter of 2024. This is a decline of 2.3 points from the previous quarter and is just 0.5 of a point above the index’s all-time low of 24.6 recorded a year ago.

- 56% of single-family builders rated current selling conditions as Poor. The majority have given this rating in four of the past five quarters.

- With respect to expectations for sales over the next six months, builders maintain some optimism for improvement with 52% rating their expectations for conditions to be Fair. 32% still expect conditions to be Poor over the near future.

- Ratings of sales office traffic and potential buyer inquiries remains weak. 70% rate their level of traffic as Low or Very Low. Only 2% of the survey respondents rated traffic as High or Very High.

- Comparatively, the NAHB/Wells Fargo HMI for US single-family builders recorded an average score of 45 in the fourth quarter. While still pessimistic, the balance of builder views is far closer to neutral than in Canada.

- Regional differences persist in the four regions tracked by the survey. Builder sentiment in Ontario reaching an abysmal 11.3, reflecting near universal current sales pessimism in the province. However, this quarter was marked by British Columbia’s sharp decline in sentiment for single-family sales, falling below that of Ontario for the first time since 2021, by reaching a score of 10.5. In contrast, builder sentiment in the Prairie Provinces was 48.2, which is 18.8 points higher than recorded a year ago. Sentiment in Atlantic provinces fell for a third consecutive quarter and recorded a neutral reading of 44.9.

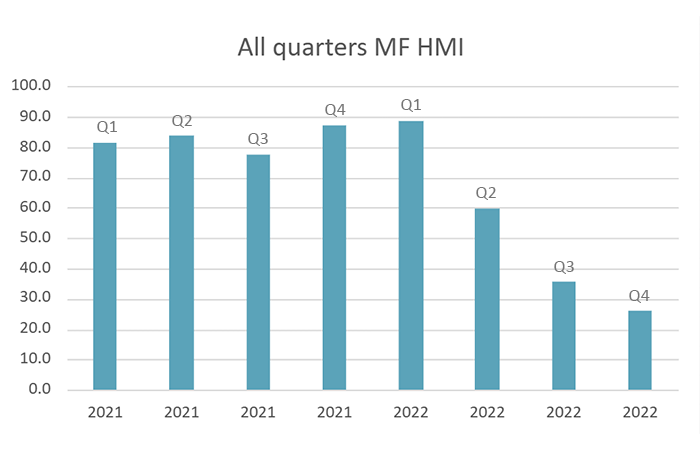

- The multi-family Housing Market Index result was 22.0 in the fourth quarter of 2024, falling 6.5 points from the previous quarter and 7.1 points from Q4 2023. Unfortunately, this quarter was a new record low, surpassing Q4 2022’s score of 26.0.

- A record-high 60% of builders rated current multi-family selling conditions as Poor, a 7-percentage point jump over the fourth quarter of 2023.

- 50% of builders reported their expectations for sales over the near future to be Fair, while 39% expect conditions to be Poor.

- The drop to a record low in the multi-family HMI this past quarter was the result of responses to sales office traffic and sales inquiries. 81% of respondents rated traffic and inquiries as Low or Very Low and lowered the traffic sub-index to unprecedented weakness.

- The Ontario multi-family HMI was 6.2, a new all-time low, down from 21.3 at this time last year and from an all-time high of 90.7 in Q4 2021. No builders in Ontario gave a rating of Good or High/Very High. British Columbia recorded a score of 25, progressively lowering from 42.9 in Q1 2024. The Prairies Provinces recorded a score of 53.7, notably falling from scores of 73.2 in Q2 2024 and 64.3 in Q3 2024.

The results from these questions allow CHBA to better understand what is driving change in builder sentiment as well as monitor current industry issues.

- The Bank of Canada delivered a fifth consecutive rate reduction in December, while the survey was in field, totalling 1.75 percentage points of reductions to short term interest rates since June. Builders were again asked if the BoC’s reductions influenced their expectations about future sales. 34% stated that rates need to fall further before they would it would give them reason to raise their outlook. While there was an initial drop in fixed mortgage rates in Q4 2023, average fixed mortgage rates fell about 0.8 percentage points over the second half of 2024 and kept the mortgage stress test above the default 5.25% Minimum Qualifying Rate. 31% of builders said they would need more time to assess how this impacts their outlook, as the mortgage offerings adjust with the longer-term bond yields. 23% of builders said Yes, it did improve their sales outlook, but this proportion was down from the previous two quarters.

- While national sales conditions remain weak, regional difference highlighted in builder sales sentiment will also extend to construction activity. Most builders state that the interest rates and general economic conditions are still restricting their starts to some degree. Responses from builders stating that interest rates are not restricting their construction came primarily from Prairie and Atlantic province builders, where pre-existing affordability was and continues to be more conducive to sales.

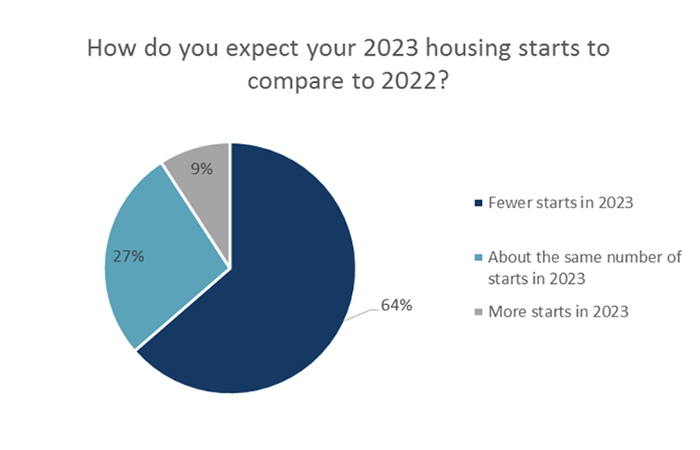

- The majority of respondents stated that they had fewer housing starts in 2024 than they did in 2023. On average these builders stated they reduced their starts by 50% relative to 2023. Note that this does not account for the magnitude of change in starts. Out of the builders that stated they had more starts in 2024, the majority were based in the Prairie Provinces.

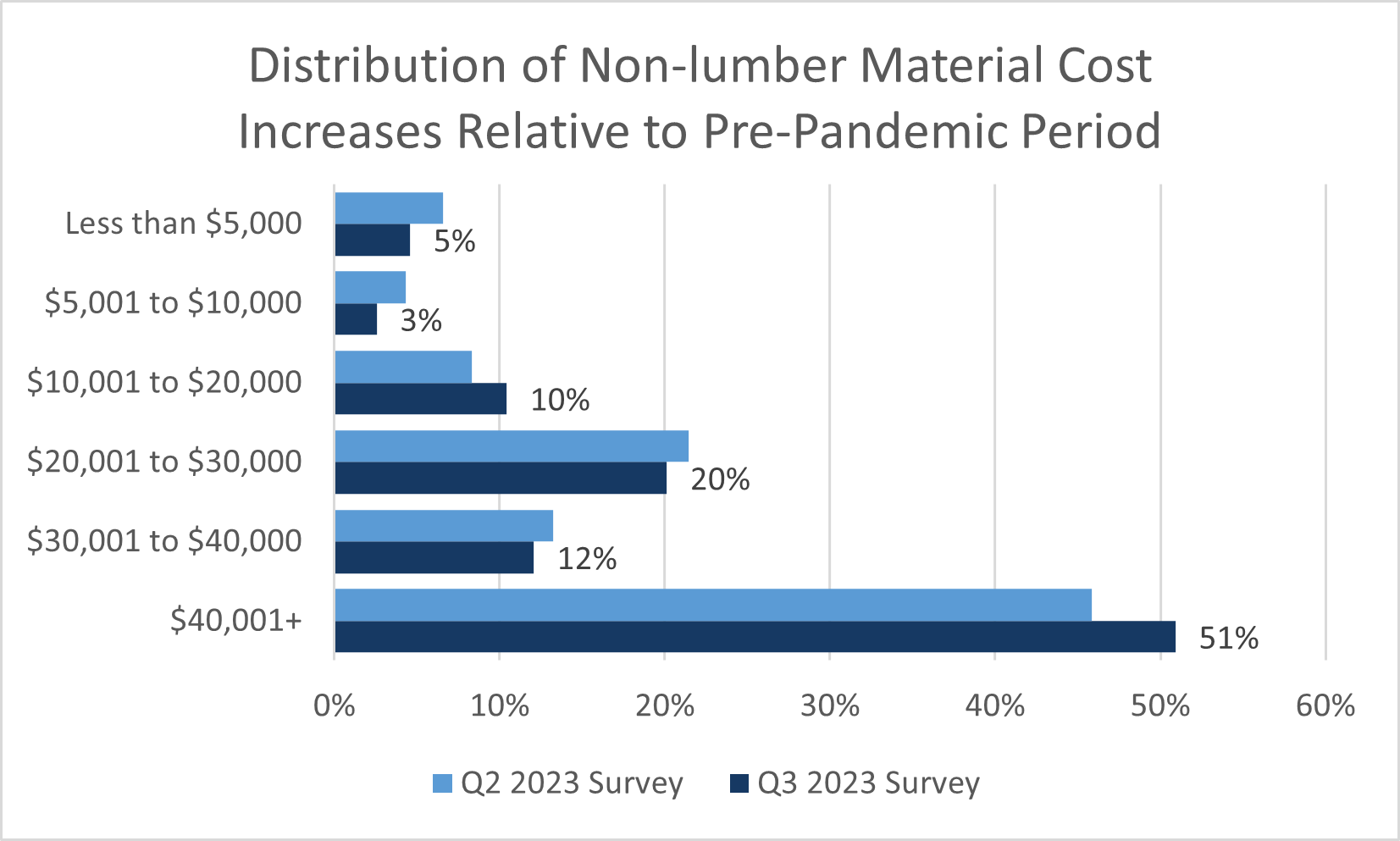

- -To continue monitoring the escalation of construction costs, builders were asked about their non-lumber material costs relative to a year ago based on the most typical home they build. Based on the average of responses, the price increases of materials excluding lumber have added $36,000 to the cost of constructing a 2,400 square foot home, relative to the end of 2023.

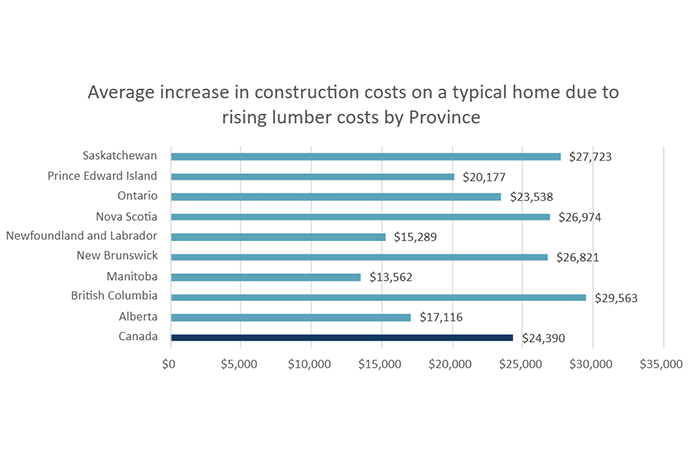

- Softwood lumber prices spiked in Q4, increasing lumber material costs by over $4,200 relative to a year ago and $30,000 since the start of 2020 to the construction cost of a 2,400 square foot home. CHBA remains engaged in policy discourse over the effect of compounding broad based tariffs on lumber and the possibility of additional lumber curtailment.

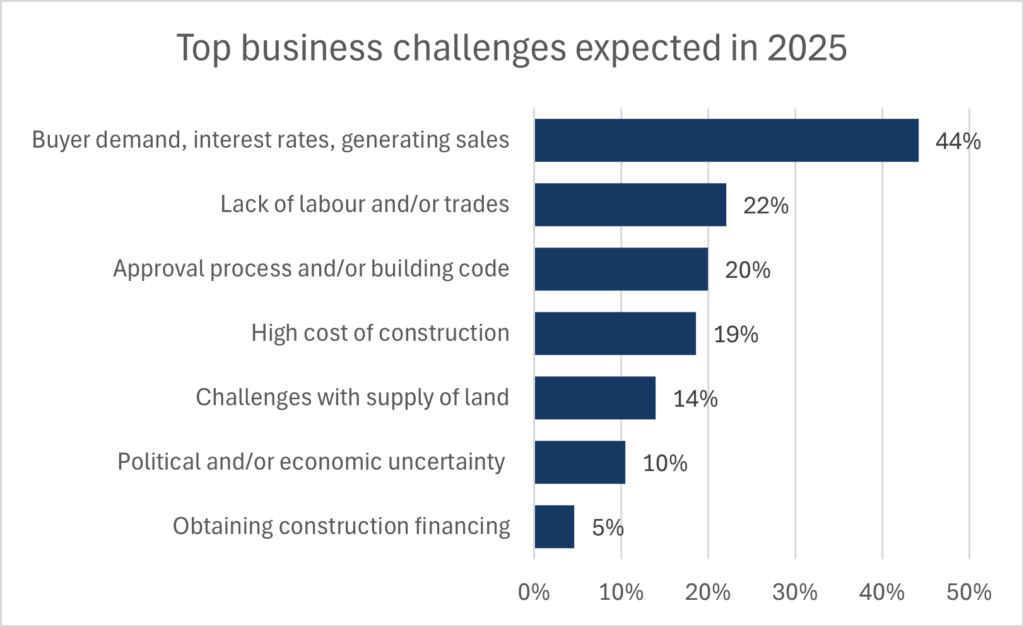

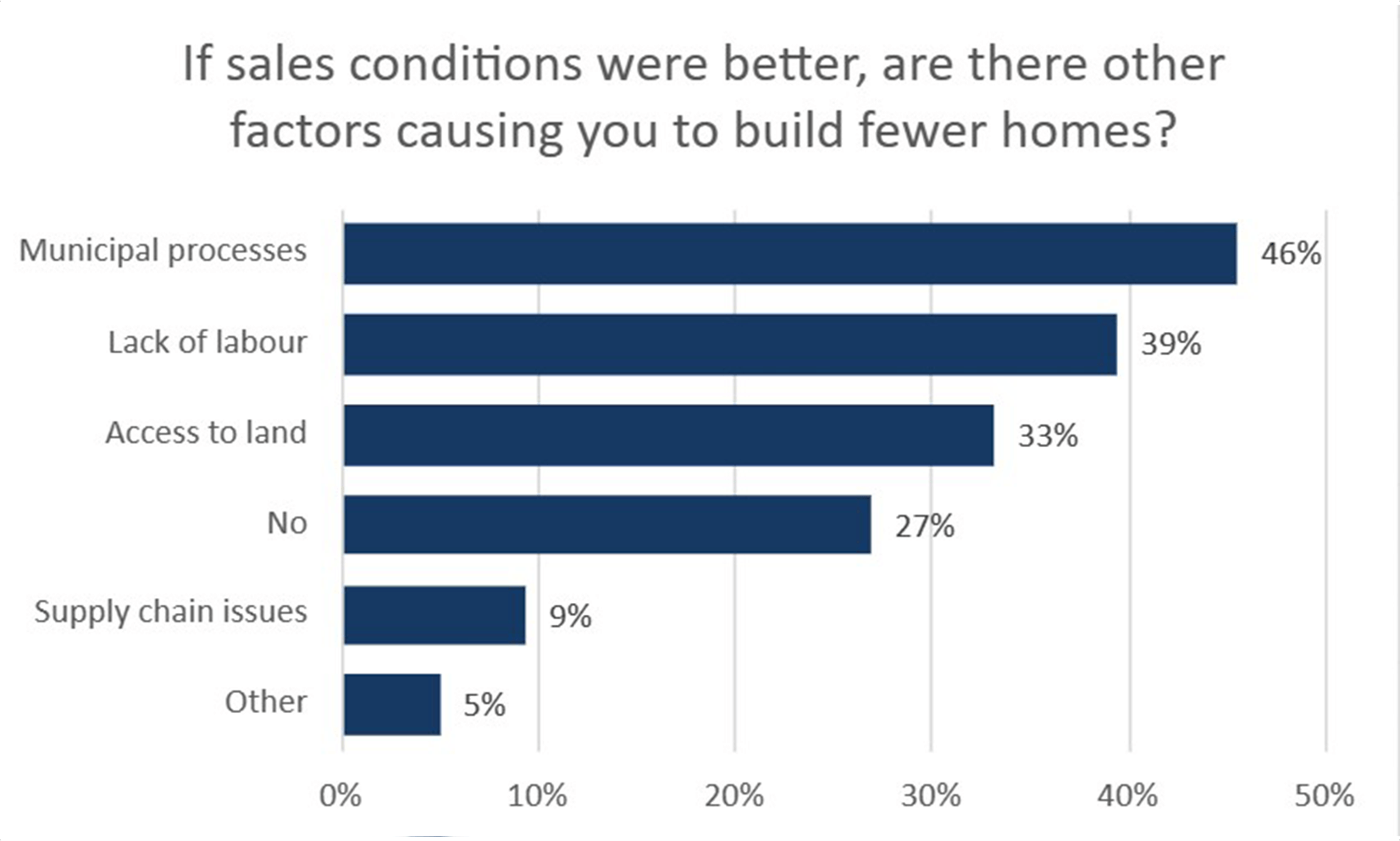

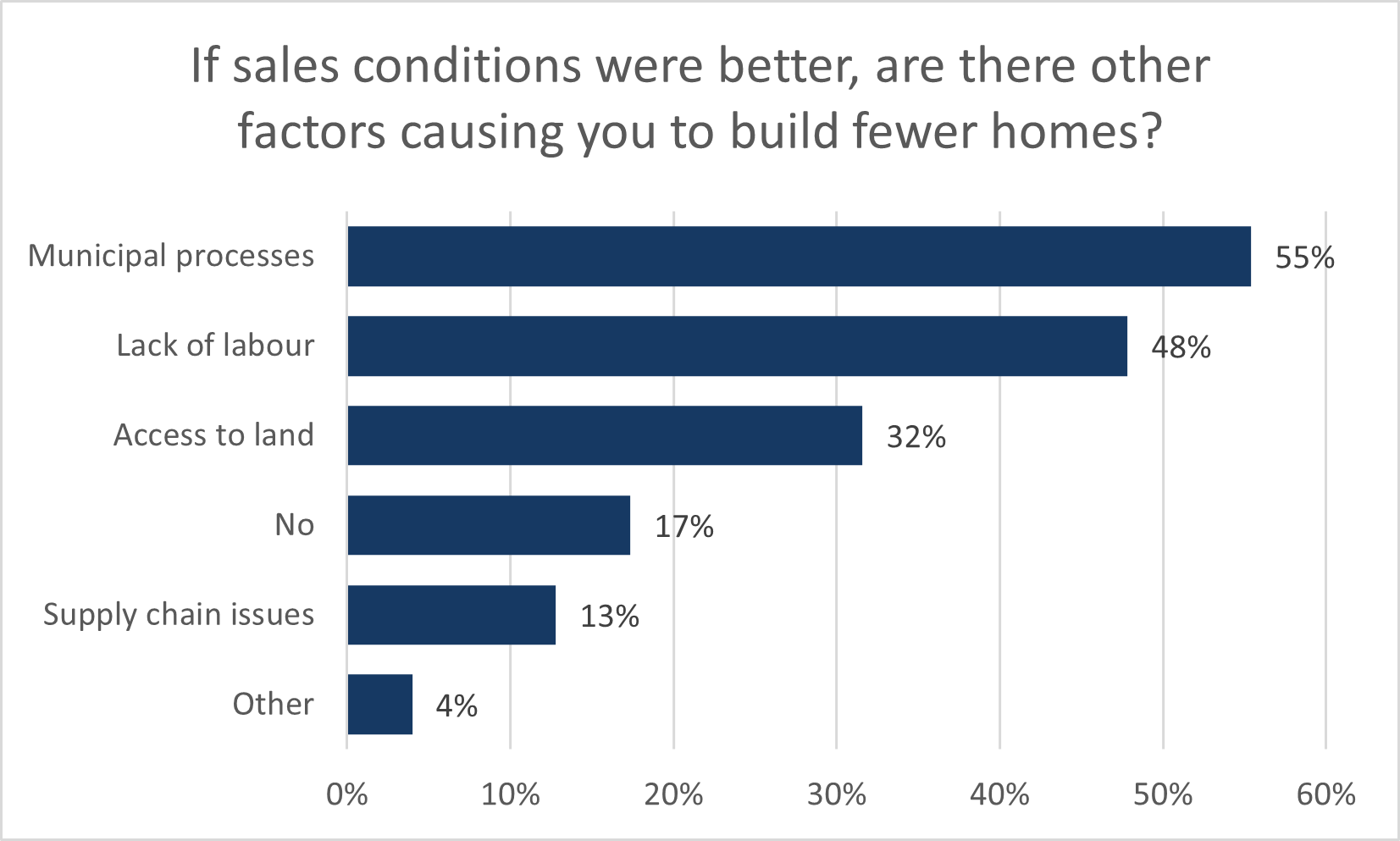

- Builders were asked, without a list to choose, what they expect the top challenge for their business will be in 2025. Comments were categorized into 7 main categories. 44% of builders stated getting their regular flow of sales back will be their top challenge. After this, there was a near-equal proportion of builders mentioning challenges of finding qualified trades, issues with the building approval process or codes changes, and their high construction costs specifically that make sales challenging. 14% of builders stated that issues with obtaining enough suitable lots or obtaining land at a viable price will be a top challenge. For reference, when asked in Q4 2023 about what the most acute issues would be if buyer demand was better, they were: municipal processes (46%), lack of labour (39%), and access to land (33%). Note: The first two issues stated were counted in cases where multiple issues were stated. Since issues related to a lack of sales remain the top issue for 2025, answers regarding the cost of construction being why they continue to expect low sales were recorded separately.

- The single-family Housing Market Index recorded 27.4 in the third quarter of 2024. This is 2.5 points lower than the previous quarter and 6.5 points lower than in Q3 of 2023. The single-family HMI has retrenched to just 1.2 points above its record low of 26.2 recorded in Q4 2022.

- Over 55% of single-family builders rated current selling conditions as Poor. This majority pushed down the present selling conditions sub-index to just 1.1 points above its all-time low recorded in Q4 2024.

- 58% of builders believe that selling conditions over the next six months will be Fair, while 25% still feel conditions will be Poor.

- 65% of single-family builders rated traffic through sales offices and general inquiries were Low or Very low. Furthermore, only one builder in the entire sample rated traffic conditions as High or Very High.

- The US NAHB Single-Family HMI for the third quarter averaged 40. The sentiment score in both Canada and the US has trended down by about 8 points since the first quarter of 2024. Yet Canadian builders have maintained a more pessimistic view going back to mid-2022.

- Regionally, single-family HMI in British Columbia edged down from 17.8 in Q2 2024 to 17.1, reaching a new record low for the second consecutive quarter. The HMI for Ontario builders remains terrible at 14.3 (up marginally from its its record low of 11.6 in Q2 2024) —still indicating abysmal sentiment on sales conditions. Meanwhile, sentiment in the Prairie and Atlantic provinces fell from their marginally optimistic readings to marginally pessimistic readings in the mid-40s.

- The multi-family Housing Market Index recorded 28.5 in the third quarter of 2024. The index declined 4 points from Q2 2024 and 5.1 points from this quarter last year. This is the second lowest multi-family HMI reading on record, after it reached 26 in Q4 2022.

- 47% of multi-family builders rated current selling conditions as Poor and 46% rated conditions as Fair. For the first time, the proportion of builders rating conditions as Good was in the single digits

- 61% of builders rated their expectations for selling conditions over the next six months as Fair. Concerningly, this sub-index has softened in the last two quarters.

- 57% of builders noted that sales office traffic and inquiries were Low or Very Low. Similar to the single-family HMI, just one builder across the country rated traffic as High or Very High.

- Ontario continued to report lowest sentiment out of the four regions CHBA tracks, with a regional HMI of 12.5, nearly as bad as the record low of 11.6 recorded in the previous quarter. The Multi-family HMI in British Columbia was 29.3, a new record low for the province. Meanwhile, the multi-family HMI in the Prairie provinces was 64.3 in the third quarter, it is down from a score of 73.2 in the previous quarter.

The results from these questions allow CHBA to better understand what is driving change in builder sentiment as well as monitor current industry issues.

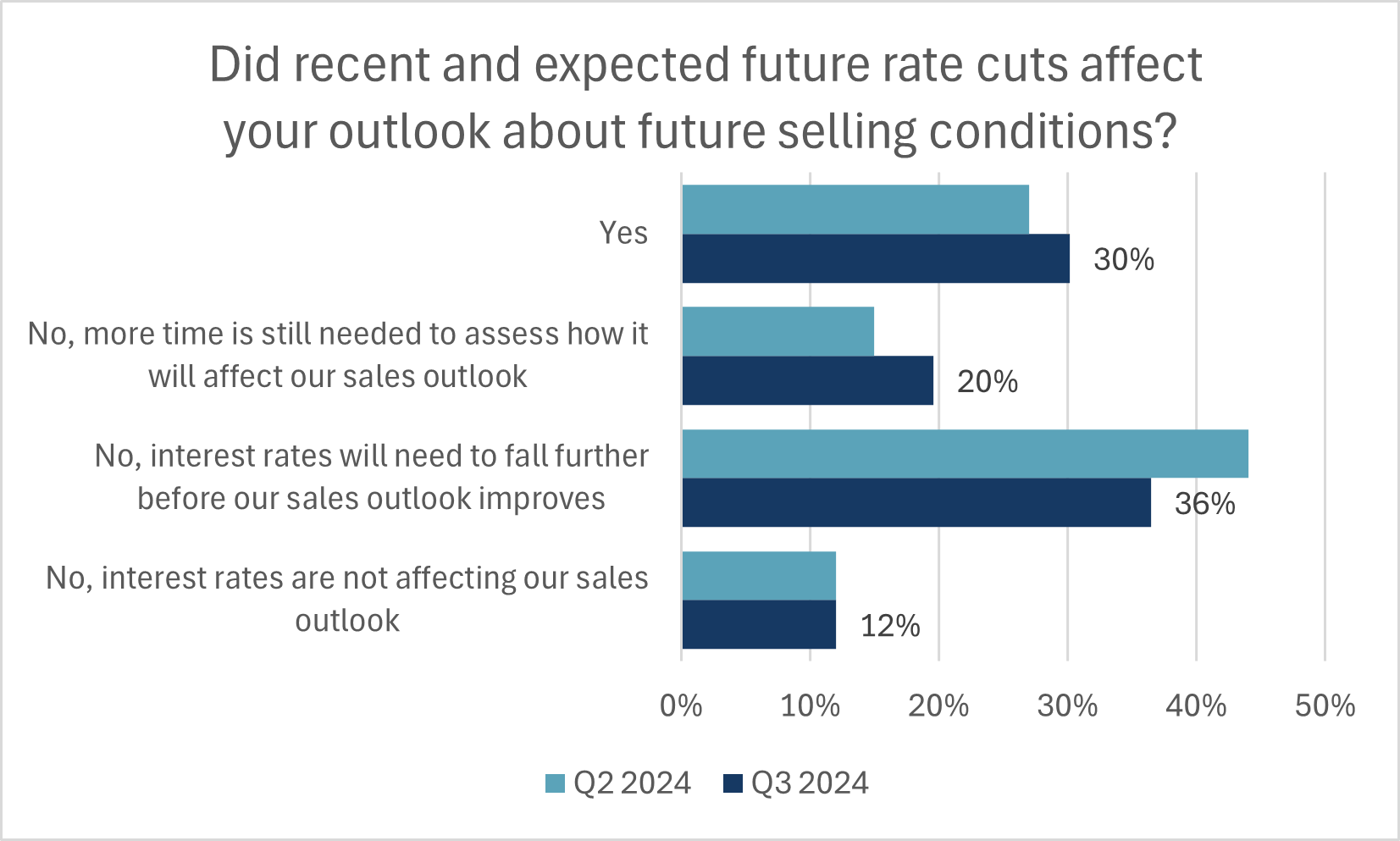

- The Bank of Canada cut its policy rate two additional times in the third quarter. Builders were again asked if these cuts, along with expectations for future rate cuts, materially influenced their view on future sales conditions. 30 percent said it did. But as with the previous quarter, the largest share of builders, at 36%, stated that it did not and that rate will need to fall further, with another 20 percent saying more time is needed to assess impactds on their outlook. Given that most mortgage originations remain fixed-rate, which are slower to adjust, and that mortgage rates still face issues with the stress test, it is not surprising that the marjority of builders remain dubious.

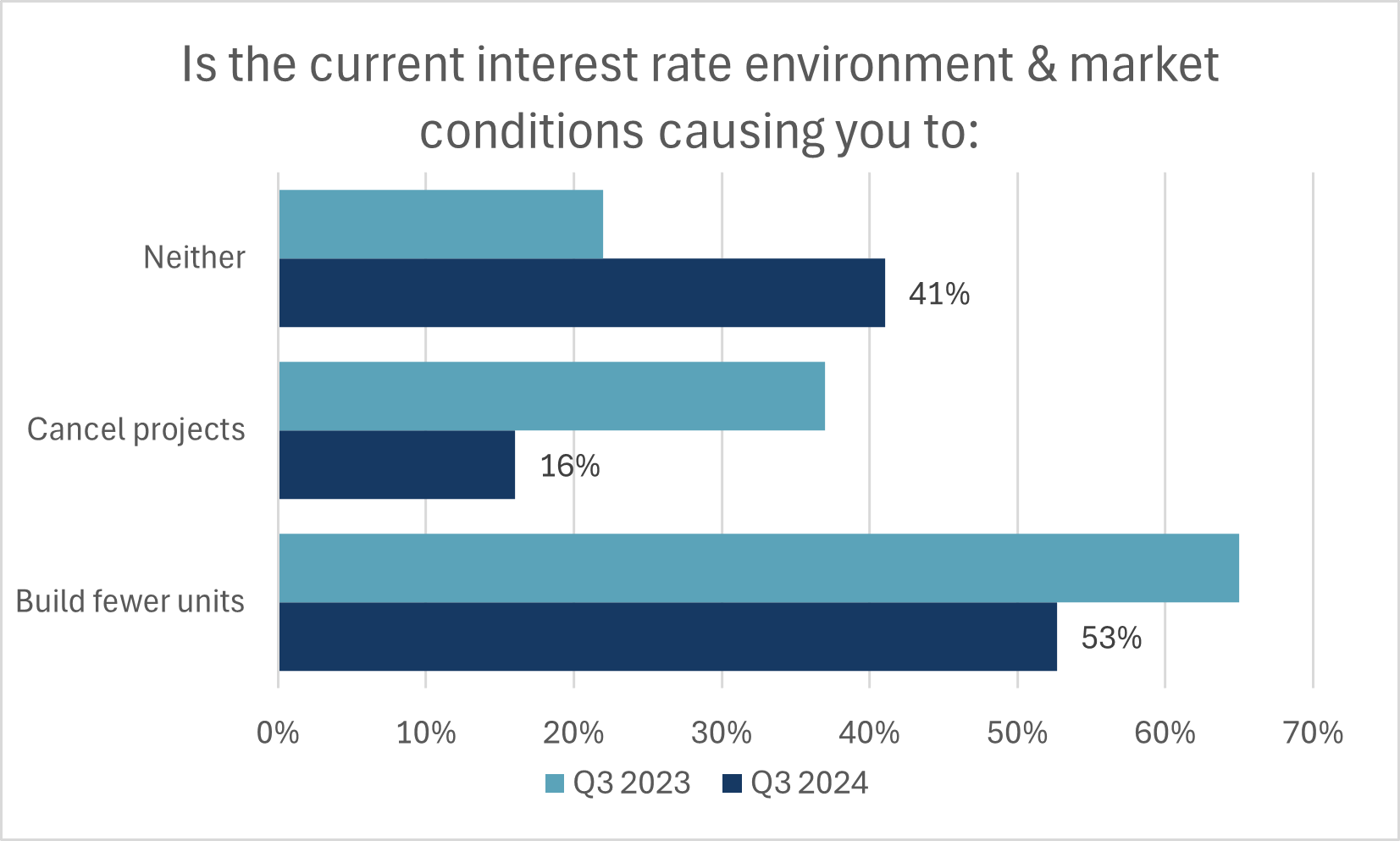

- While sales conditions across the country remains weak, regional variations in sales strength have emerged. This has reduced the proportion of builders reporting that the current interest rate environment is hampering their operations relative to a year ago, but is regional – regions with better affordability are seeing a greater impact of lower interest rates, while more expensive markets are finding slightly lower interest rates are insufficient to create a turnaround. Overall, the majority of builders continue to state that the rates for builders and homebuyers are reducing their quantity of starts. Note that this question does not measure the magnitude of the interest rate impact on starts.

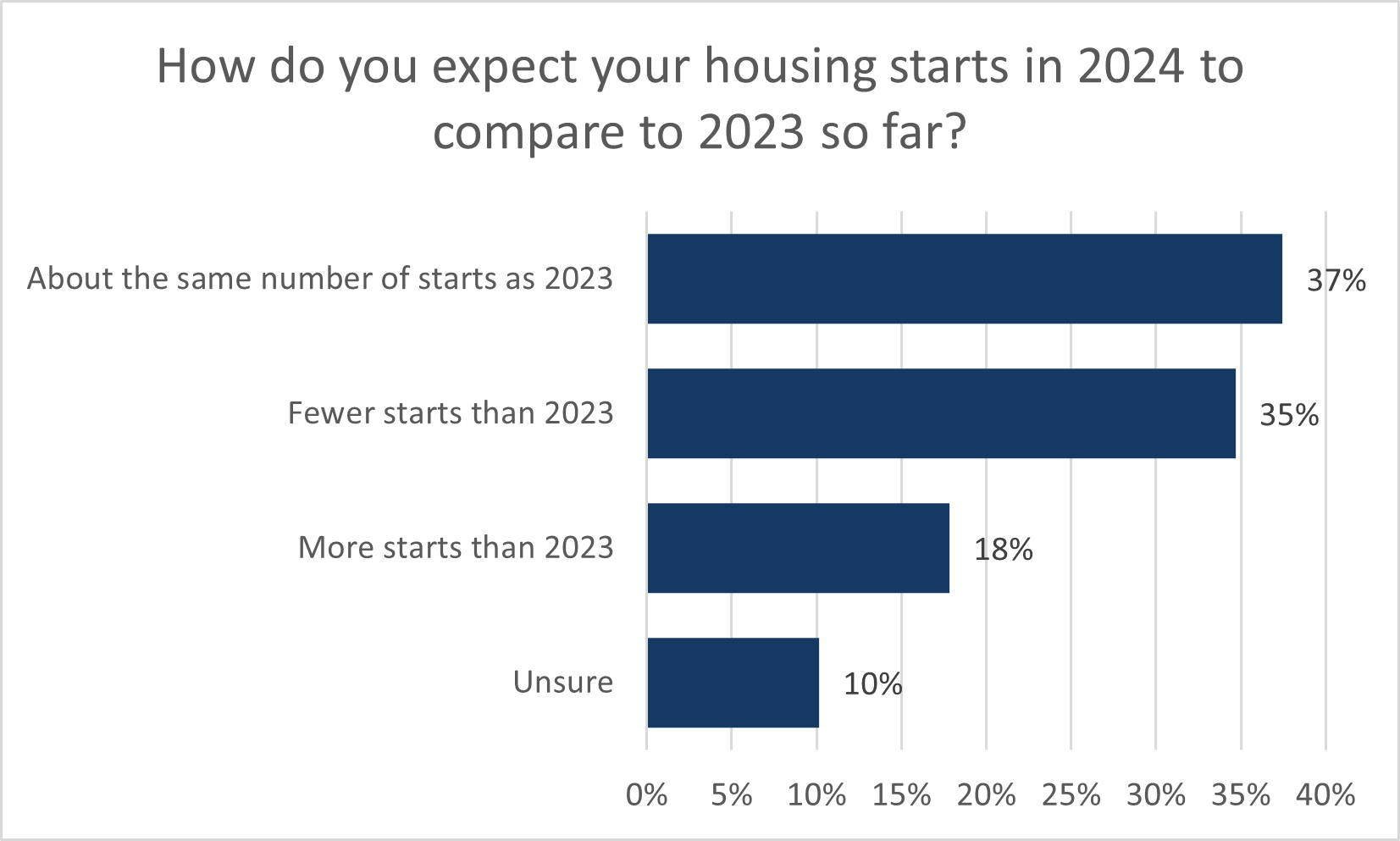

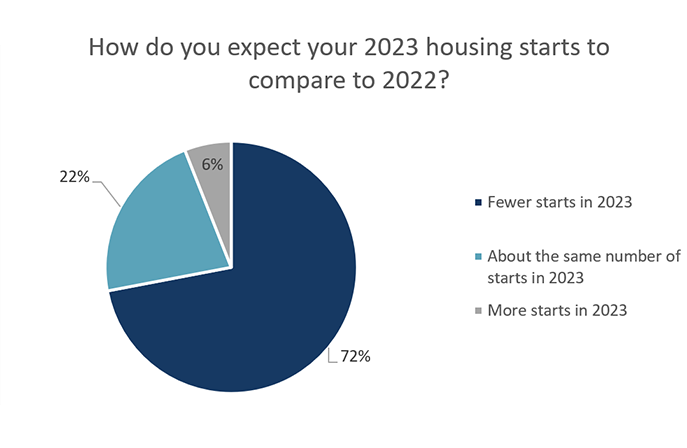

- Half of builders continue to expect to have fewer starts this year compared to 2023. Of particular concern is that this group contains many small and medium sized builders who report they will have far fewer starts this year. On average this group expects to have 52% fewer starts relative to 2023. 36% of builders expect starts to be about the same, while on 15% expect higher starts. Some builders did comment that they are hopeful for a better 2025 spring selling season, which will lead to starts in late 2025 or the following year.

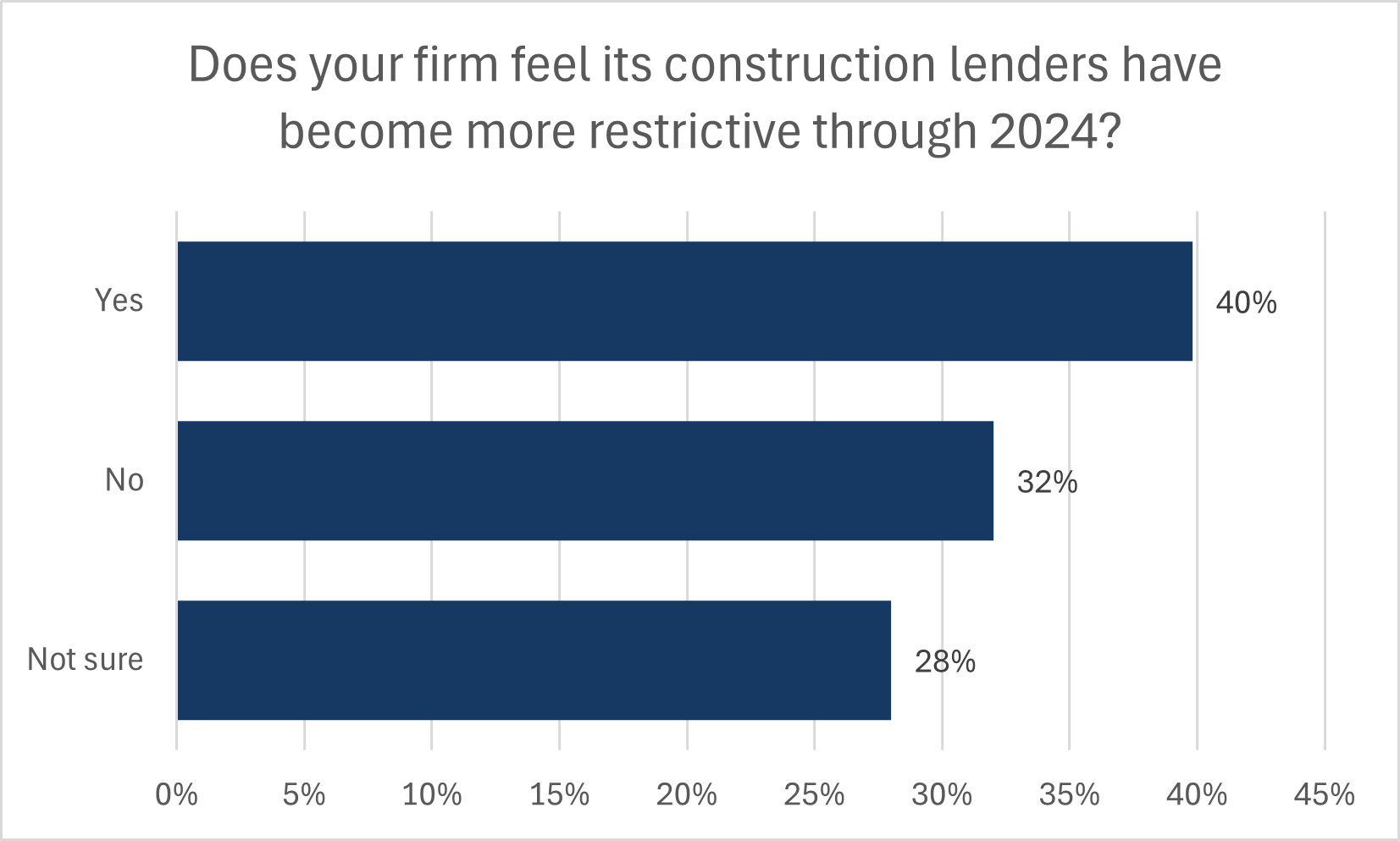

- While credit conditions have broadly eased with policy rate cuts, it is less clear for builders accessing loans for construction. 40% said it is more difficult to work with lenders in 2024, a function of other tightening in lending practice. This is attributable to difficulties in meeting lenders’ pre-construction sales requirements, changes to CHMC multi-family insurance offerings, and appraisers more closely monitoring values of the project. Several builders that were not sure about credit access conditions stated because they have not needed funding this year.

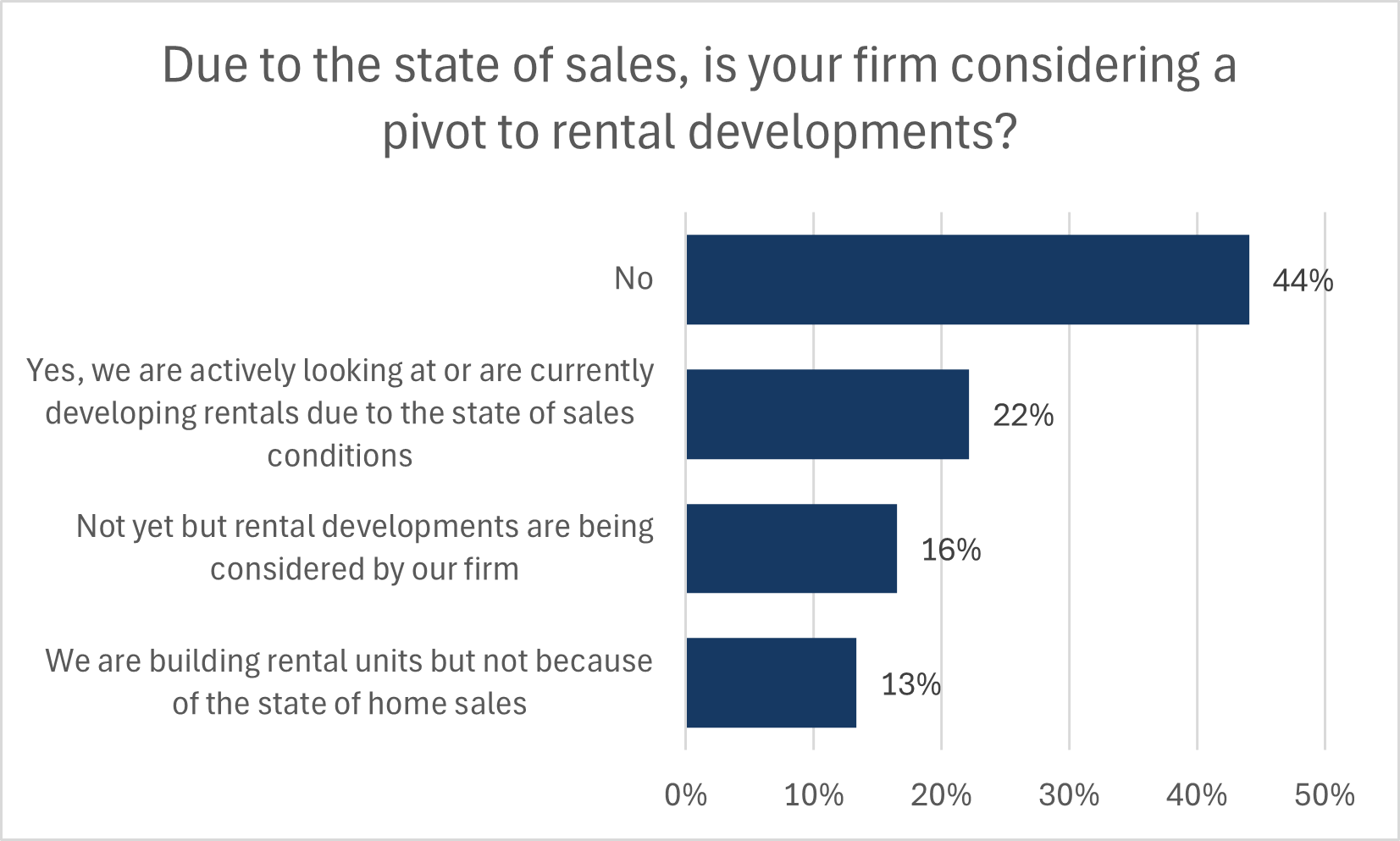

- The extended period of weak sales, along with year-old enhanced rental GST rebate incentive, builders were asked if they are or are considering pivoting to constructing rental units. 22% of builders said that the state of new home sales has led them to develop or actively consider developing rental units. A further 16% stated that this is informally under consideration. CHBA will monitor this trend in future HMI surveys.

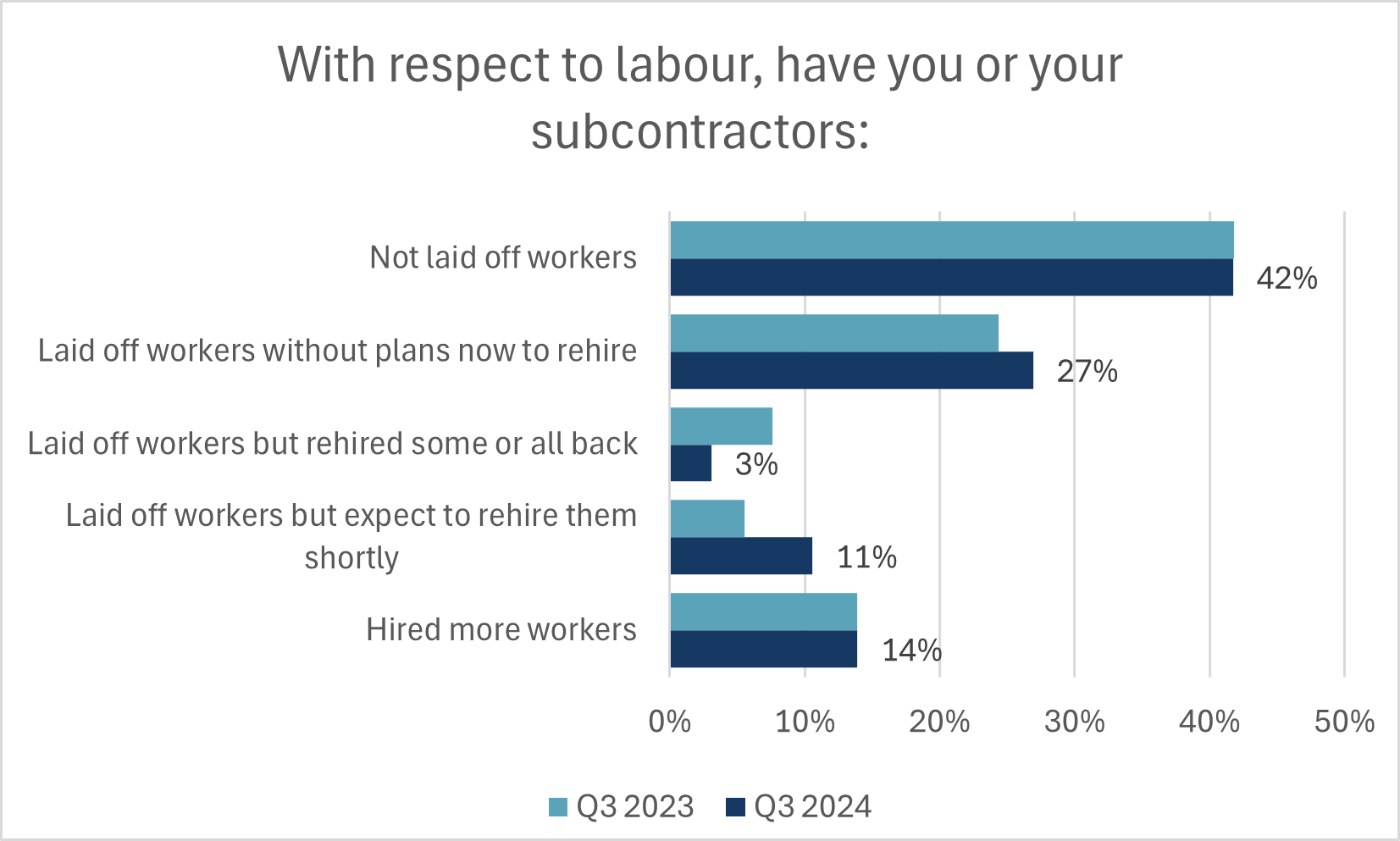

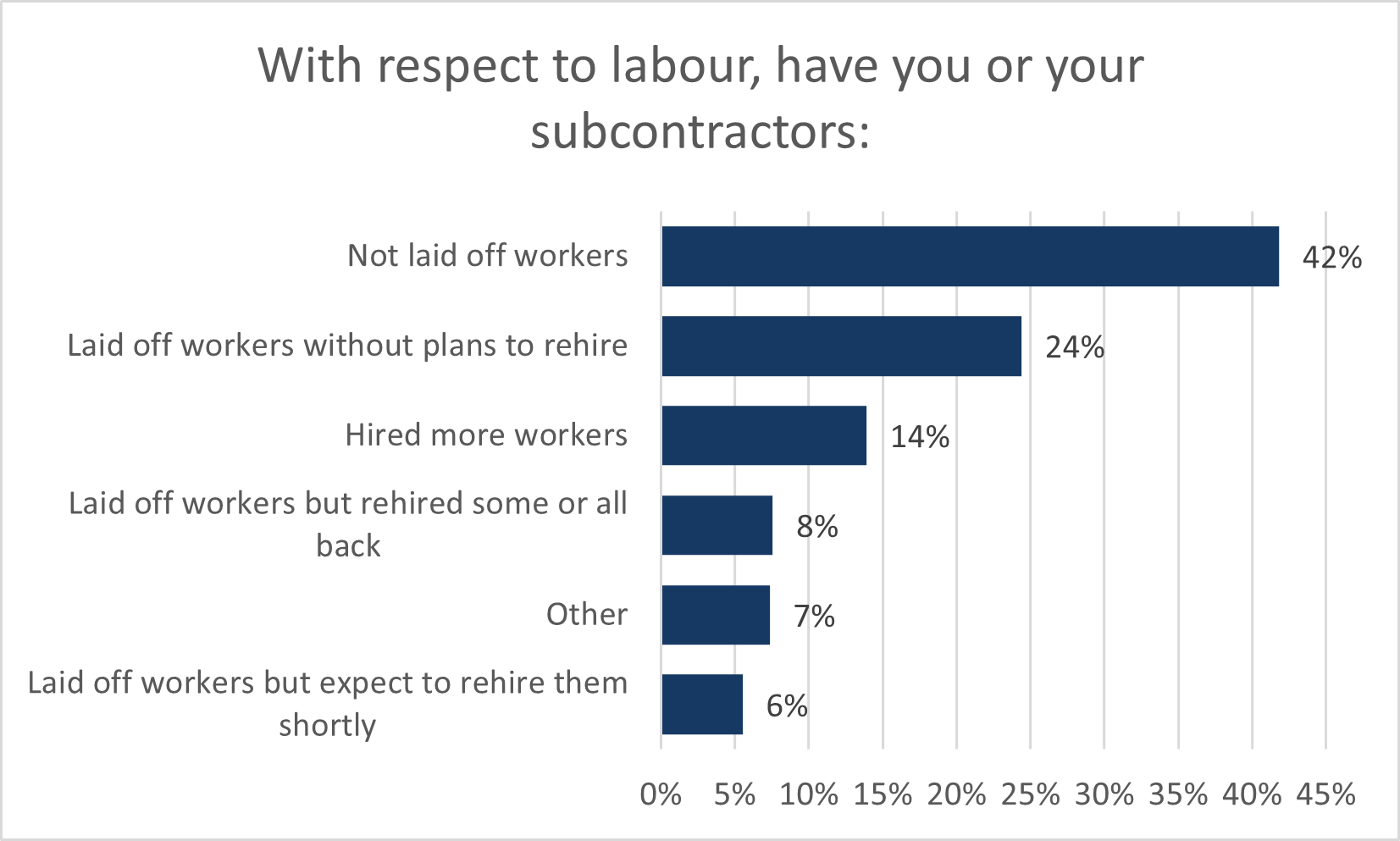

- While past surveys have illustrated that trades access and prices have stabilized relative to their challenges in recent years, the underlying labour shortage in residential construction remains. 42% of builders state they have not laid off workers, partly due to the difficulty in finding a replacement at a time when local market conditions improve. The results of this question were in line with findings from the third quarter survey in 2023.

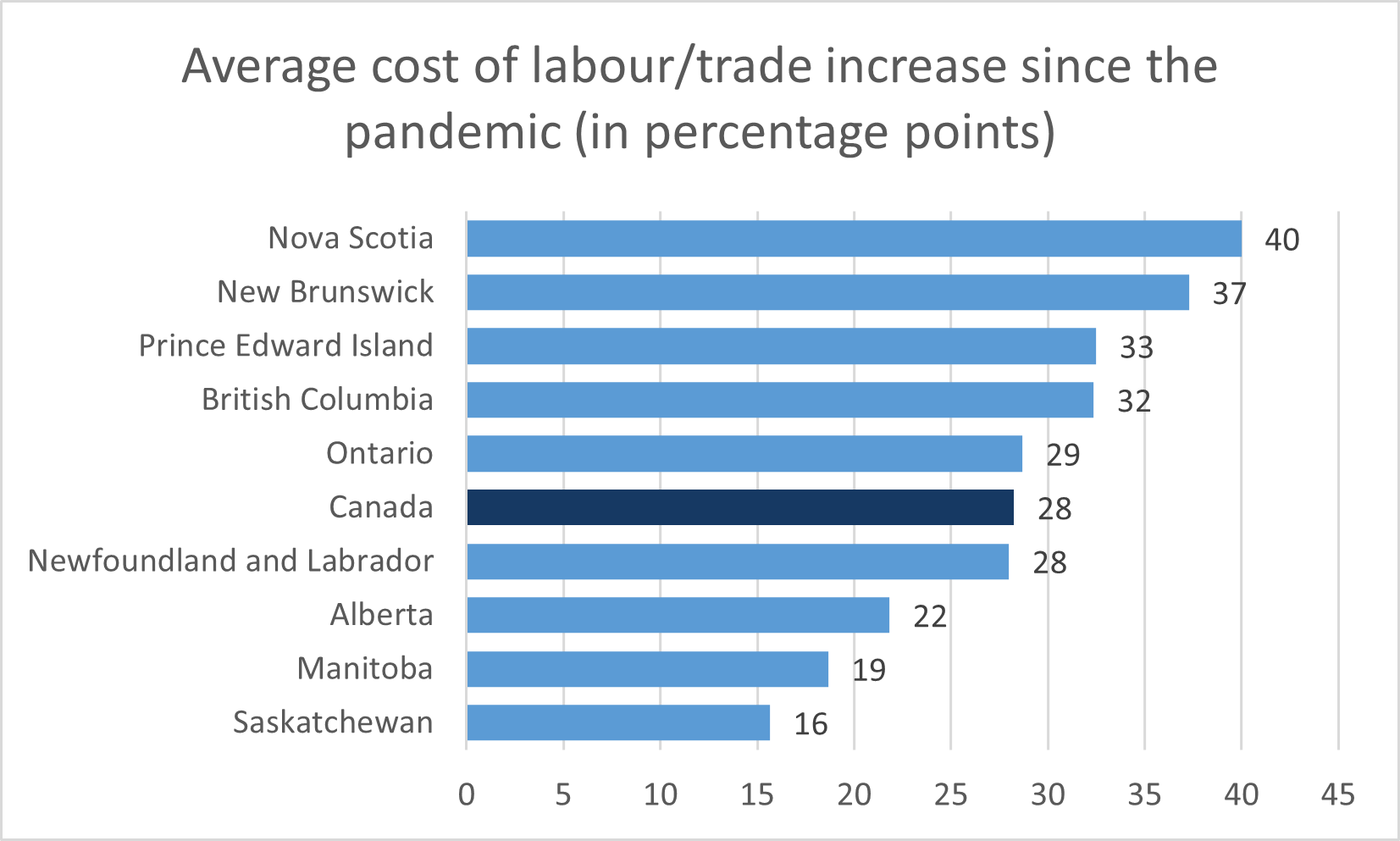

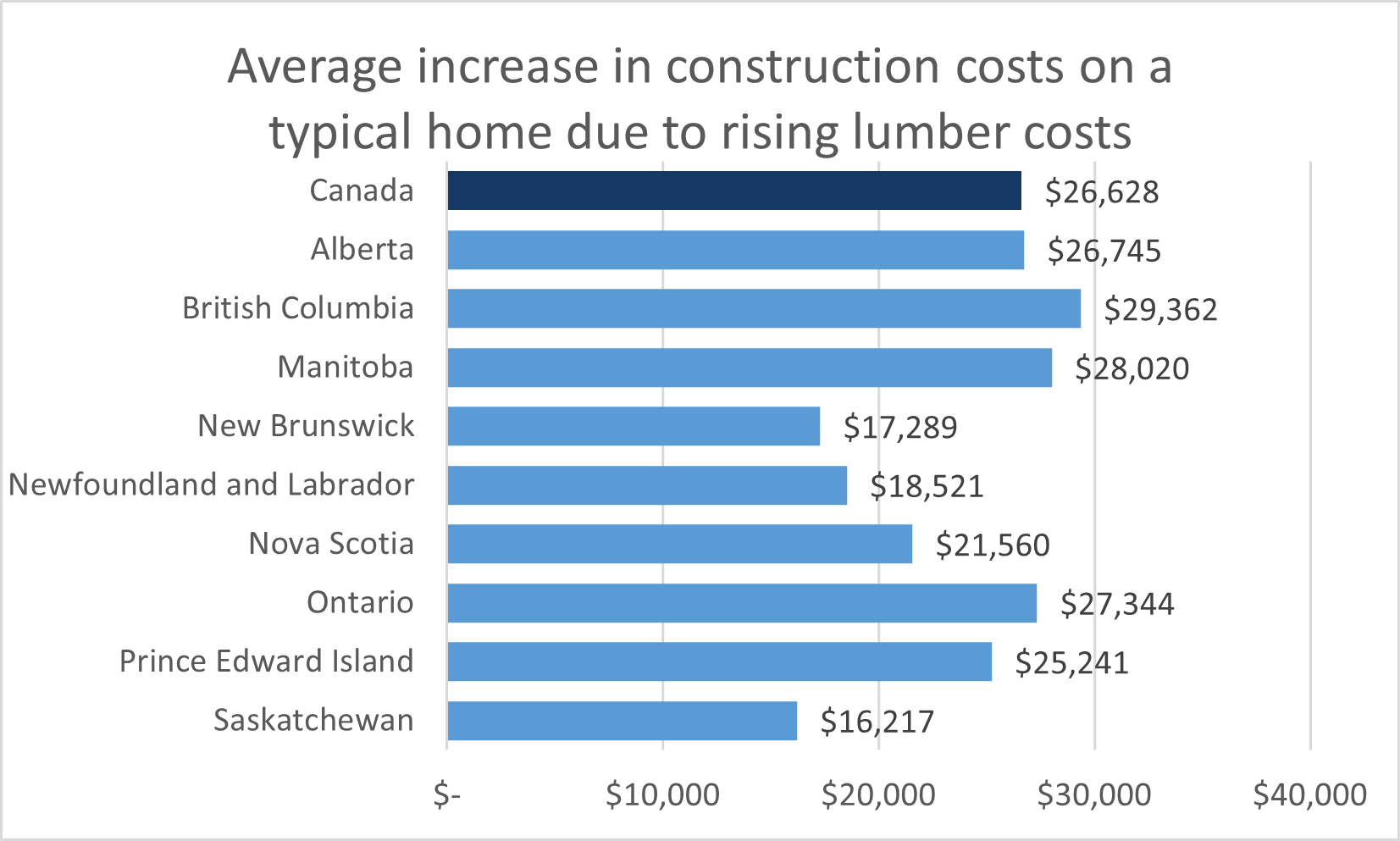

- The average increase of non-lumber materials cost relative to this time last year, as reported by surveyed builders, added an additional $35,270 to the cost of a square foot detached home. Factory gate softwood lumber prices have declined over 2% from a year ago, but this still leaves the lumber cost for the same 2,400 square foot home at over $26,000 more than it was pre-pandemic. Normal rates of inflation for building materials continues to compound the accelerated cost increases from the years prior, further eroding affordability.

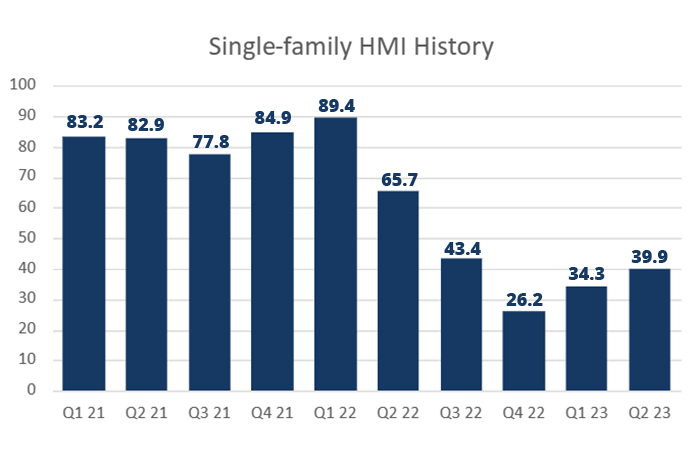

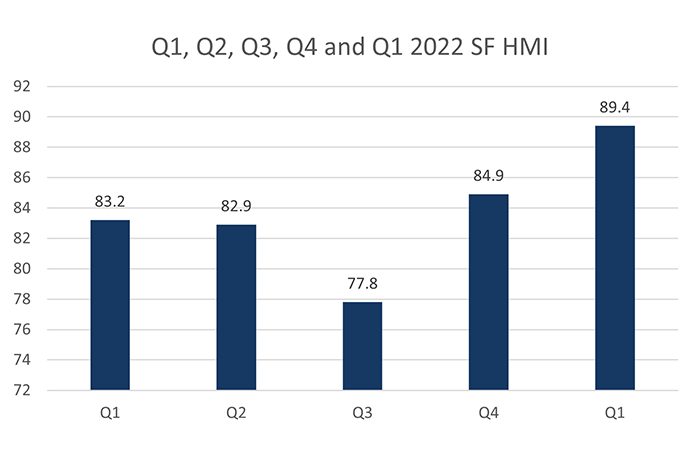

- The CHBA Single-Family Housing Market Index (HMI) continued to reflect builders’ broadly pessimistic views on new home selling conditions, registering a score of 29.9 in the second quarter of 2024. This score is 5 points lower than in the first quarter of 2024 and 10 points lower than in same quarter of 2023. This latest reading is close to the record low of 24.6, in the fourth quarter of 2023. By comparison, the record high was at 89.4 in Q1 2022, when interest rates were still extremely low and before the rate hikes began.

- Since the final quarter of 2022, there are different regional trends in selling conditions sentiment that have emerged. Sentiment held by Ontario and BC have continued their downward trajectory and the single-family HMI in both provinces hit their lowest level ever in Q2 2024 (11.6 in Ontario and 17.8 in BC).

- Over the same 18-month period, sentiment across the aggregated prairie provinces has trended up and breached the neutral sentiment mark of 50 for the first time since Q2 2022. Meanwhile, builder sentiment in the Atlantic provinces has held steady and is modestly positive.

- In the US, the NAHB/Well Fargo single family HMI averaged a score of 46.3 in the second quarter. This sentiment was also down from both a quarter ago and a year ago, albeit not as much as the declines seen in Canada. This is reflected in healthier housing starts in the US versus Canada.

- The present-sales sub-index fell once again, as the majority of builders rated conditions as Poor. With costs continuing to pressure selling prices, the builders experienced another challenging spring sales season. In Ontario, there were no builders that characterized current sales as Good.

- Builders continue to hope for more normal conditions in the future, based on the expected future selling conditions sub-index. 48% of builders rated future selling conditions as Fair. This proportion has roughly held steady over the past year, and points to expectations of falling interest rates and hope that policy changes will come into effect to help conditions.

- Single-family sales traffic remained the weakest sub-index, with 60% of builders rating traffic sales and/or inquiries Low or Very Low. This suggests builders experienced an even slower important spring season relative to the same time last year.

- The second quarter multi-family housing market index was 32.5 – firmly downbeat selling conditions. The index fell 5.4 points relative to the previous quarter and 8.5 points relative to the same quarter a year ago.

- Regional results were similar to the findings of the single-family index. Overall sentiment is at survey record lows in Ontario (11.6) and British Columbia (32.5), with the overall index lifted by sentiment in the prairie provinces, which has remained above 50 for five consecutive quarters.

- The present sales sub-index remained pessimistic, with 48% of builders rating it as Poor. This proportion was a 10-percentage-point increase over both the last quarter and the result from the Q2 2023 survey, underscoring the slow sales conditions. Only 13% of builders gave present conditions a rating of Good, and this small proportion has held steady for four consecutive quarters.

- The expectations for future sales sub-index showed that 42% of builders expect Fair conditions, and an equal proportion rated their outlook as Poor. Notably, the proportion rating a poor outlook rose by 24 percentage points over the previous quarter.

- The sales office traffic sub-index was the lowest of the three. Only single-digit proportions of builders reported traffic levels of High or Very High, which has remained consistent over the past year.

The results from these questions allow CHBA to better understand what is driving change in builder sentiment as well as monitor current industry issues.

- Builders were asked if June’s 25-basis point lowering of the Bank of Canada’s policy rate affected their answer regarding their outlook on future sales over the next six months. 44% of builders said that rates will need to fall further before they adjust how they rate their outlook on sales conditions over the next six months. 27% stated that the cut did affect their outlook, likely related to how it increased confidence if there are additional rate reductions in the months ahead.

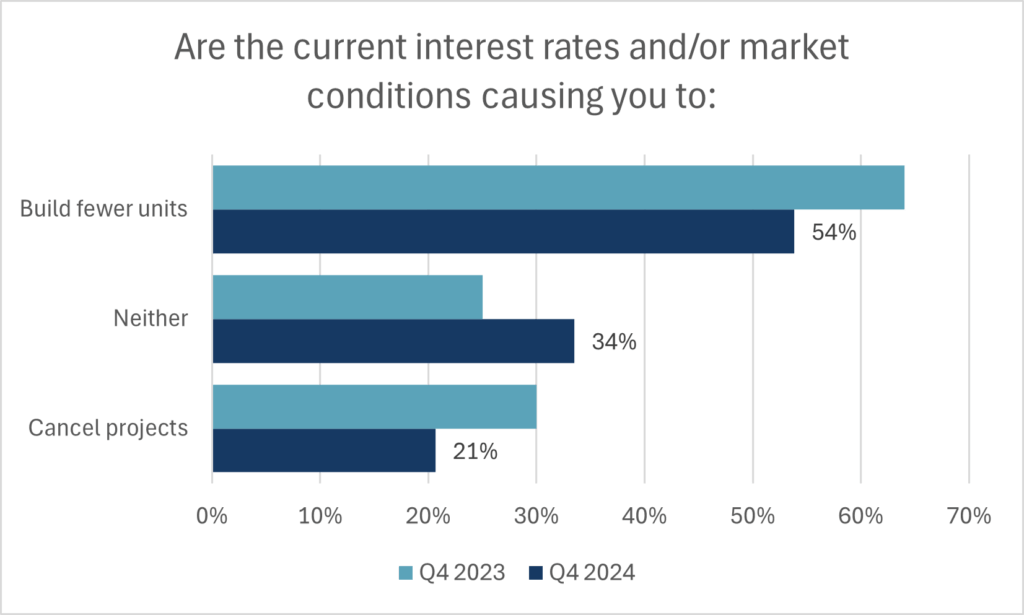

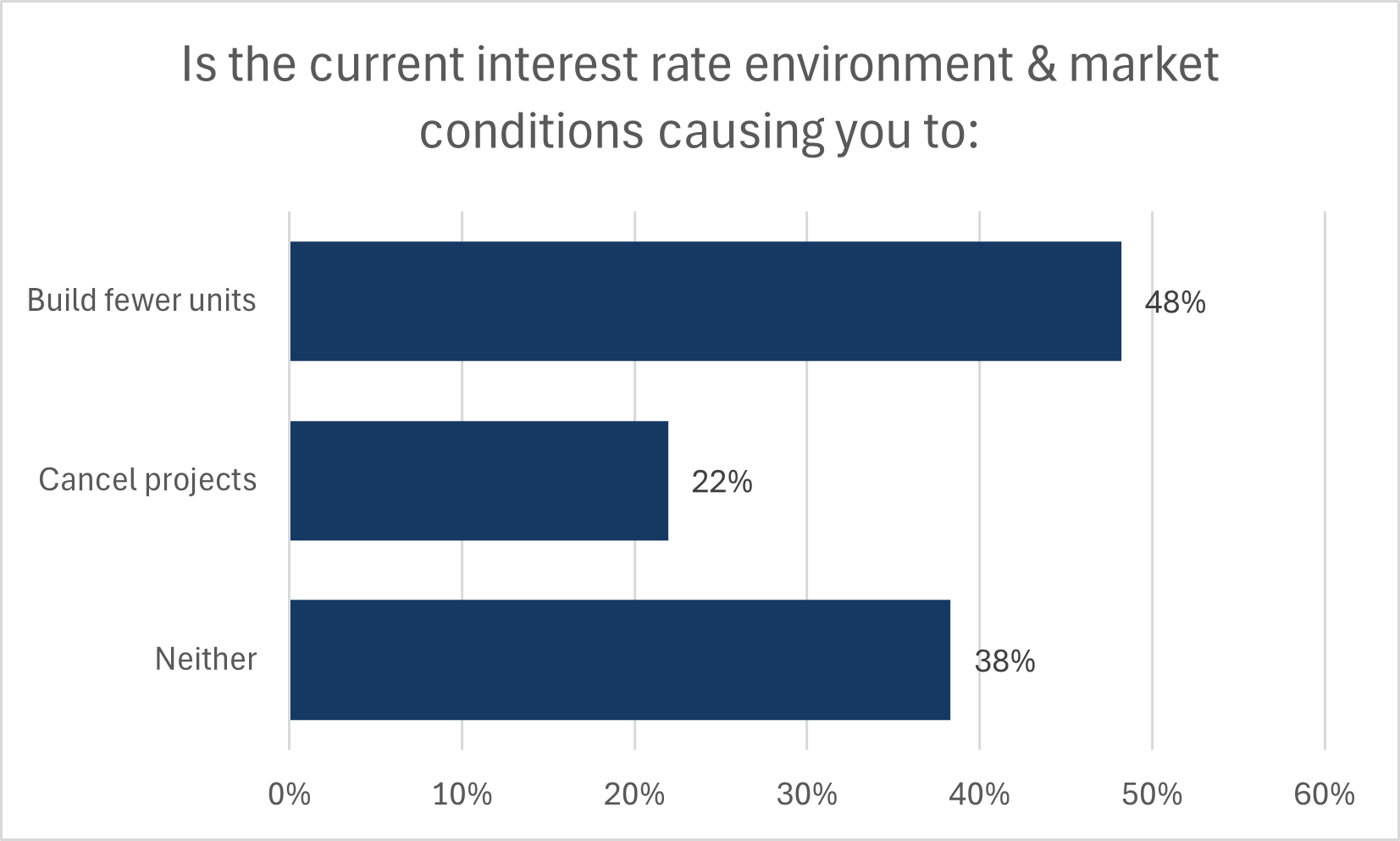

- With the majority of builders believing that further rate reductions and/or more time is needed to normalize the level of well qualified demand, builders also reported that their construction activity continues to be hampered. 48% stated that they are building fewer units than they otherwise would have as a result of demand reduction attributable to challenges with mortgage qualification. 22% have stated that the lack of sales have led to the cancellation of projects.

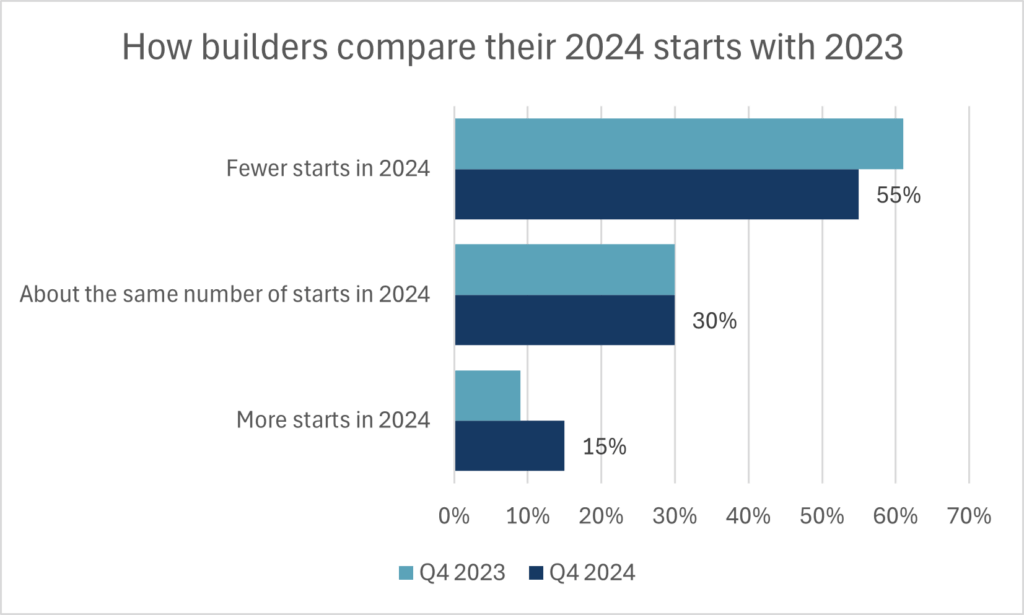

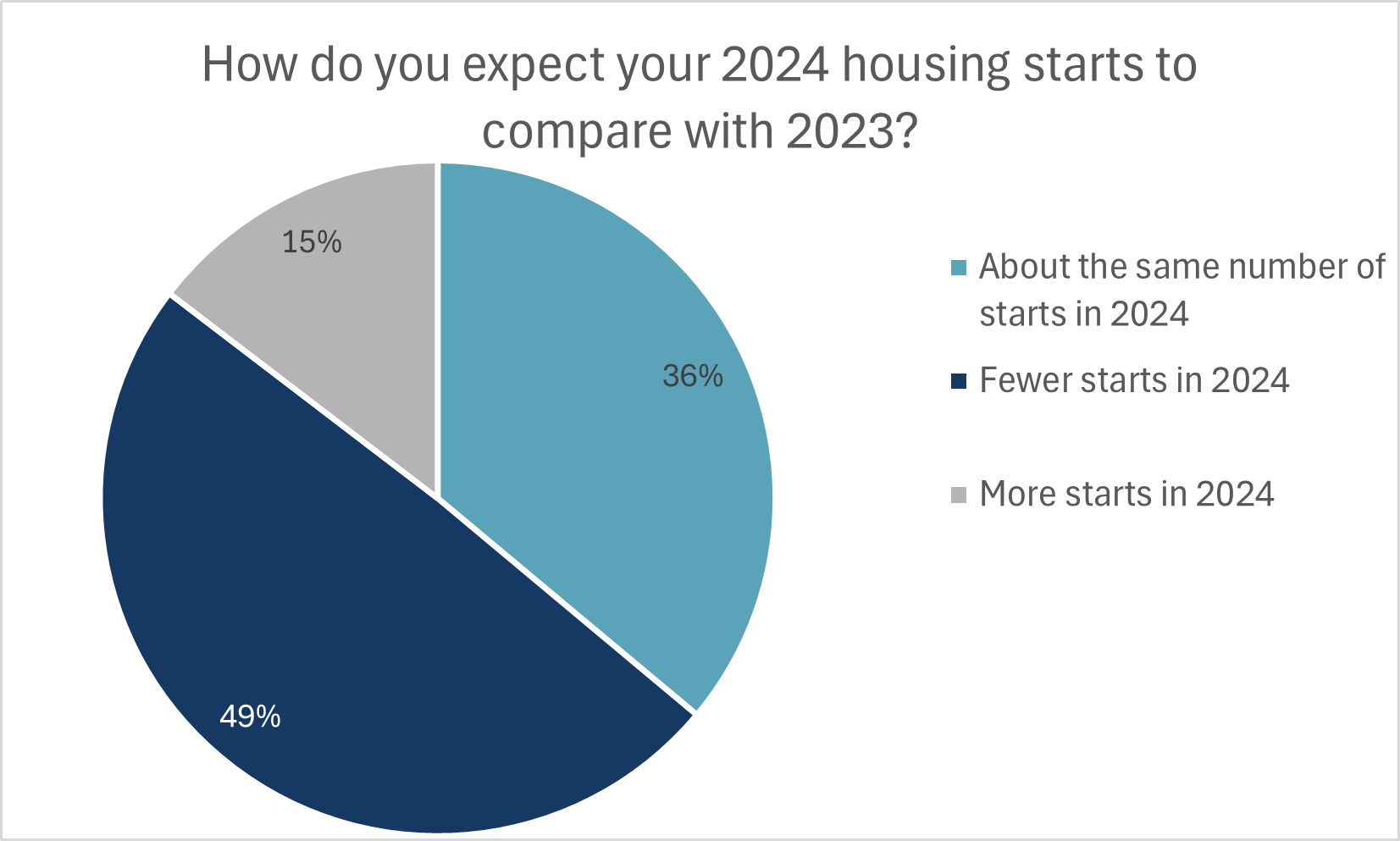

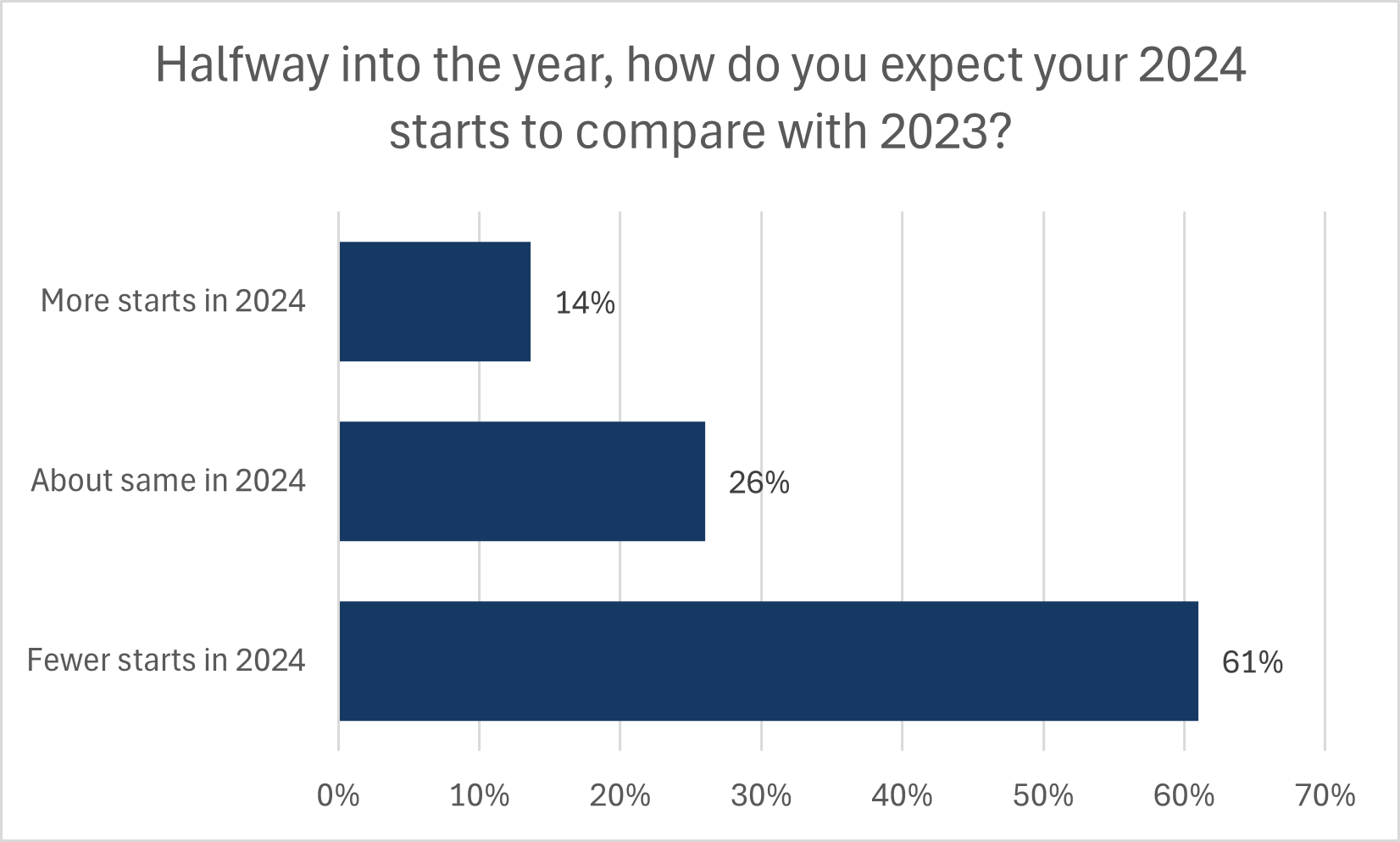

- Builders were again asked how they expect 2024 housing starts will compare against their starts in 2023. 61% of respondents expect to have fewer starts. This group of builders on average believed that their number of starts will fall 50% relative to 2023. Several small- and medium-sized builders in BC and Ontario believe that their starts will fall by 80 percent or more. Only 26% of builders felt they would maintain a similar level of starts as last year.

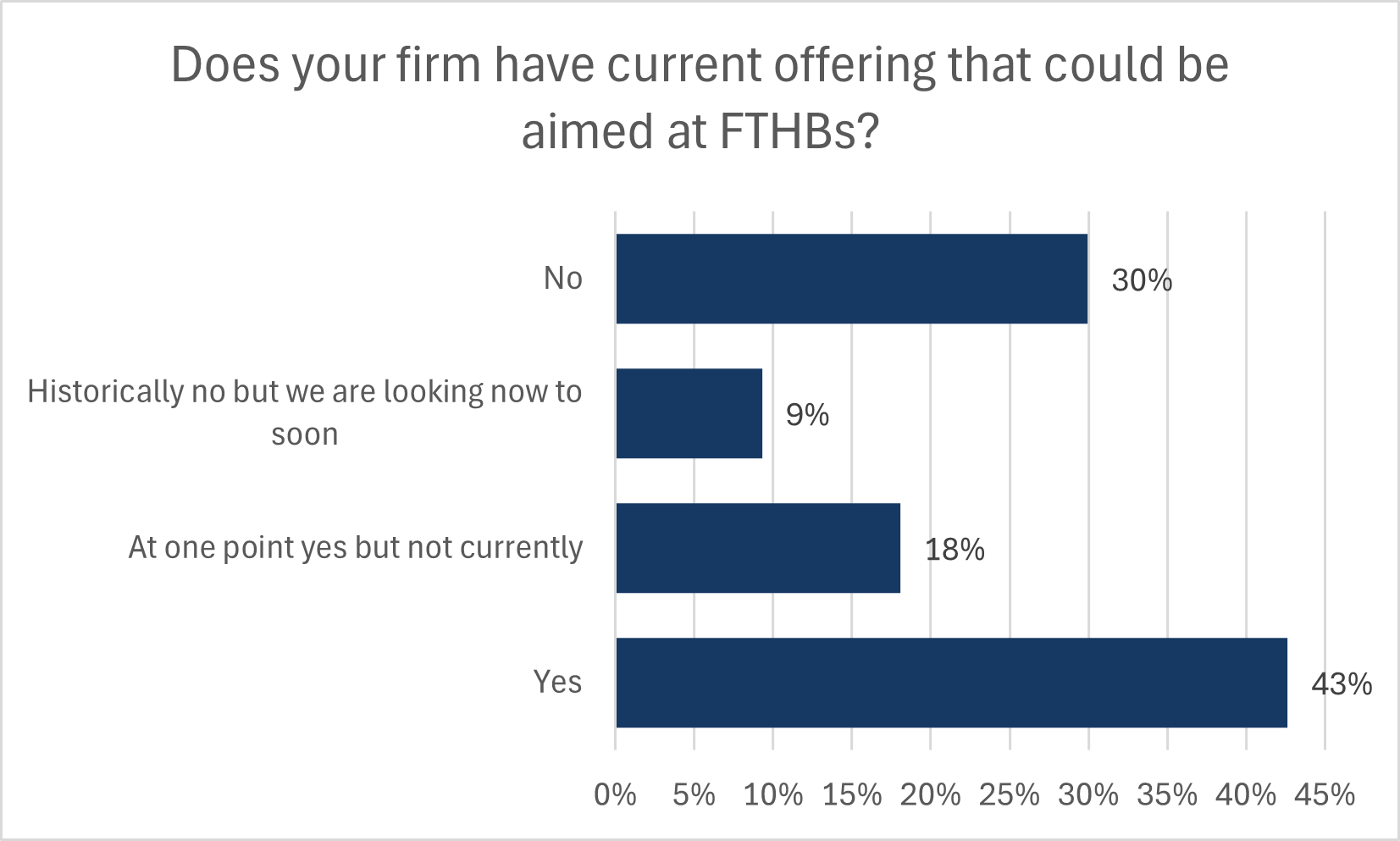

- The Canada Housing Plan, within the Federal Budget 2024, announced a lengthening of insured mortgage maximum amortizations from 25- to 30-years for new homes purchased by first-time home buyers (FTHB)—beginning August 1st. This move aims to support the creation of new supply at the entry-level segment of the market. 43% of builders state that they produce homes that could be aimed at first-time buyers. Given affordability and the cost of construction, 30% stated they do not operate in this segment and 18% stated they used to but currently do not.

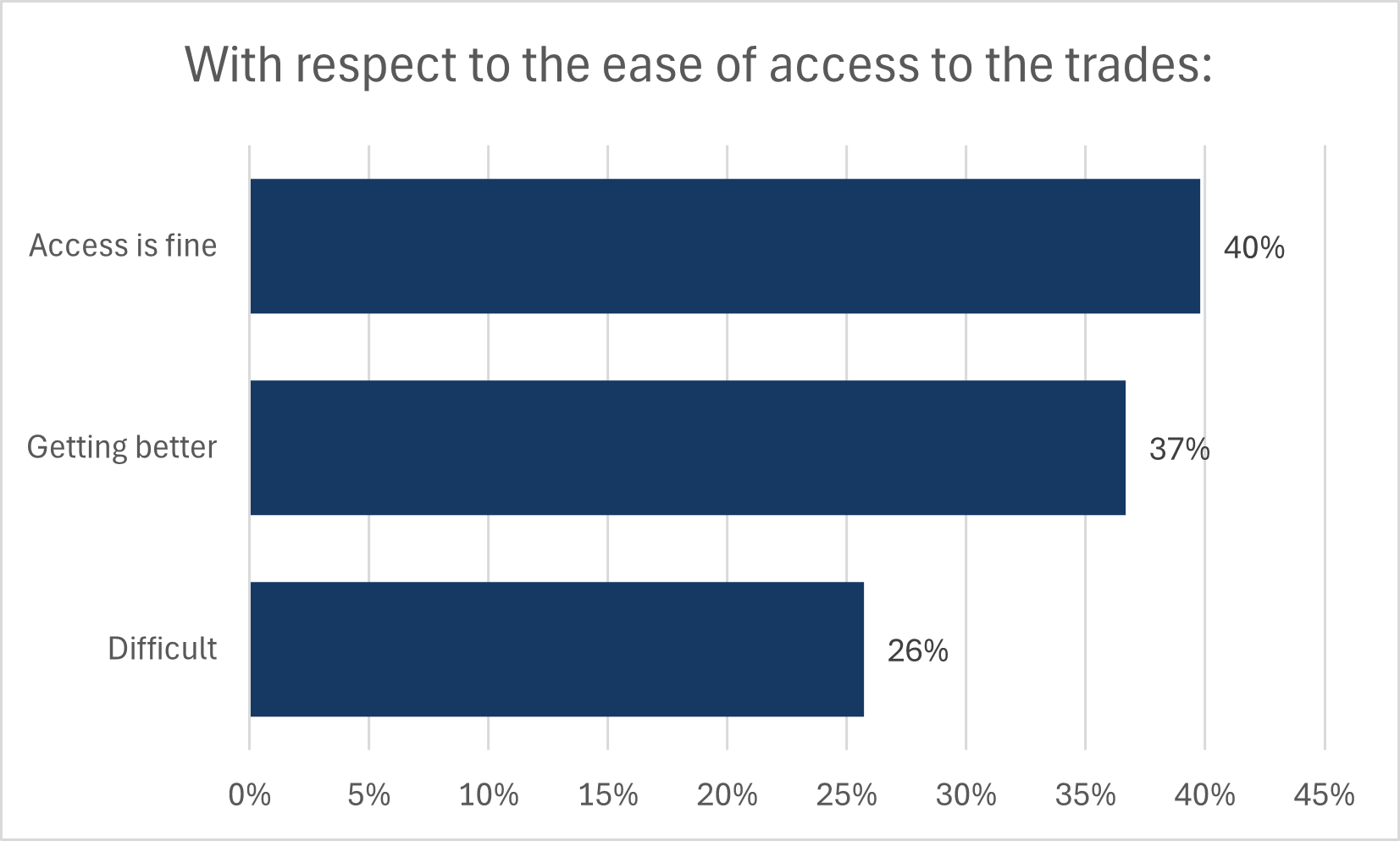

- Based on the extended period of poor sales, pressure on trades access has lowered. 40% of builders characterized trades access as Fine and a further 37% said that access was getting better. The 26% of builders that felt trades access was difficult was down from the 39% that gave this rating a year ago. It is important to note that the underlying shortage in Canada’s construction labour force has not changed and is only muted because of the slowdown in construction; this issue still requires comprehensive policy reform to increase capacity to build once the market begins to turn around.

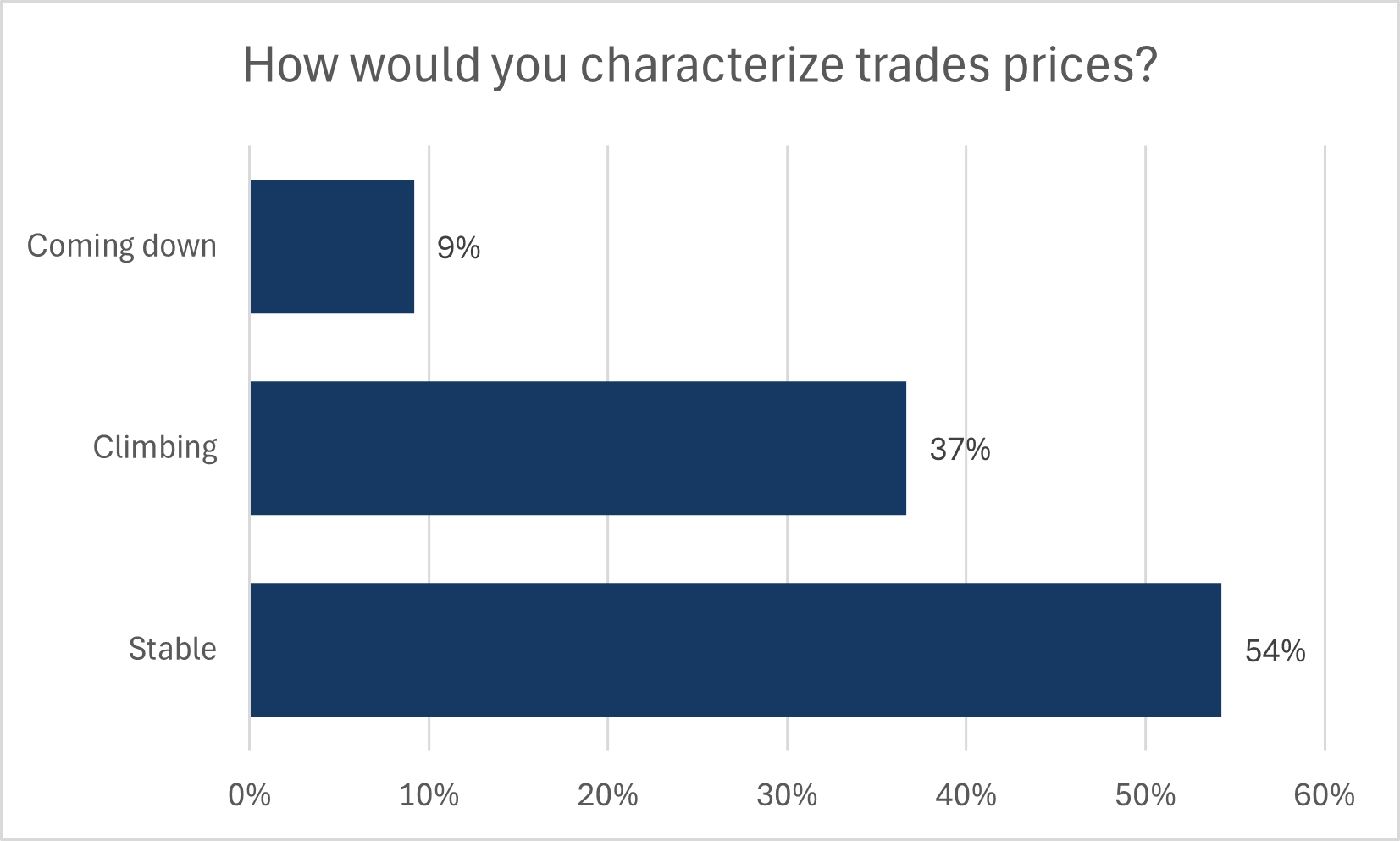

- While trades access is easing, the price of trades is continuing to rise. 37% stated that trades prices are climbing while just 9% felt they have come down. This comes after a period of rapid increase in prices, which have now settled as the new normal. While the majority believed prices are stable, these new high prices are a major source of the higher construction costs builders face.

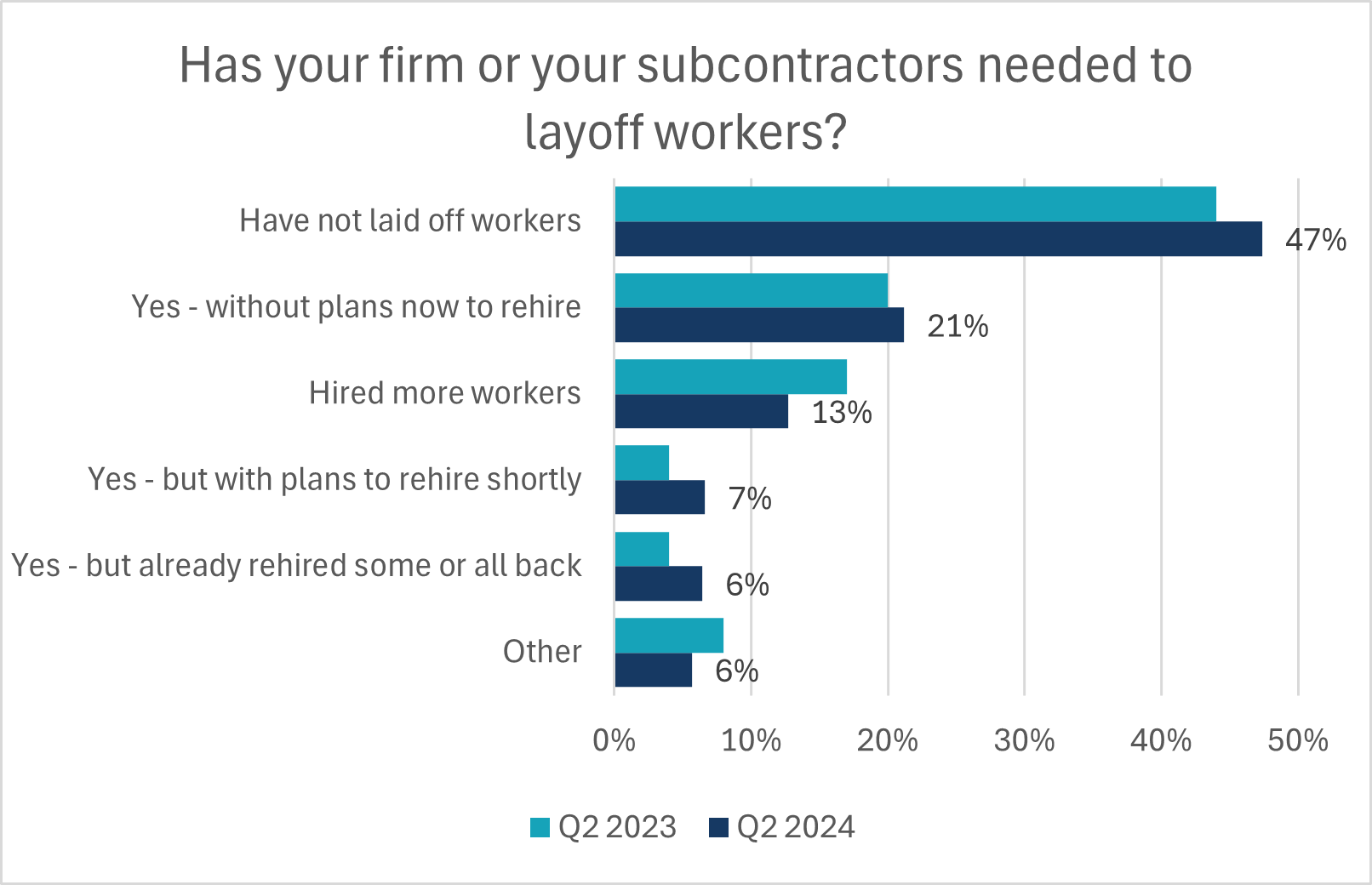

- While it may seem that trades conditions are easing under poor sales conditions, builders and the subcontractors they work with prioritize holding onto their employees. 47% reporting they have not laid off employees, reflecting the desire to retain workers even in this slow period, given the challenges of replacing them when conditions improve. The results of this question are broadly like the results of the Q2 2023 survey. In addition, average year-to-date monthly payroll employment in residential construction is largely unchanged between 2023 and 2024.

- Construction material costs also continue to mount. On average, builders estimate that their non-lumber material costs for a 2,400 square foot home have risen by just under $28,000, relative to the prices paid over the first half of 2023. Since the start of 2020, non-lumber material costs for said home will have risen by $70,000. When combined with the costs of lumber, which are also rising, inflation of material prices has added $94,000 to the cost of construction to a 2,400 square foot home compared to 4.5 years ago.

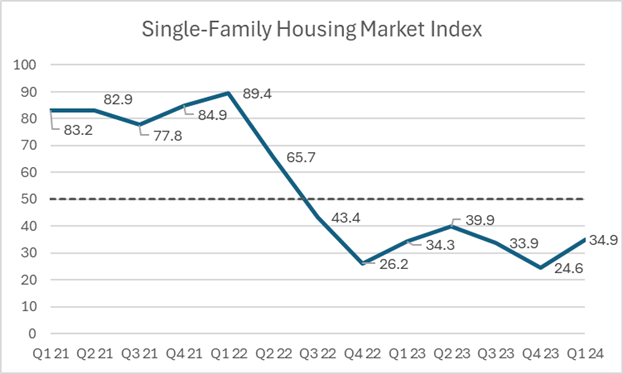

- The Q1 2024 single-family housing market index value is 34.9, 10.3 points above the record low of 24.6 in Q4 2023. This quarter’s index value is also in line with the level recorded a year ago.

- Despite the increase, it comes on the heels of a 3-year low in sentiment from the previous quarter. This means that negative sentiment, below a value of 50, has prevailed for seven consecutive quarters.

- In comparison to US single-family builders, the NAHB/Wells Fargo HMI averaged 48. This was also an improvement over sentiment in Q4 2023, and is an indication of U.S. home sales improving faster than in Canada.

- Regionally, single-family home builders in Ontario held the most downbeat views on sales once again.

- Open-ended comments from single-family builders were also in line with the responses to the HMI, with many noting extreme drops in sales.

- In a highly interest-rate-dependent market, expectations around summertime rate cut played a role in lifting sub-indices for present selling conditions, expected future selling conditions and sales office traffic levels. The rise in the current sales conditions index is likely related to well-qualified buyers forgoing some interest rate relief over the mortgage term in favour of entering the market ahead of anticipated sale price increases.

- 45% of builders rated current selling conditions as poor and contributed the most to the overall HMI remaining below 50.

- Half of builders rated their expected future selling conditions over the next six months as Fair. Again, this improvement is related to builder expectations that some additional well-qualified buyers will come off the sidelines.

- The sales office traffic subindex was the weakest of the three HMI subindices, as 55% of builders still rated their sales office traffic as Low/Very Low and a further 38% rated traffic volumes as Average.

-

-

- The multi-family housing market index recorded a value of 37.9 in Q1 2024, up 8.8 points from a value of 29.1 in the previous quarter. This is modestly above the value of 33.5 recorded in Q1 2023.

- The multi-family HMI has also remained deep in pessimistic territory for seven consecutive quarters.

- Regionally, the most downbeat views continued to stem from multi-family builders in Ontario.

- 47% of multi-family builders rated current selling conditions as Fair, a material increase from the previous quarter. Yet, just 15% of respondents characterized selling conditions as good. This led to the sub-index of present selling conditions remaining well below a score of 50.

- 62% of respondents believed future selling conditions will be average. The lower cost and larger existing inventory of multi-family units relative to ground-oriented builds could help them improve sales if and when conditions improve.

- The assessment of sales office traffic was split, at roughly 45%, between rating conditions as Average volume and Low/Very Low volume.

- Despite the intense rotation towards multi-family housing starts through 2023, the survey shows that sales office traffic is still historically weak.

- Unlike the single-family builders, open-ended comments from multi-family builders were unanimously negative, largely attributed weak sales and traffic flows to buyers remaining in a wait and see mode.

-

- These questions allow CHBA to better understand what is driving change in builder sentiment and gain insights into current industry issues. The following are some of the findings from the special questions in the Q1 2024 survey:

- As the Bank of Canada’s 5.0% policy rate continues to progressively weigh on home construction activity and the broader economy, 65% of builders said that the level of interest rates have directly caused them to build fewer units than they would have otherwise, and 31% stated they have cancelled projects. These proportions are up 6 and 8 percentage points respectively from the first quarter of 2023, when the Bank’s policy rate was lifted to 4.5%.

- With the weakness in sales conditions, particularly over the second half of 2023, 54% stated that they expect their housing starts in 2024 to be below their level of starts in 2023. On average, these builders expect a decline in their starts of 41%. Just 15% of all respondents expect to have more starts in 2024.

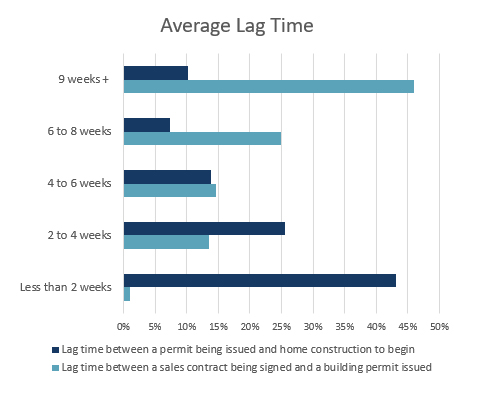

- Builders were asked to estimate the average time between the application for a building permit and its issuance. The most common average range was 2 to 4 weeks—31% of builders. However, the second most common answer was over 10 weeks, at 22%. Out of this subset of builders, half said their average wait time can extend to six months and beyond.

- The distribution of average wait times was similar to responses in the Q2 2022 survey, with a modest reduction in the proportion of builders that are waiting more than 10 weeks. The forthcoming update to CHBA’s Municipal Benchmarking Study will provide a more robust assessment of the progress made on improving municipal processes since 2022.

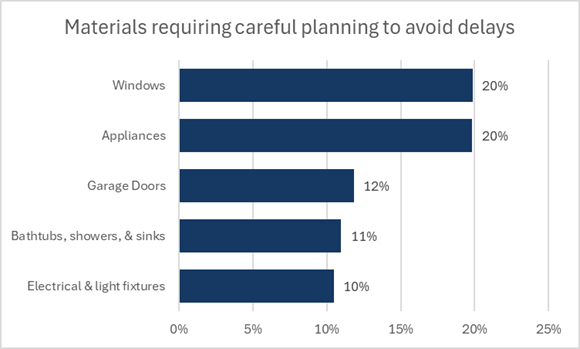

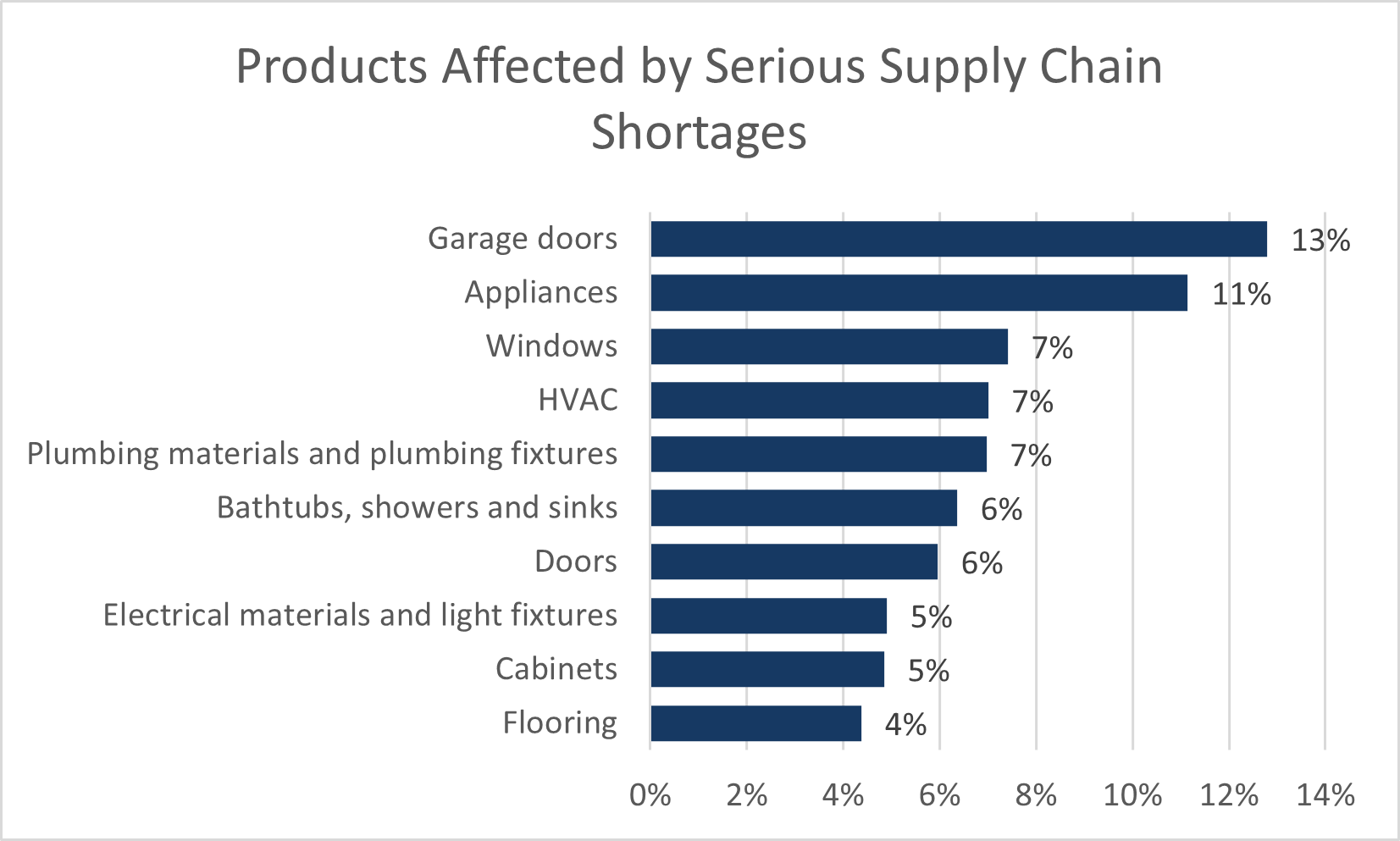

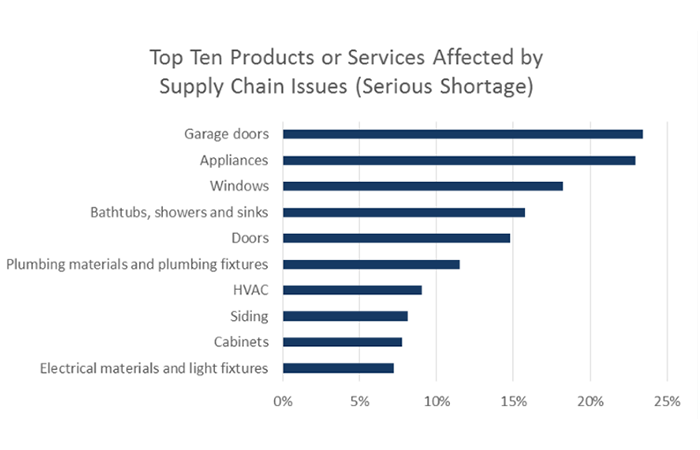

- Respondents were asked about any building materials that need more careful planning to avoid construction delays, recognizing that supply chains are back to normal. Windows and appliances were the most common answer—given by 20% of respondents each. To a lesser extent, garage doors were also an issue, dropping from the top issue as they had been for several quarters. Encouragingly, 49% stated that they are not concerned about the availability of any specific building material.

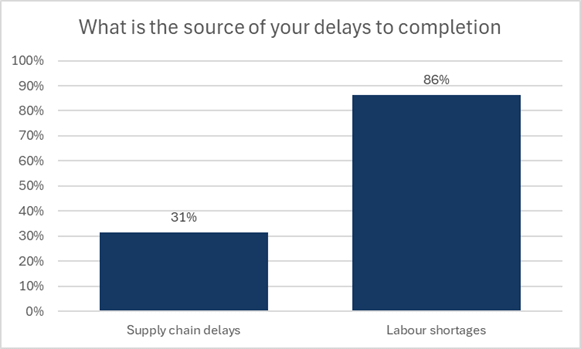

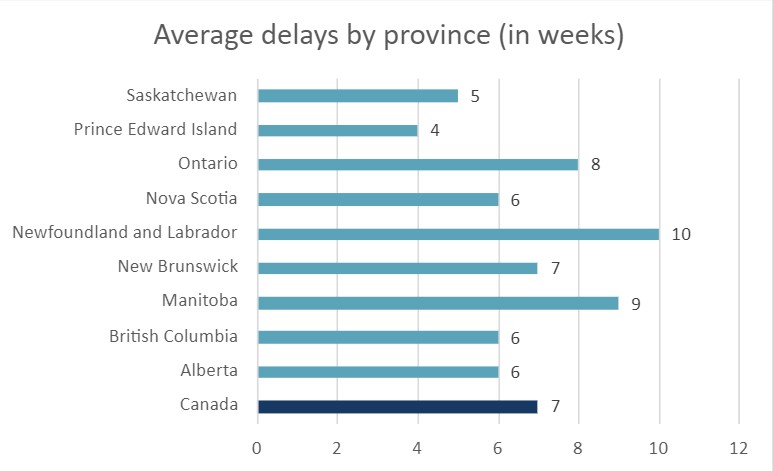

- A third of respondents said that they have difficulty meeting closing dates as a result of either building materials or labour issues. This group of builders reported a delay length of 10.6 weeks on average, a significant hinderance to rates of completion. In total, 30% of all builders are having trouble with meeting closing dates because of labour availability, and building material availability is affecting 10% of builders.

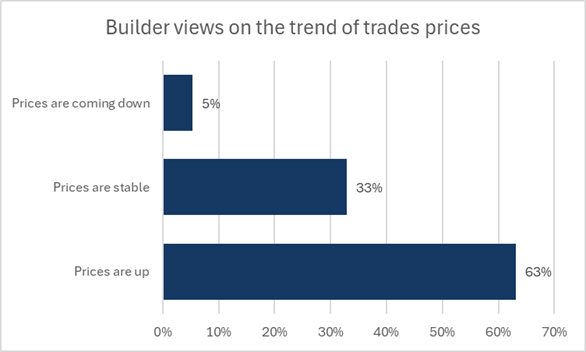

- The survey asked to characterize the labour market conditions and wage trends for trades. In terms of ease of access, the range of views were evenly represented across respondents. This suggests that acute labour challenges have been lessened by extended poor sales conditions as well as differences in access to specific types of trades. In terms of characterizing trades prices, 63% of builders stated that price of trades is up and 33% said they are stable.

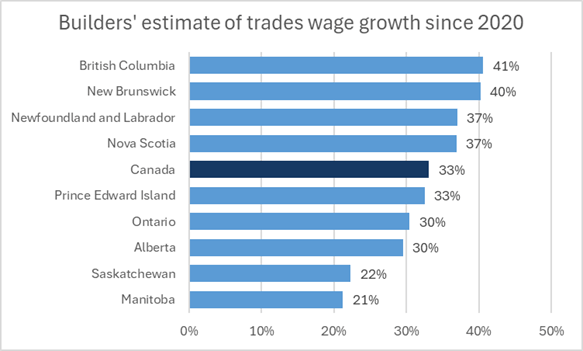

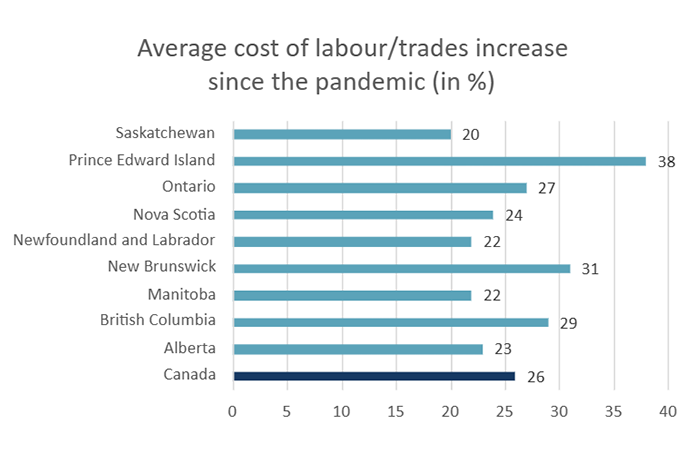

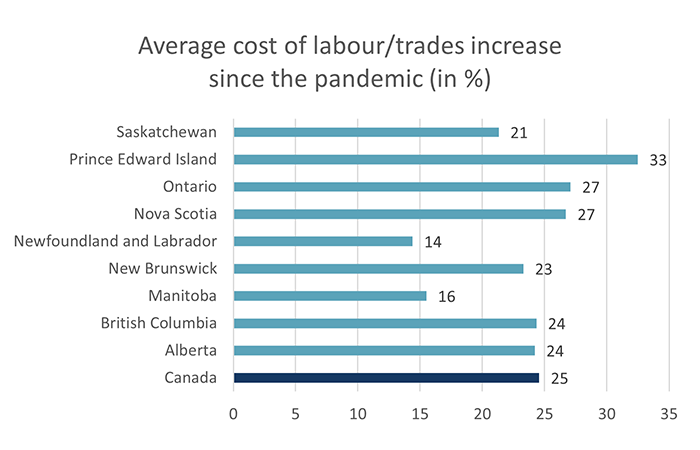

- The average of builders’ estimated trades wage growth since the onset of the pandemic in 2020 was 33%, up from a reported 26% average in Q1 2023. In combination with the results of the previous question, trades wage growth is normalizing, but this growth is occurring on top of the large increases seen in years prior.

- When asked about recent layoffs, 40% stated they have not laid off workers. This is a smaller proportion than in recent surveys. Meanwhile, the 13% that stated that there are plans to rehire those who were laid off in the very near future was slightly higher than past quarters. This could be related to some hope that interest rate changes will help bolster headcounts.

- Statistics Canada data shows that industrial prices for framing lumber rose noticeably in early 2024. Since the beginning of 2020, the estimated average cost of lumber on a 2,400 square foot home incurred by a builder stands at $24,470.

- CHBA continued to ask builders about the rise in non-lumber material prices experienced since the start of 2020. Builders estimated that these costs have risen by $43,270 on a 2,400 square foot build. 55% of builders reported their non-lumber material costs have rise above $40,000, up from 47% of builders this time last year. Similar to consumer goods, closer-to-normal material price growth is being applied to the pandemic-era run up in prices and suggests that this is the ‘new normal’ in terms of costs of construction.

- This brings the total costs of construction material increases (lumber and non-lumber) to $67,740 compared to prior to the pandemic.

Special Question Results on Factory Built Construction

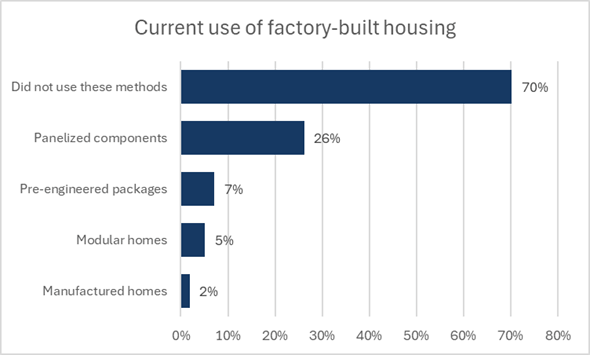

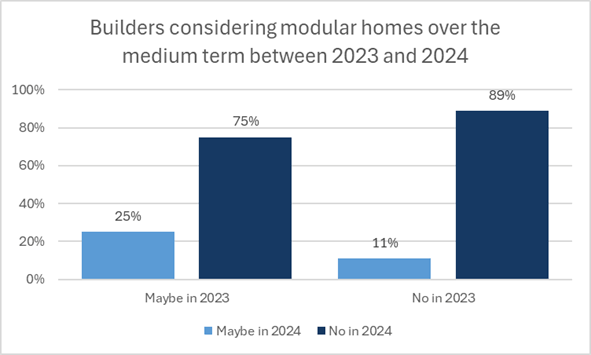

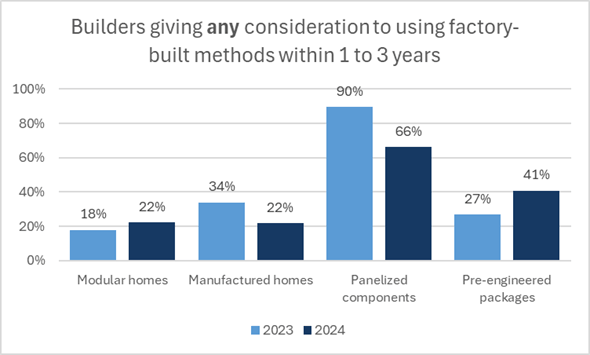

Following up from the questions surrounding factory-built construction methods first asked during 2023’s Q1 HMI survey, builders were asked if their business currently makes use of modular housing, manufactured homes, panelized components, or pre-engineered packages. Relative to 2023, panelized components remained the most prevalent factory construction method among builders at 26%. The 2% that reported using modular construction and 3% that used pre-engineered package methods in 2023 rose to 5% and 7% with the sample, respectively.

- Given the changes occurring in the industry, and in particular the labour shortage, builders were asked how seriously they are considering using various factory-built methods within their business over the next 1 to 3 years. 66% of builders said that they are considering panelized construction—which includes builders that are currently utilizing this method. Although the most prominent method, panelized construction was down from 90% in the 2023 survey. Part of this could be related to differences in survey sample or a legitimate decline in interest given market conditions. That said, using a subset of repeat respondents between 2023 and 2024, we found that 72% of those that had originally stated they were firmly interested in implementing panelized construction methods remained interested a year later, while 19% who originally said they may be considering panelized construction now are no longer considering it a year later. That said, 38% of the builders who originally said they were not considering factory-built options are now giving it some thought. Therefore, despite the total sample decline, there is evidence that panelized adoption will increase over the next few years.

- Both the use and medium-term consideration for modular housing improved relative to 2023, but total uptake remains low. 5% stated they have produced a modular home over the past year, up from 2% in 2023, and a total of 10% said they are firmly considering modular over the next 1 to 3 years—relative to 4% last year. With increased government focus on derisking this technology, adoption could accelerate over the years ahead.

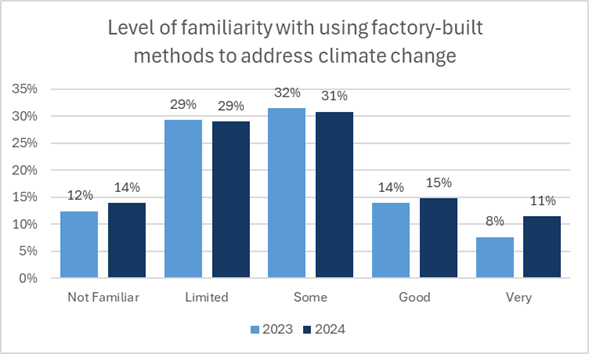

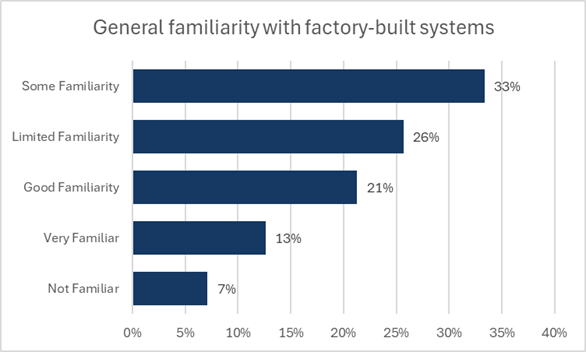

- Builders were asked to characterize their familiarity with factory-built methods in a broad sense as well as its separate benefits related to improving business productivity and addressing climate change factors (i.e. emission reductions and improved resiliencies). About two thirds have familiarity with factory-built methods and the productivity benefits, and 57% are familiar with the benefits for addressing climate change factors.

- The CHBA Single-Family Housing Market Index fell to a historical low of 24.6 in Q4 2023, the most negative quarterly sentiment reading in the three years CHBA has been conducting the survey. The index fell 9.3 points from a reading of 33.9 in Q3 2023 and is 1.6 points below the previous record low of 26.2 recorded in Q4 2022.

- The record low sentiment readings represent a continued decline in serious and qualified buyers looking to purchase a new home. In addition, builders commented that some buyers are waiting on the sidelines with the belief of lower mortgage rate offerings in 2024.

- For an approximate comparison, the US NAHB’s single-family HMI averaged 37 in the fourth quarter of 2023, down from an average reading of 45 in Q3 2023, but still better than the Canadian numbers.

- The Q4 2023 single-family sub-indices for present selling conditions, expectations for future selling conditions, and sales office traffic fell to levels that were all lower than the previous quarter and the previous record low seen in Q4 2022.

- As with previous quarters, the proportion of builders holding pessimistic views were broadest in Ontario. However, single-family sentiment deteriorated in all regions of the country over Q3 2023.

- 57% of single-family builders rated current selling conditions as Poor, worsening nearly 10 percentage points from the previous quarter. Regionally, except for the Atlantic region, most builders characterized current selling conditions as Poor.

- Influenced by several factors, views about future selling conditions were closely split between Poor (45%) and Fair (43%). However, the proportion of builders that were optimistic about conditions in the next six months fell six percentage points from Q3 2023 to 12%. Rating future conditions as Fair was most common in all regions outside of Ontario, where the most common rating was poor.

- The collective view on sales office traffic was the most pessimistic of the sub-indices, with 73% giving a Low or Very Low rating. Several builders commented that traffic was especially slow even when considering that it is a seasonally slow time of the year for inquiries from prospective buyers. Just 2% of builders surveyed rated sales traffic conditions as High or Very High.

- The CHBA HMI for multi-family builders was down to 29.1 in Q4 2023. The index fell 4.5 points from a value of 33.6 in Q3 2023. The declines seen in the second half of 2023 leaves sentiment marginally above its 3-year low of 26.0 recorded in Q4 2022.

- Regionally, downbeat views from multi-family builders were most broadly held in Ontario as well as British Columbia. This is despite strong annual growth in multi-unit starts in both Toronto and Vancouver in 2023, reflecting projects that were approved before the climb in interest rates. Meanwhile, the balance of sentiment was neutral among builders responding from Prairie provinces.

- The majority of multi-family respondents, at 53%, rated current selling conditions as Poor. The increase in the proportion of those giving a Poor rating over last quarter came from a decline in the proportion of respondents that gave a Fair rating. Builders that gave current selling conditions a Good rating held steady from Q3 2023 at only 13%.

- Expectations about future selling conditions were balanced, with 47% of builders giving a Fair rating. This was higher than the 32% of multi-family builders that gave a Poor rating. Only 21% expect future conditions to be good.

- 63% of multi-family builders rated traffic of prospective homebuyers to be Low or Very Low, up a substantial 22 percentage points from the previous quarter. This came from a large drop in the proportion of builders that said sales traffic was average, which now stands at 31%.

- Relative to Q4 2022, multi-family builder views on current selling conditions and sales traffic levels were quite similar in Q4 2023 survey.

These questions allow CHBA to better understand what is driving change in builder sentiment and gain insights into current industry issues. The following are some of the findings from the special questions in the Q4 2023 survey:

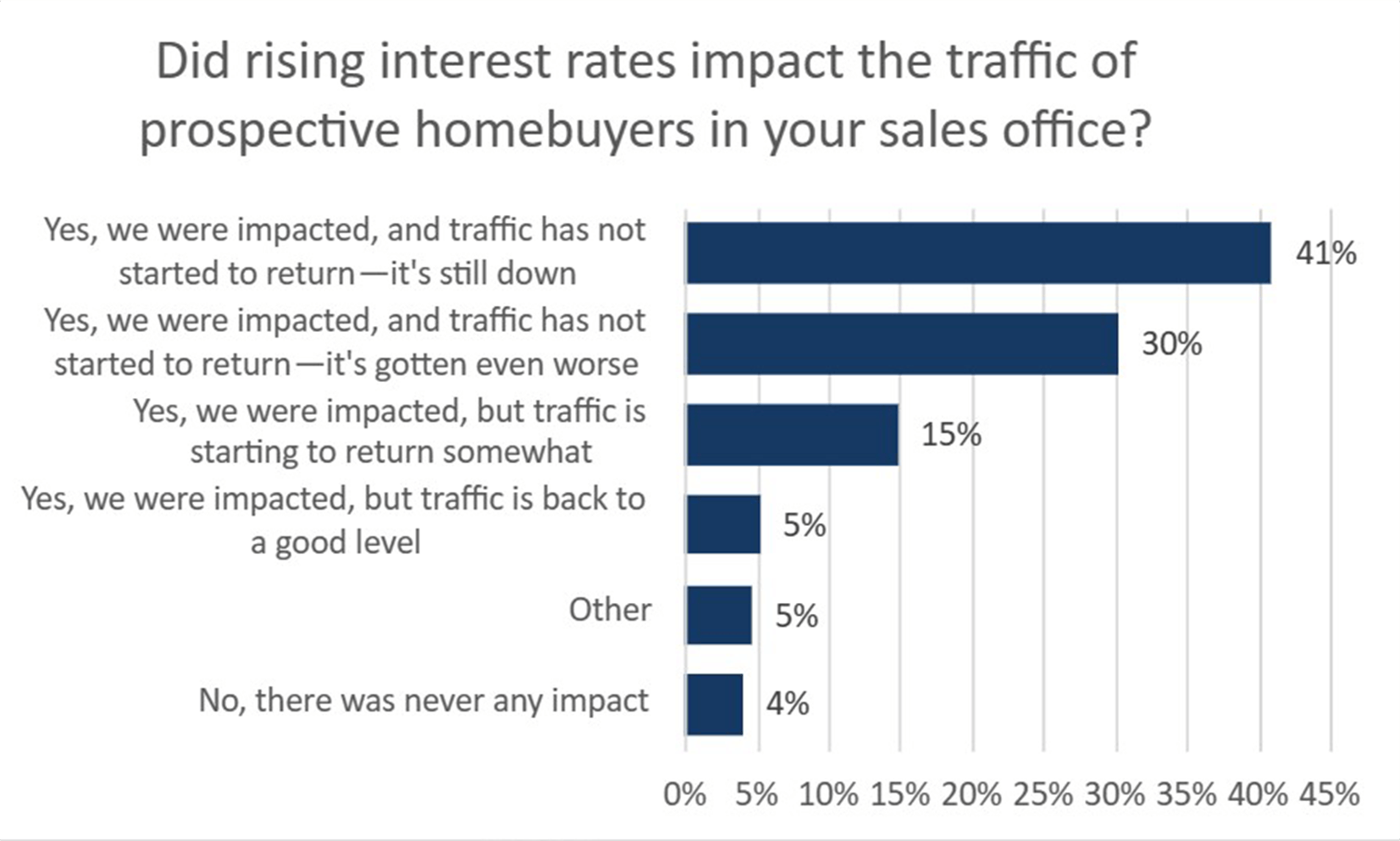

- Assessing the cumulative impact of interest rate hikes on their sales office traffic, 41% of builders stated that their sales traffic is down and they have not yet seen a recovery in traffic flow. A further 30% of builders noted that not only has prospective buyer traffic not seen a recovery, but it has also worsened as of late.

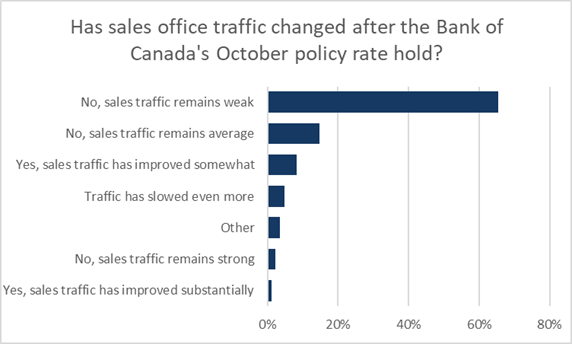

- Builders were asked a follow up question about prospective buyer traffic after the Bank’s rate hold announced in late October. In the first half of 2023, a four-month pause in interest rate hikes corresponded to a modest improvement in both HMI readings. However, this was the case in Q4. 65% of builders reported that sales traffic remains weak, and another 5% reported that traffic has slowed even more.

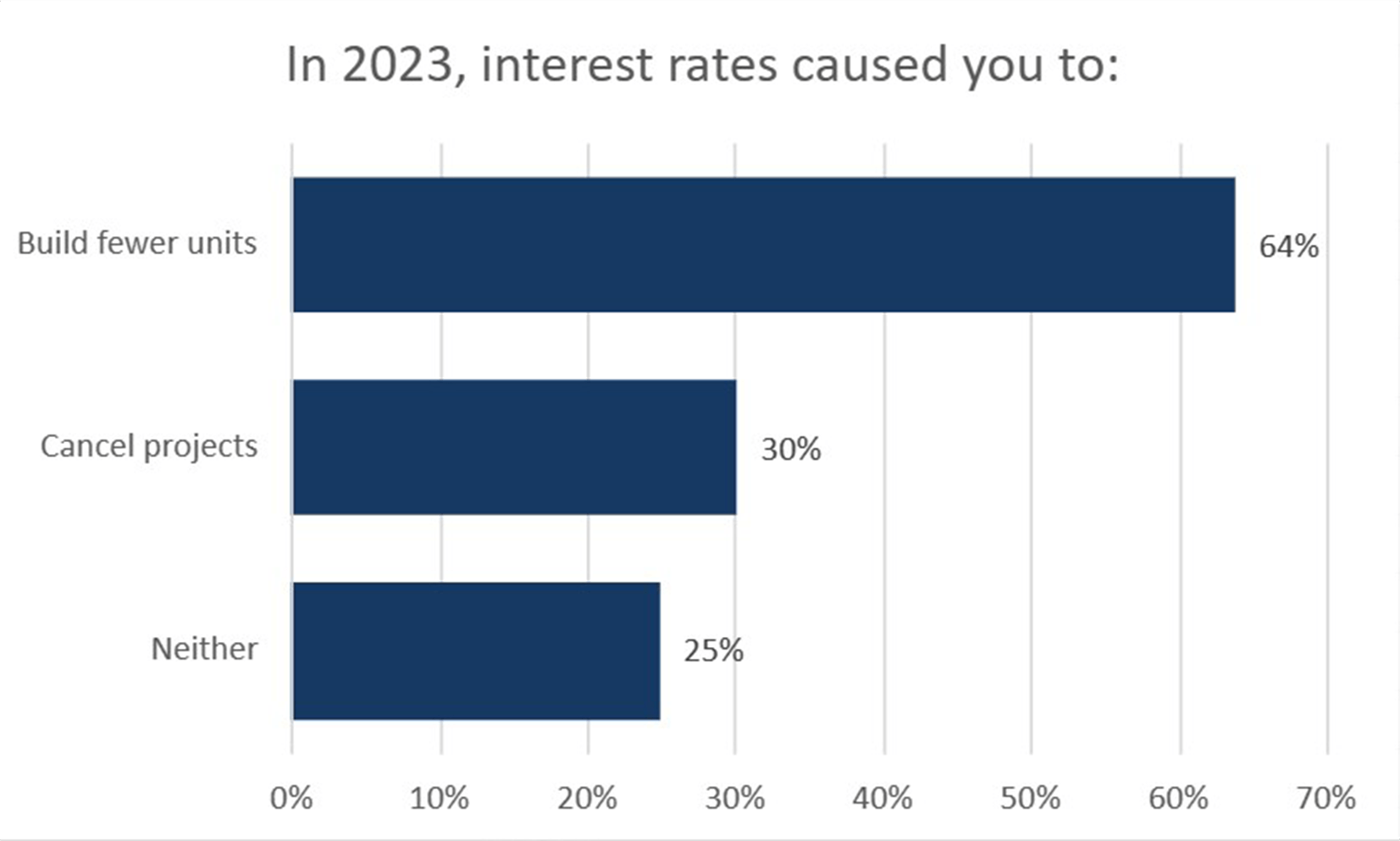

- Builders were asked if they have had to scale back their operations as a result of the interest rate environment in 2023 and the results were somewhat consistent with the prior quarter. 64% stated that it has caused them to build fewer units and 30% of builders stated that they canceled projects as a result.

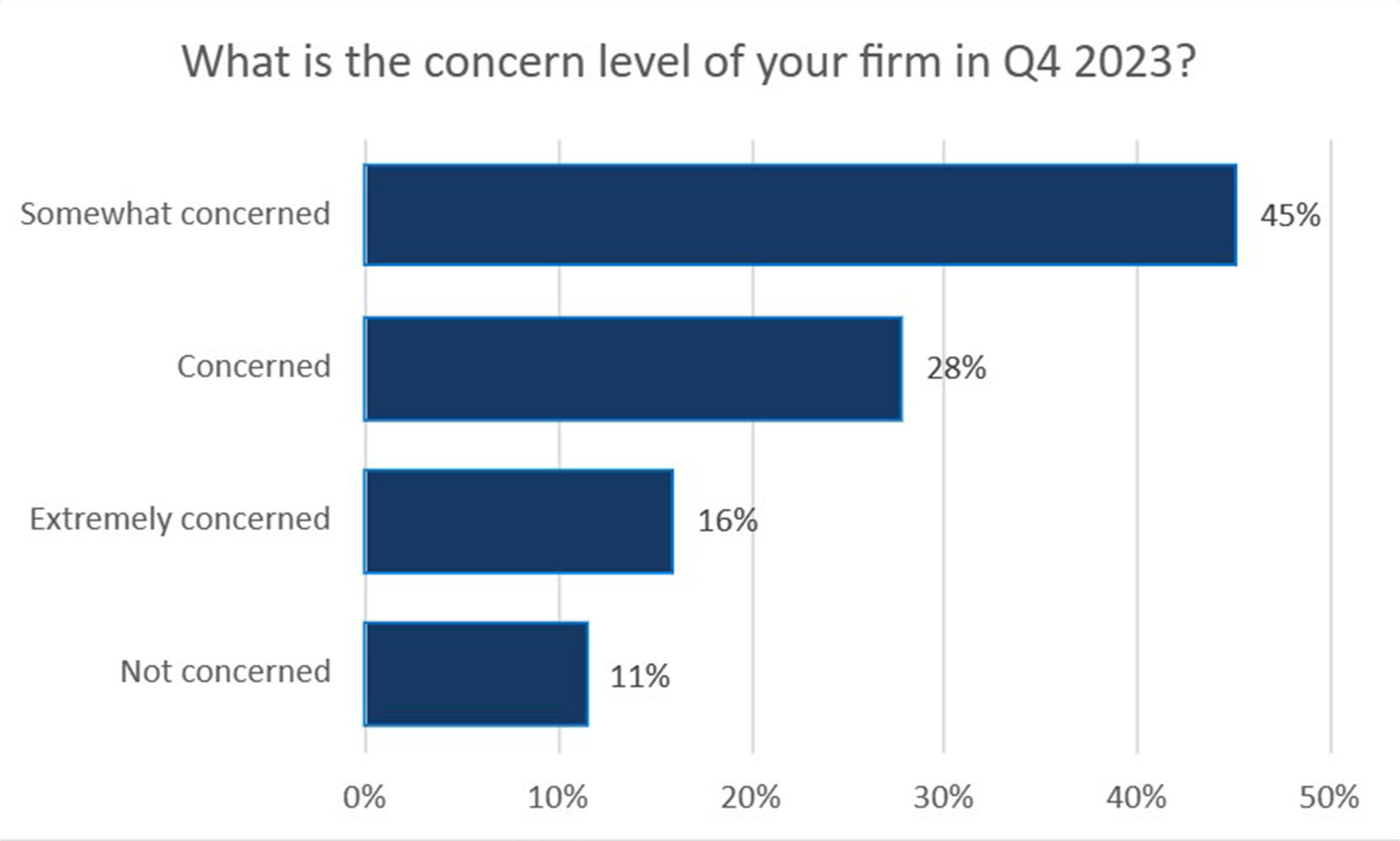

- With respect to the concern they currently have about the future of their business, 45% of builders stated that they are somewhat concerned and 28% said they are concerned. 11% stated they did not have any concern.

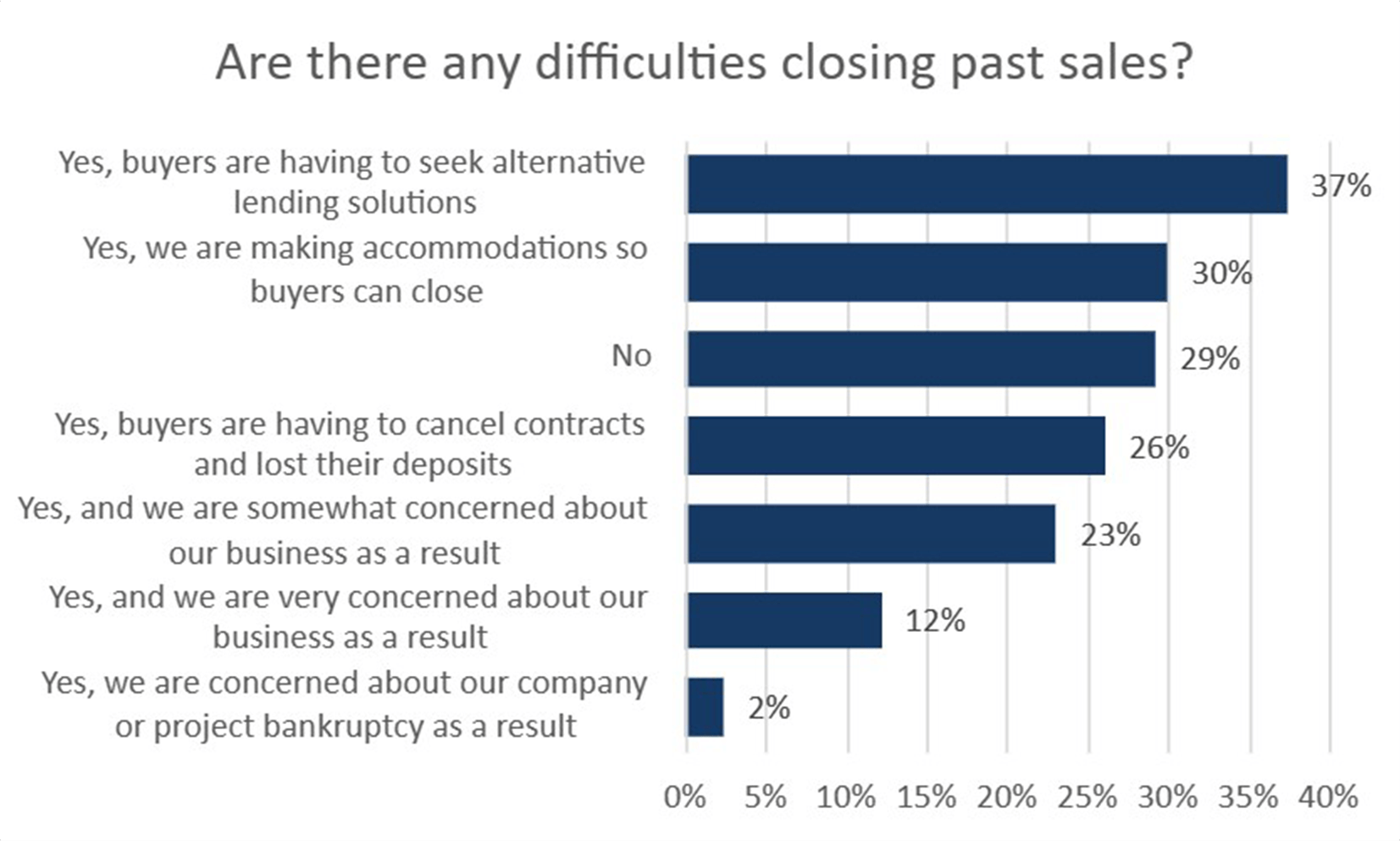

- Builders continue to face difficulties with closing past sales. 37% of respondents stated that buyers have sought alternative lending solutions and 30% said that they’ve made accommodations so that buyers can close.

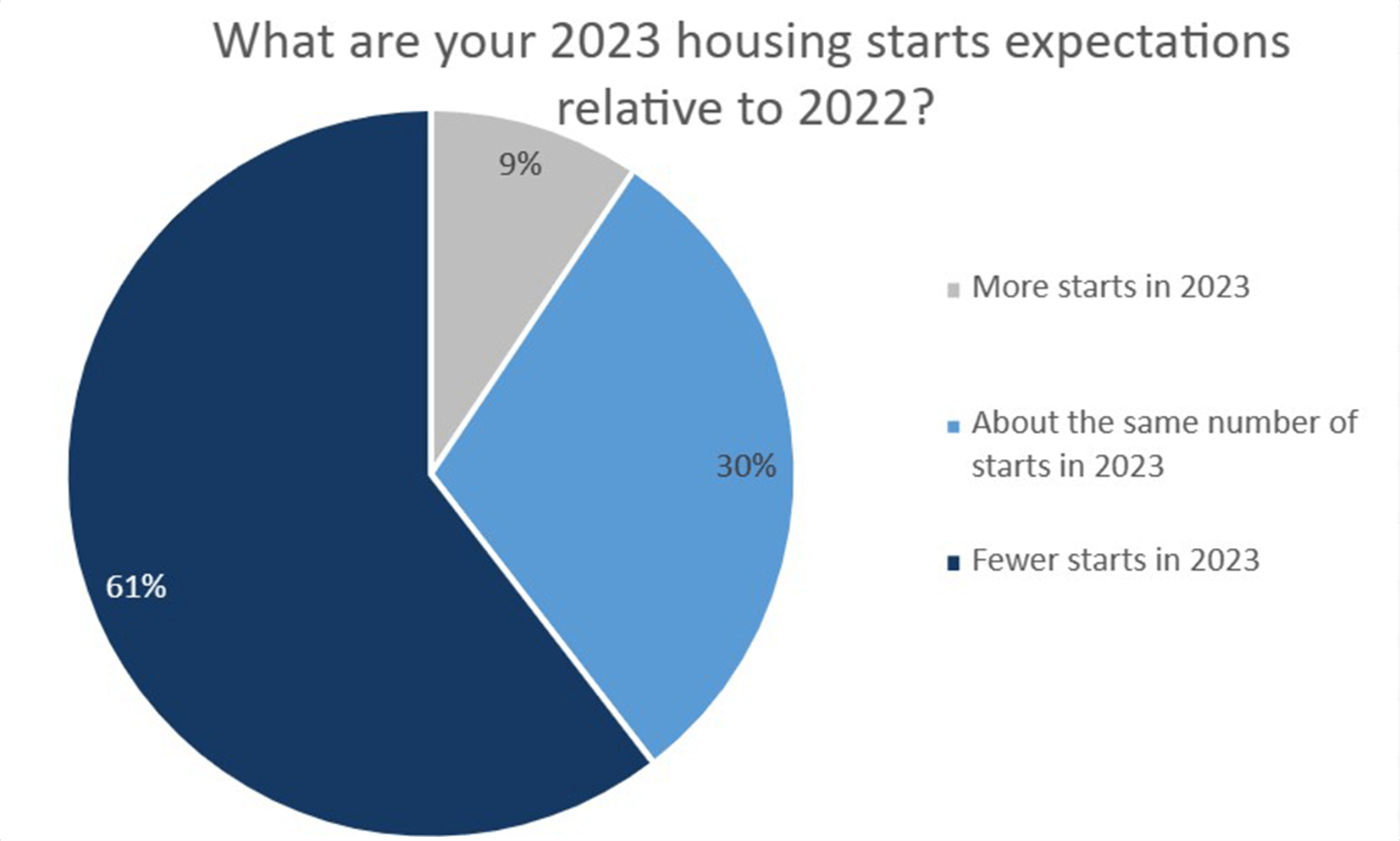

- With the majority of the year complete, builders were asked to report how their annual housing starts compare to the number of starts in 2022. 61% of builders surveyed stated that they expect to have started fewer builds in 2023 relative to 2022, while just 9% said they expect their starts to have increased.

- Out of the builders that said they expect to build fewer units in 2023, they expect to have reduced their starts on average by 47%. The average expected percentage decrease in 2023 starts was higher among small and medium builders.

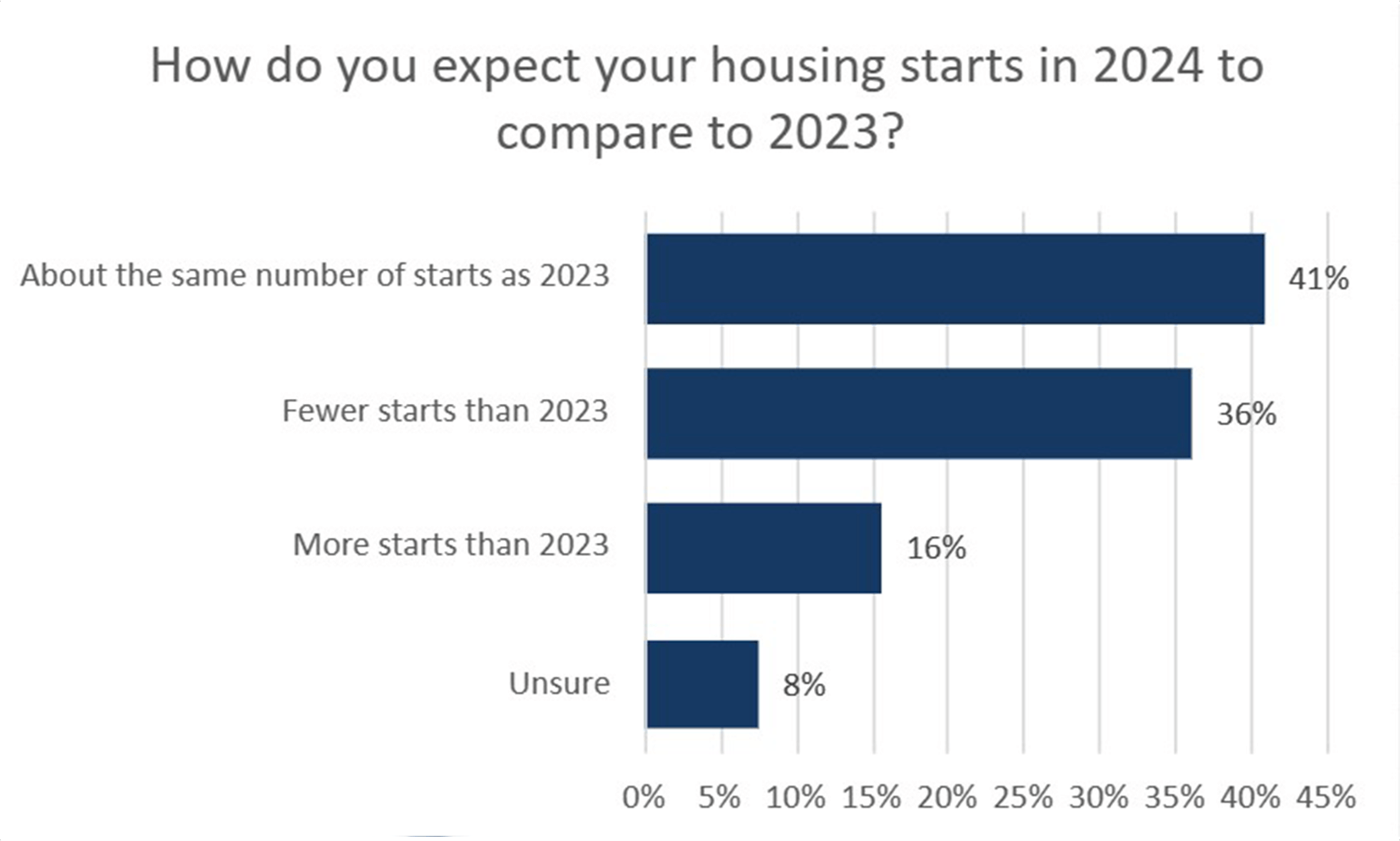

- We asked about builder expectations for their number of starts in 2024, based on demand conditions over the previous 12 months. 41% of builders stated they expect to build about the same number as they will in 2023. Closely behind, 36% reported that they expect to start fewer homes next year.

- Builders were also asked to provide any other comment about their starts expectations for 2024 and while focused on interest rates, builder rationale varied. Several builders stated their belief around maintaining their number of starts as 2023 was due to the expectation of rate cuts. Other comments stated that 2024 will certainly be lower, as 2023 was used to catch up on delayed projects from 2022.

- Beyond interest rates, builders were asked to identify other pertinent factors that are also constraining their housing starts. As with Q3, municipal processes was the most widely reported pain point lowering a builder’s number of starts—at 47% of builders. 30% of builders noted a lack of adequate labour remains an issue, while 28% stated that access to land is difficult.

- When asked the same question but under a hypothetical situation where market conditions were better, the proportion of builders stating that a lack of labour would hold them back increased to 39%. The proportions of other stated factors were similar to the answers from the original question.

- With the lowering of sentiment and weak sales conditions, 33% of builders reported laying off workers - 9% expect to rehire but 24% do not.

- Builders were asked about the cost and the availability of trades. 51% of builders stated that the cost of trades is up. Some builders commented that access has improved because of the weak local market conditions and that delays due to trades access will return when those conditions improve.

- On average builders estimate that their trades costs have increased 33% since the onset of the pandemic. So as more normal wage growth resumes, this is on top of large increases in the recent past, which is also the case for many other costs incurred by builders.

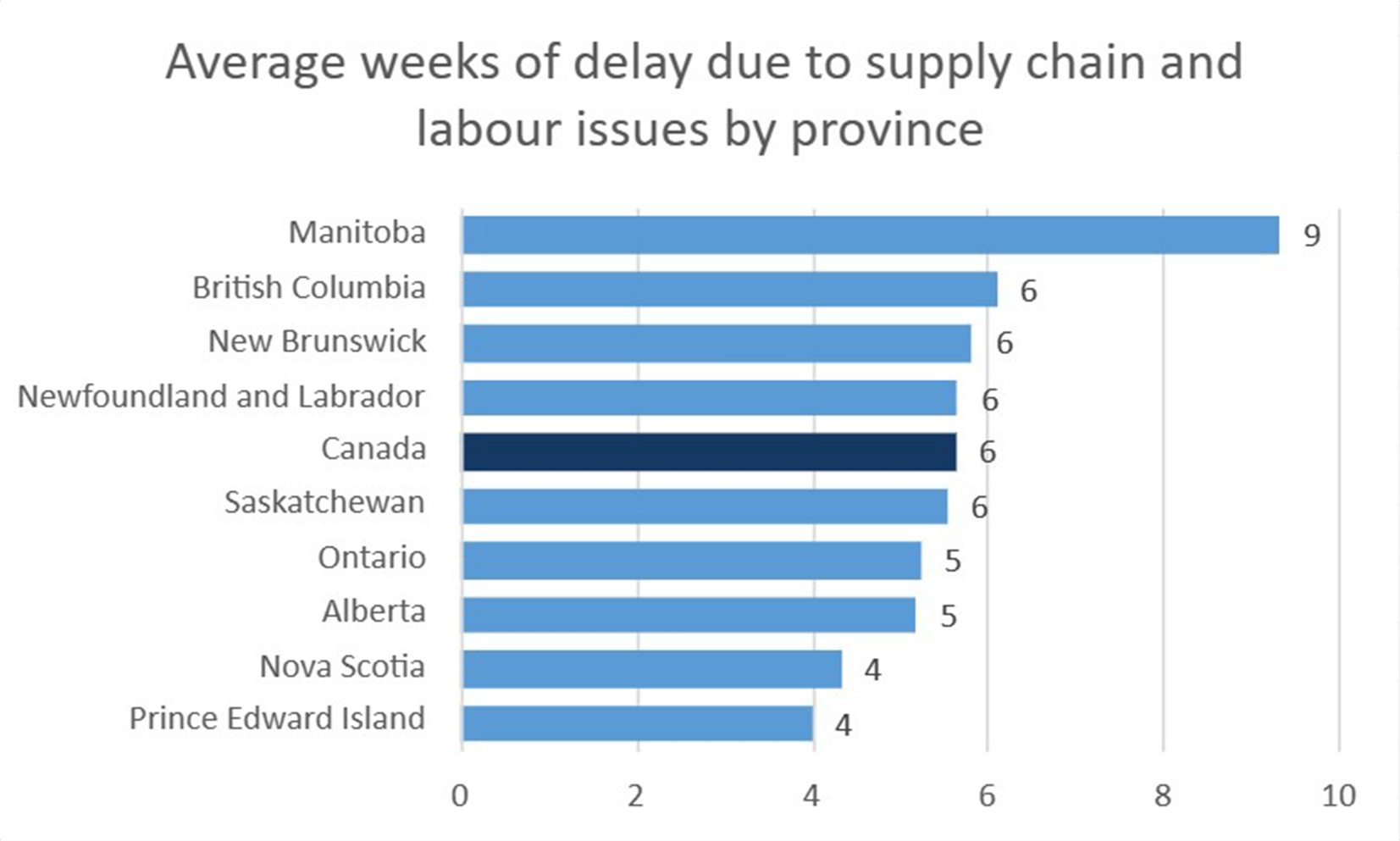

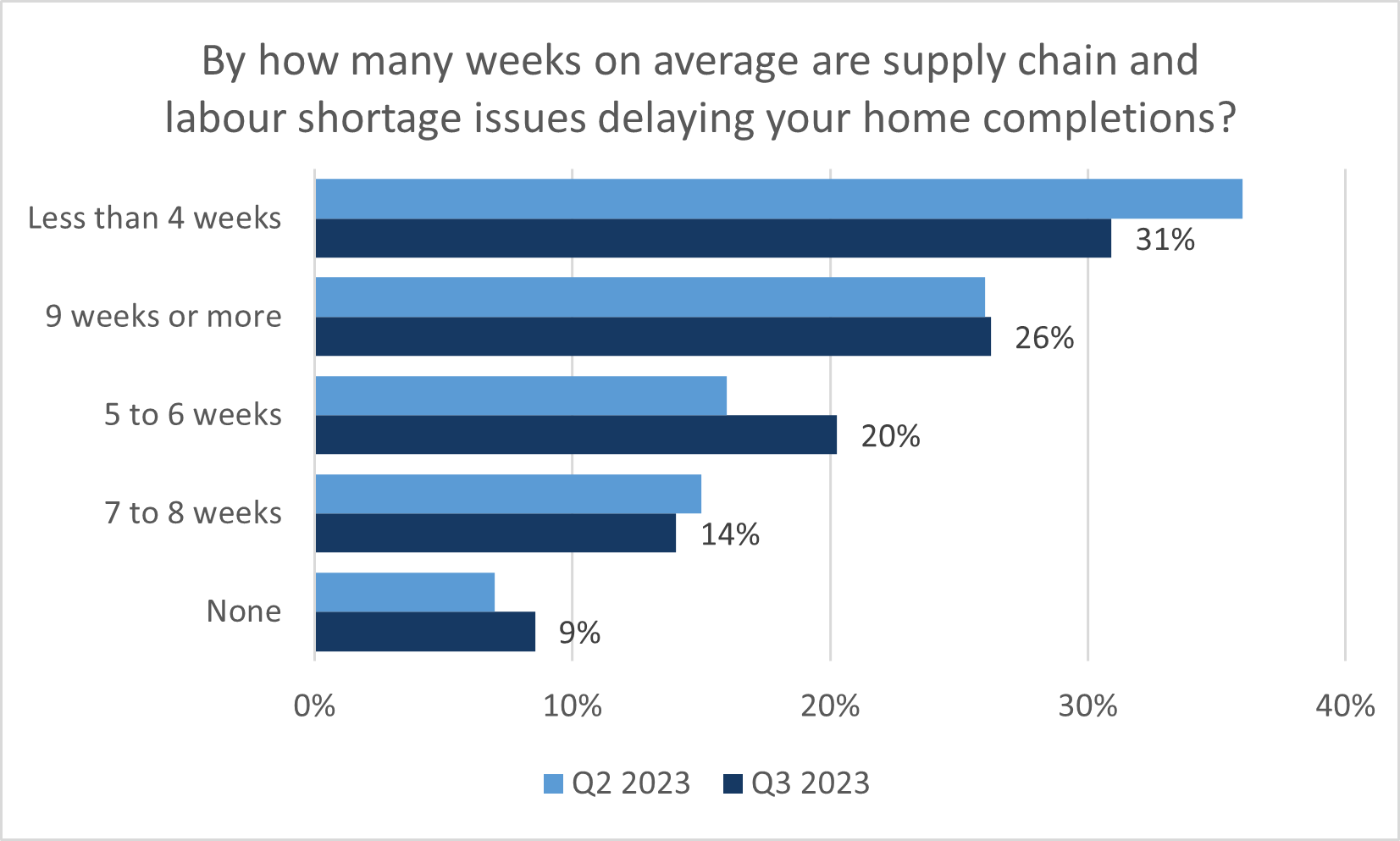

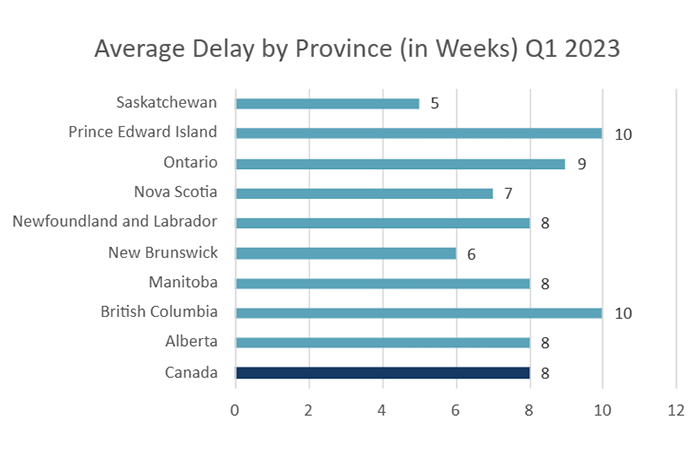

- Supply of inputs, especially building materials, have improved over the course of 2023 as demand for new homes weakened and supply chains normalized. The nationwide average construction delay as a result of a lack of materials or labour trend downwards towards normal, but is still at 6 weeks delay compared to normal. This is down from an average of 7 weeks over the previous two quarters and down from 10 weeks in Q4 2022.

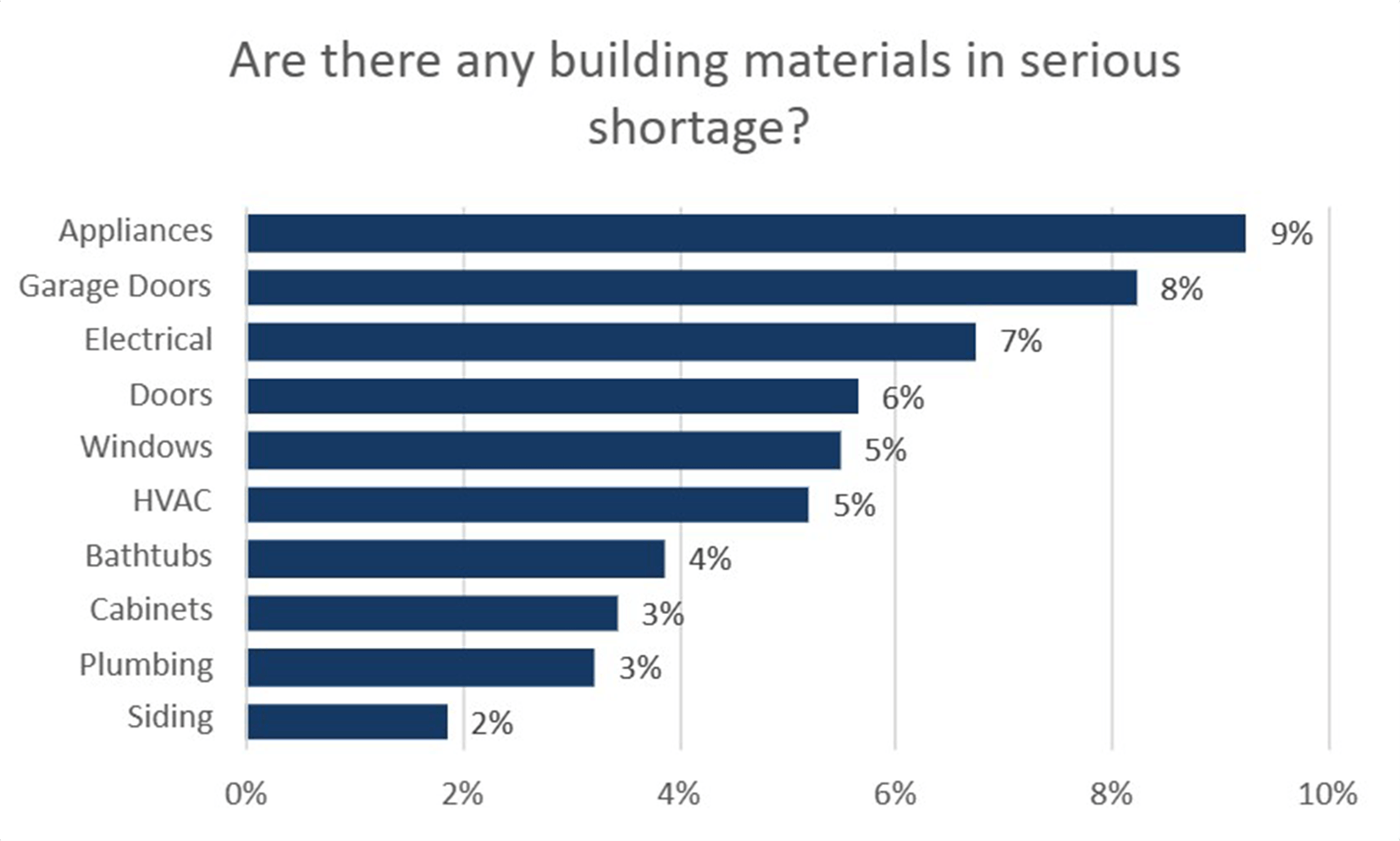

- As with previous quarters, appliances and garage doors were the two building material categories with the highest incidence of being in serious shortage at 9% and 8%, respectively. 21% of builders stated they did not experience noteworthy material shortages this quarter, which would be good if it weren’t coupled with the slowdown in construction activity overall.

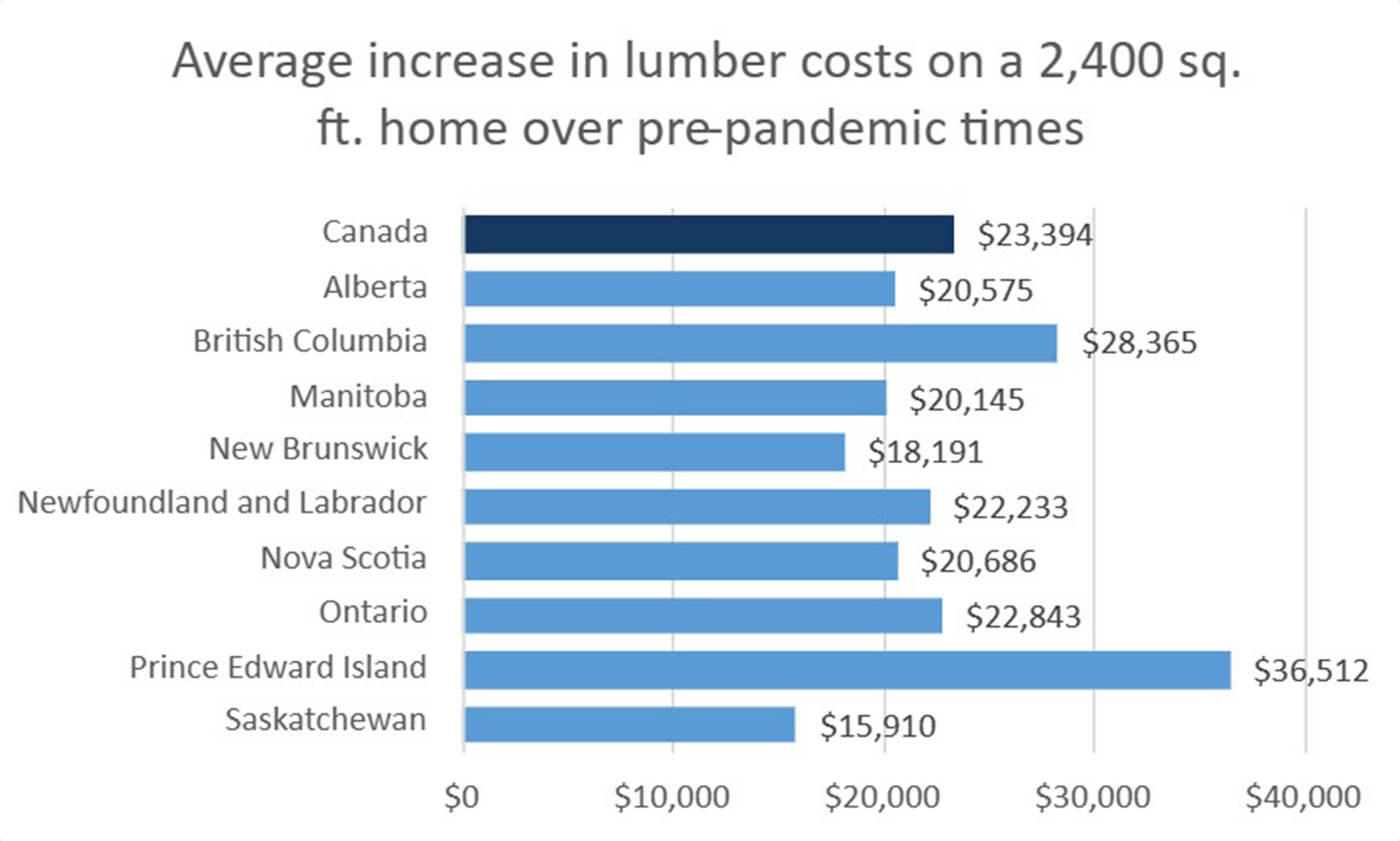

- Although lumber prices and sharp market price swings have normalized, survey respondents reported that lumber has increased the cost of construction from the onset of the pandemic on a 2,400 square foot home by a national average of $23,400. This average has remained fairly consistent over 2023.

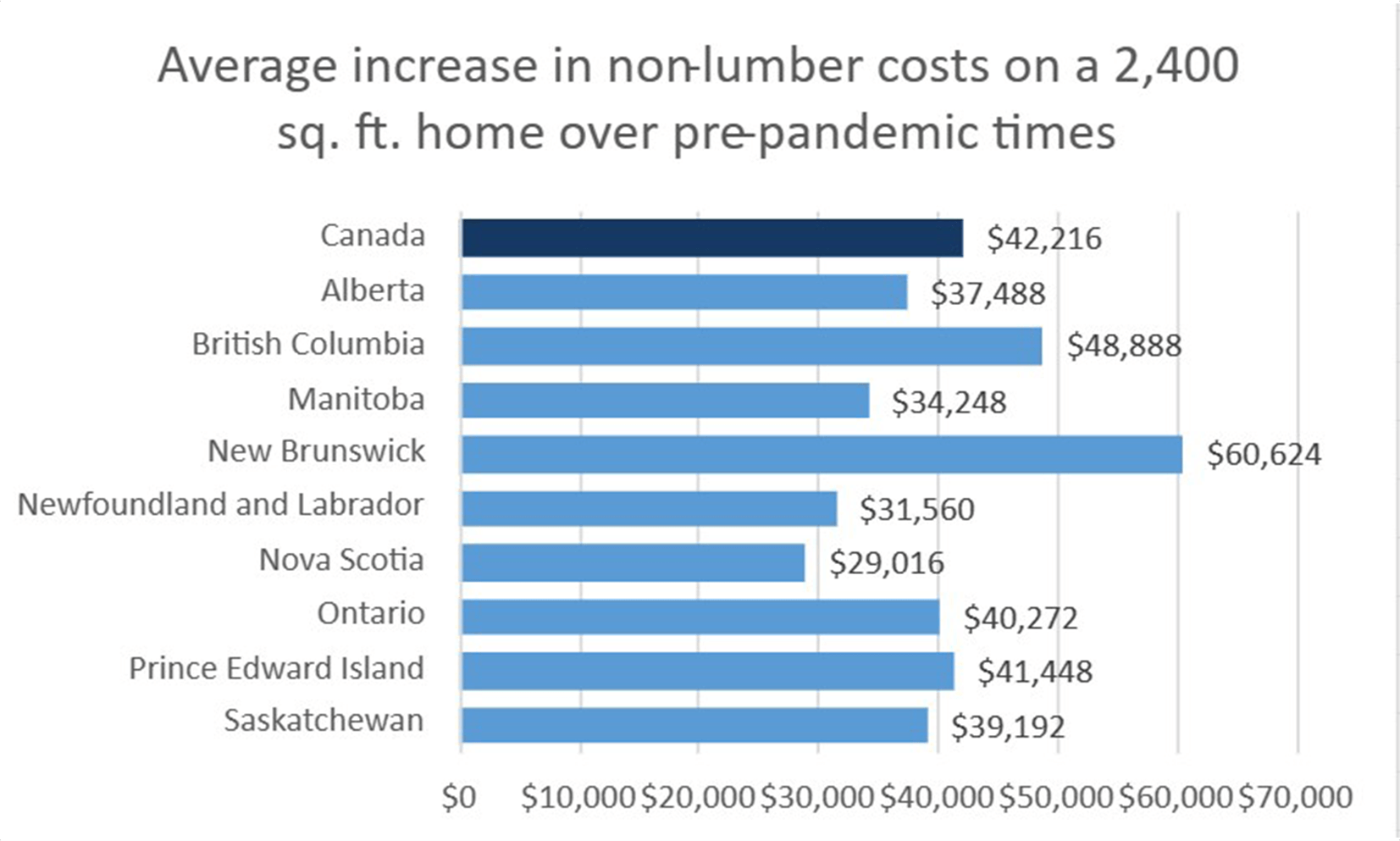

- We also continued to ask about the increase in construction costs from non-lumber building materials. 77% of respondents said that their costs have gone up by more than $20,000 since the start of the pandemic. The national average construction cost increase for a 2,400 square foot home is $42,216. This average has remained well above $40,000 throughout 2023 and is unlikely to see a broad or material decrease in the near future.

- This puts the total cost of materials for construction (lumber and other materials) compared to prior to the pandemic up over $65,500 for a 2,400 square foot home.

- The CHBA HMI for single-family builders fell to 33.9 in Q3 2023, 6 points lower from 39.9 recorded in Q2 2023. This is its second lowest reading on record, with data going back to 2021, and is slightly below 34.3 that was recorded in Q1 of 2023. Furthermore, the single-family HMI has reflected downbeat sentiment—below a value of 50—in five consecutive quarters. All three subindices for present selling conditions, expectations for selling conditions in the next six months, and sales traffic of prospective homebuyers deteriorated and contributed to the decline in the single-family HMI between the second and third quarter.

- Regionally, home builders in Ontario were most pessimistic. That said, the third quarter single family HMI readings in British Columbia and the Prairie Provinces also declined.

- The open-ended comments received from builders also follow similarly to sentiment readings. Given the difficulty in gaining mortgage approvals, sales office traffic remains low. Some builders noted that of the few well qualified buyers, there is buyer interest in existing inventory only.

- 47% of single-family HMI respondents rated the current selling conditions as Poor, which is 15 percentage points worse than Q2 2023. Relative to the previous quarter, the proportion of respondents that gave current selling conditions a Fair rating fell by over 17 percentage points to 30.7%.

- Compared to the national average of 48%, Ontario respondents were most likely to rate current conditions as Poor, at 70%.

- Only 7% of single-family builders rated sales office traffic of prospective homebuyers to be High or Very High. The proportion of builders selecting this rating has now remained in single digits for five consecutive quarters. 55% of respondents rated prospective traffic volume as Low or Very Low, which is an increase of 11 percentage points over the previous quarter but still below the 72% that gave this rating in Q4 2022—when the single-family HMI recorded its all-time low.

- Both the Prairie Provinces and the Atlantic Region were most likely to select an Average rating. Meanwhile, 79% of builders from Ontario rated traffic conditions as Low or Very Low.

- The CHBA HMI for multi-family builders was 33.6 in Q3 2023. The index fell 7.4 points from the value of 41.0 in Q2 2023 and is closely aligned with the sentiment value of 35.9 recorded a year ago in Q3 2022. Similar to the single-family index, sentiment among multi-family builders has remained downbeat for five consecutive quarters.

- Again, the breadth of downbeat sentiment was widest among builders located in Ontario.

- Comments from strictly multi-family builders suggest prospective buyers are taking longer to make decisions and overall sales traffic volumes were particularly slow through the summer months.

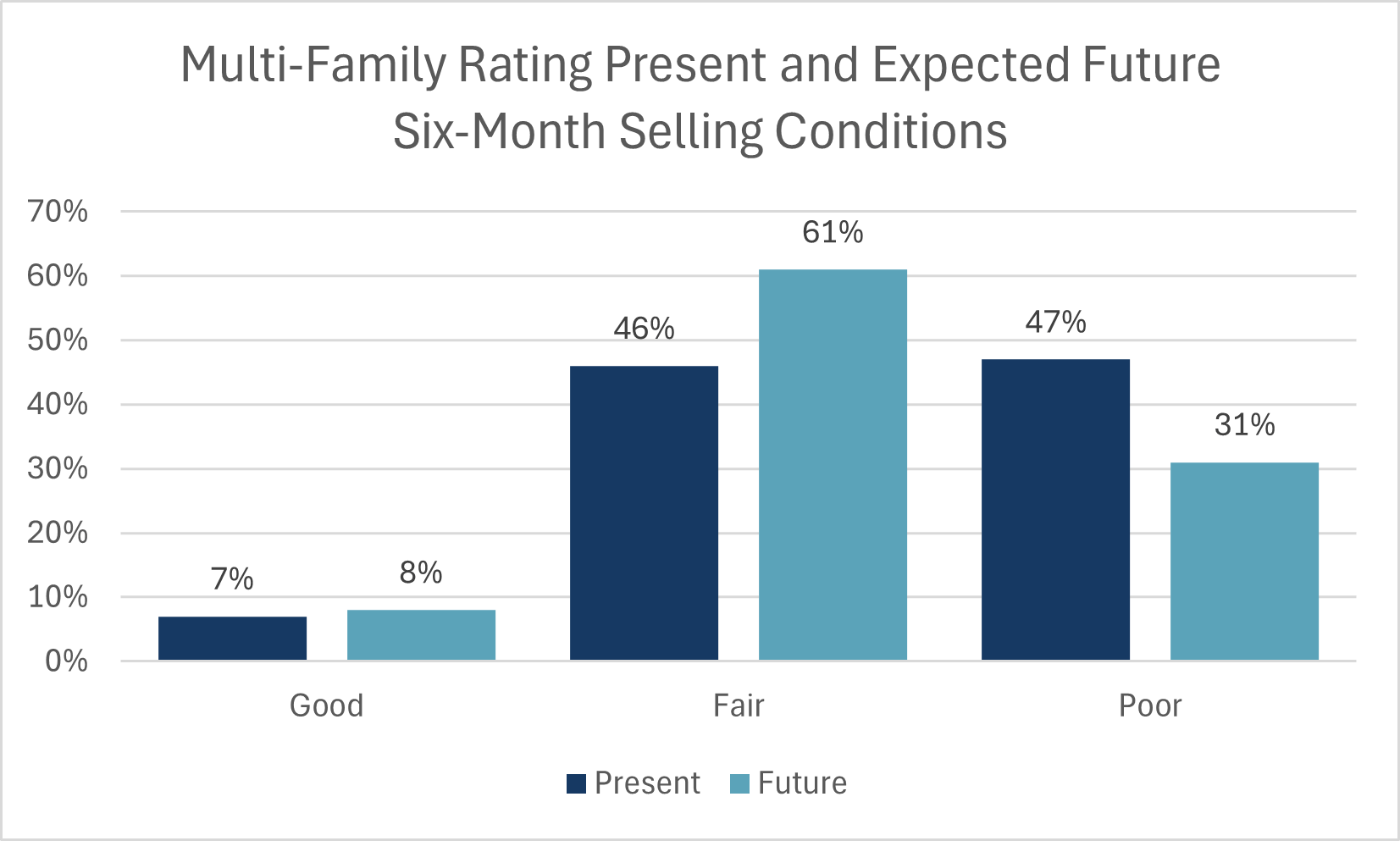

- The proportions of builder ratings for present selling conditions were closely split between Fair (45%) and Poor (44%). Both these ratings saw their proportions worsening among builders over the previous quarter, as the proportion that gave a Good rating fell 12 percentage points to 12%.

- Builders from Ontario were most likely to be downbeat, with 72% rating current selling conditions as Poor, compared to the national average of 44%. Conversely, the majority respondents in the three other regions rated current selling conditions as Fair.

- The majority (56%) of multi-family builders characterized their expectations of future selling conditions as Fair; 29% of builders gave a Poor rating. On balance, builders across all regions hold slightly more neutral views about the near future relative to current selling conditions.

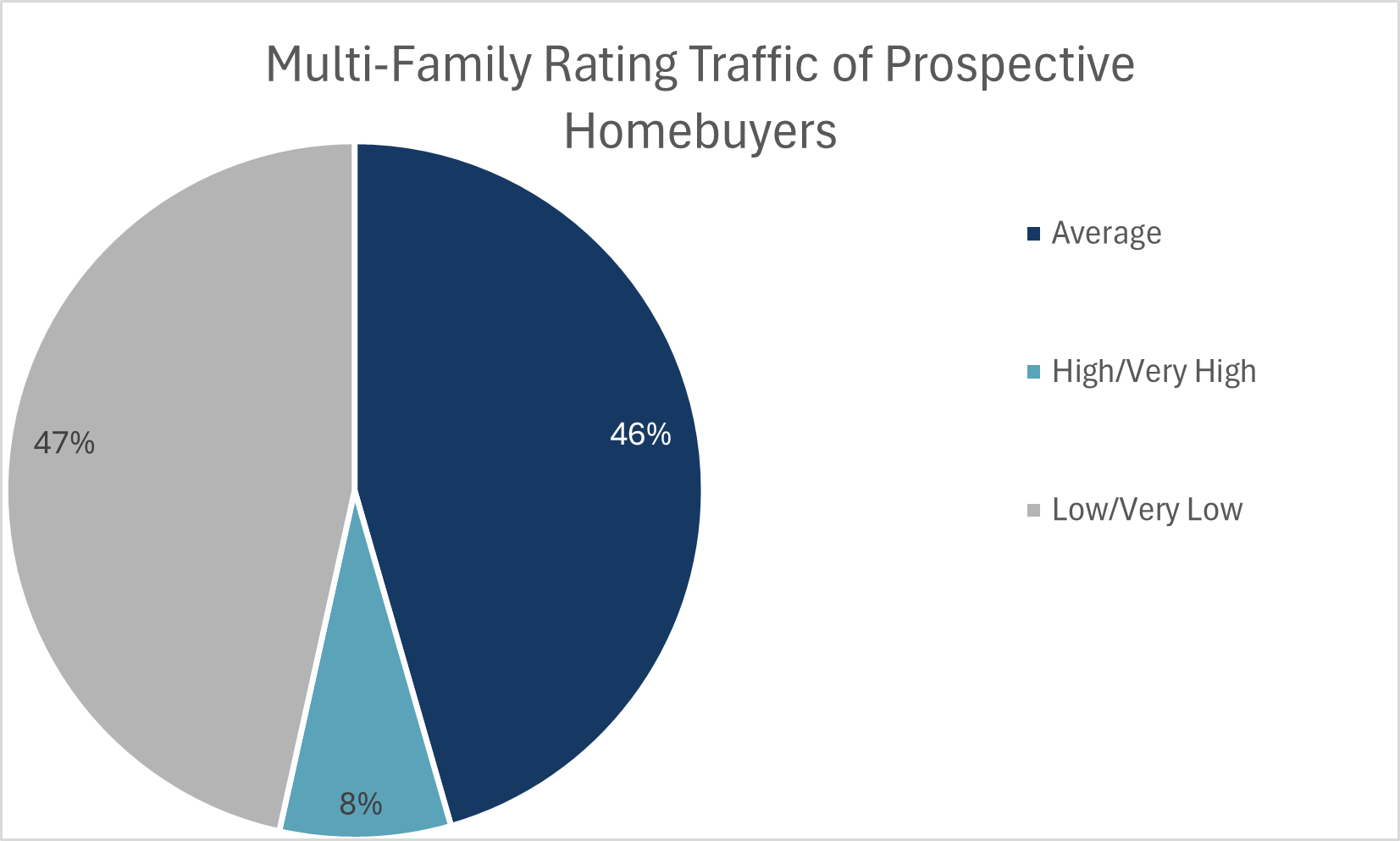

- A 58% majority of builders of multi-unit projects indicated that prospective buyer traffic was Average. Just one builder gave a sales office traffic rating of High or Very High—the lowest incidence recorded.

- In Ontario, 72% of multi-unit builders gave a Low or Very Low rating. However, builders in British Columbia were more neutral, with 75% giving an Average rating.

In addition to the survey questions directly used to calculate the HMI, CHBA includes additional “special questions” to ask the expert panel. These special questions allow CHBA to better understand what is driving change in builder sentiment and gain insights into current industry issues. The following are some of the findings from the special questions in the Q3 2023 survey:

- When asked about the impact of the cumulative increases to the Bank of Canada’s policy rate, the builders’ most common answer (40%) was that sales traffic is down and has not shown any signs of recovery. The proportion of builders stating that sales traffic was starting to return fell 11 percentage points from the previous quarter, down to 28%. Meanwhile, those reporting that sales traffic flow has gotten worse fell 9 percentage points over the Q2 2023, and is now at 21%.

- Builders were asked a follow up question about the impact of the policy rate increases in June and July on sales traffic. 39% of builders reported that these announced rate increases put an end to the springtime recovery in sales office traffic. 29% reported that sales traffic slowed even more—beyond their already low foot traffic.

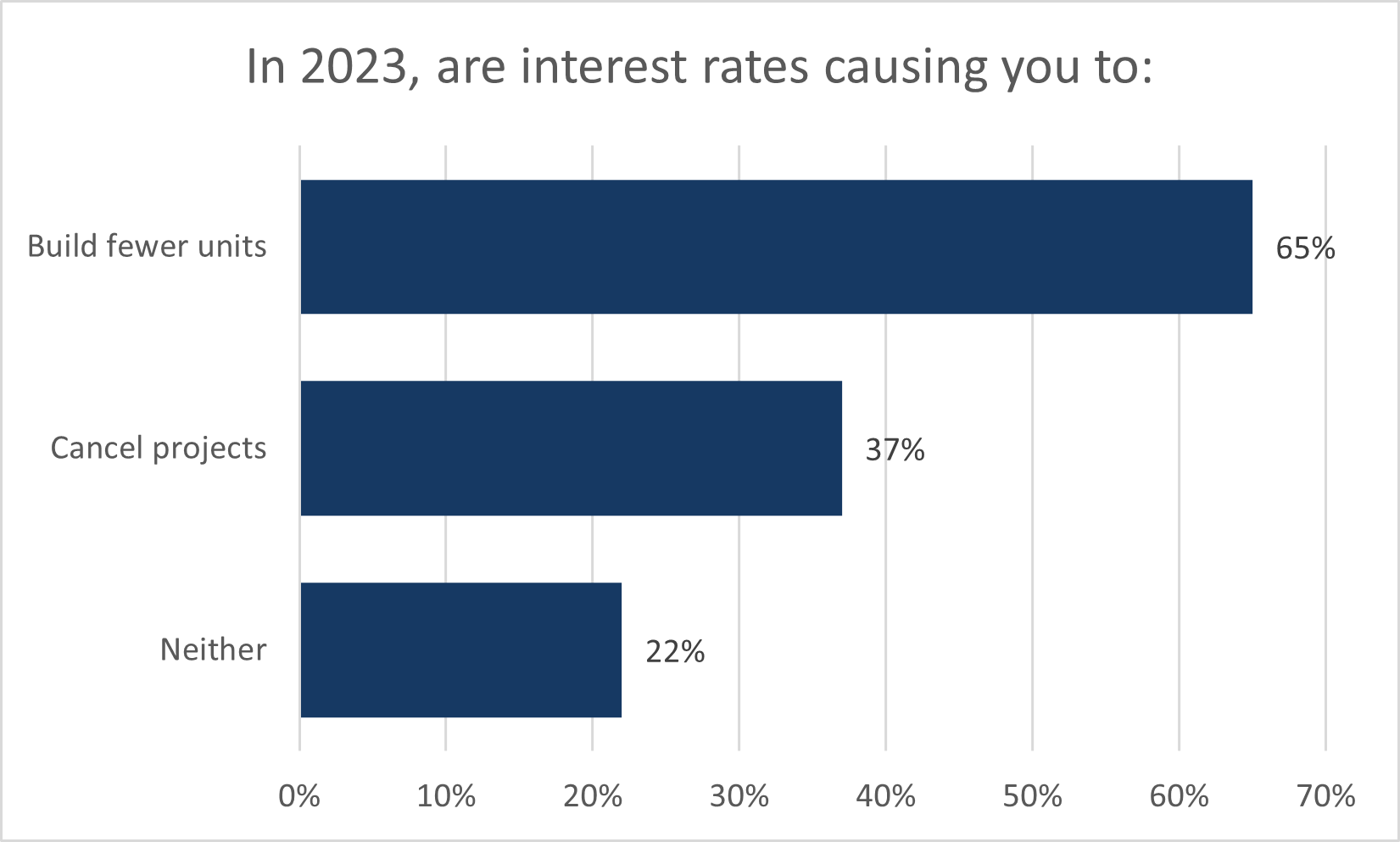

- With high interest rates reducing demand from qualified buyers and reducing builders’ access to capital, builders were asked if they have had scale back their projects or cancel them completely. 65% of the survey panel stated that interest rates are causing them to build fewer units. Most concerning was the 37% of panelists that stated they have canceled projects as a result—up from 26% of panelists in Q2 2023.

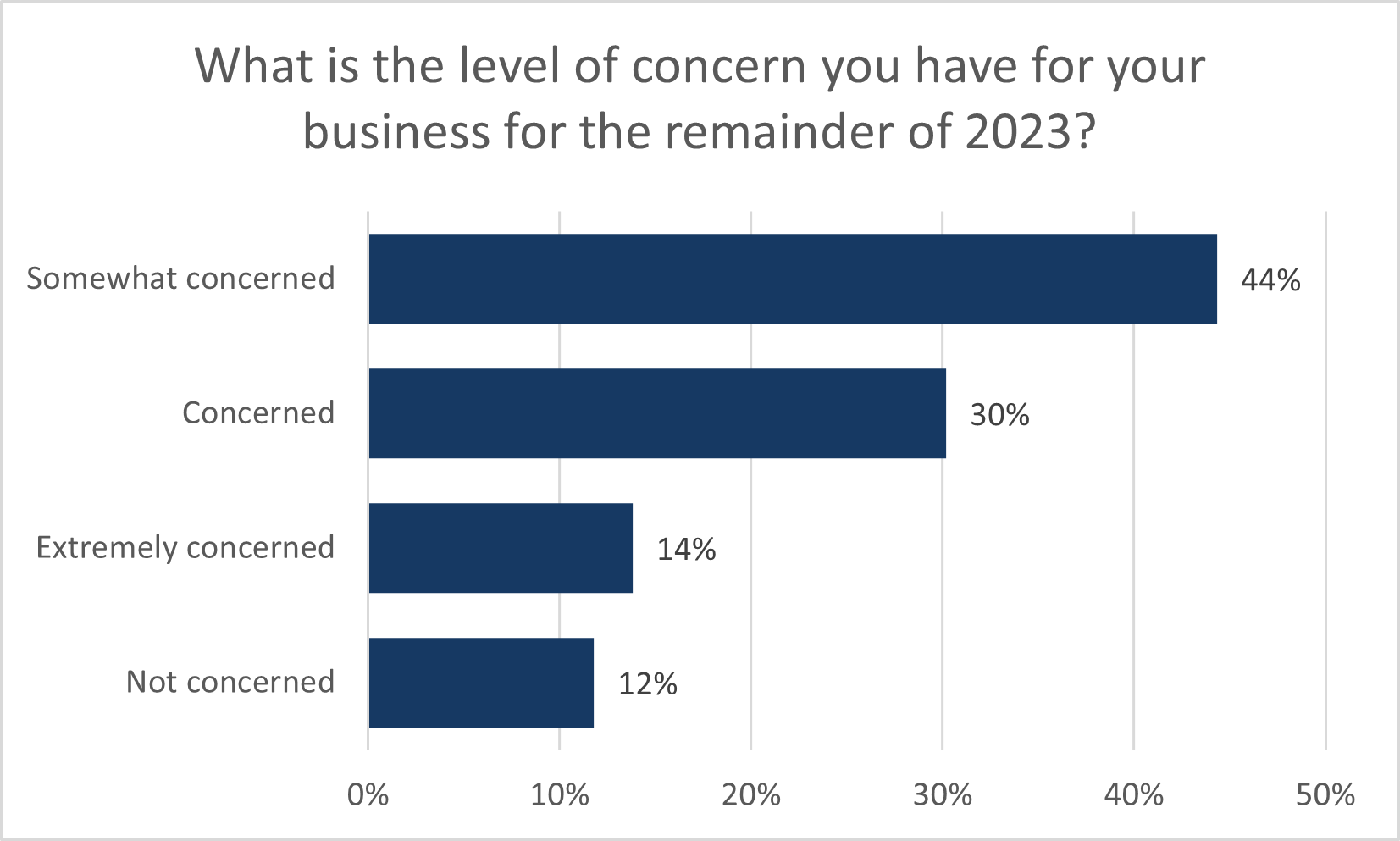

- Corresponding with the retrenchment in both HMI readings, there was an increase of 11 percentage points over the previous quarter, to 44%, in the proportion of builders reporting that they are concerned or extremely concerned about the future for their business.

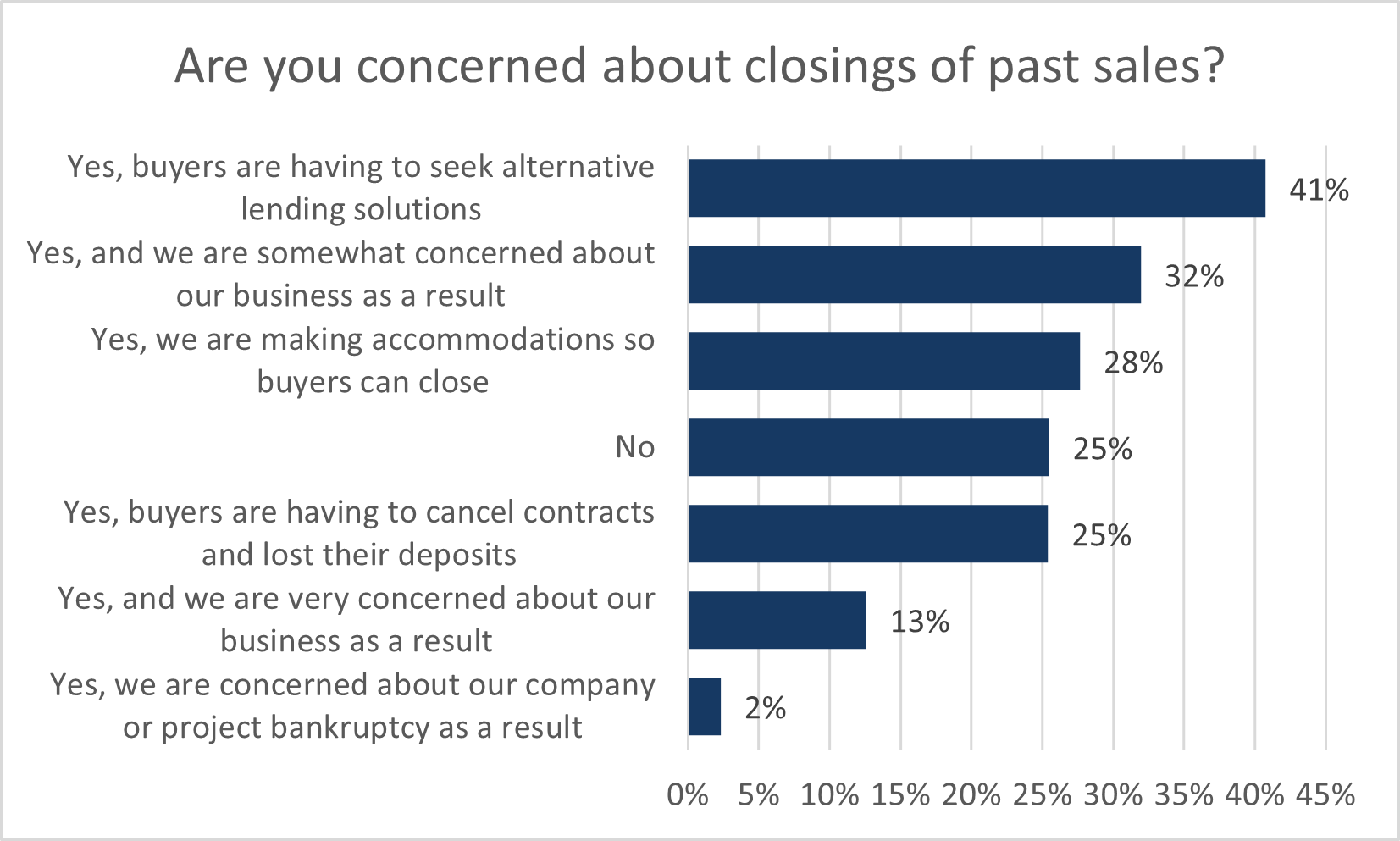

- Builders were asked to state their difficulties and level of concern surrounding closings of previous sales. 41% of panelists stated that their buyers are having to seek alternative lending solutions, down from 49% in the previous quarter. However, 32% of builders stated that distressed buyers are causing concern about their business, up from 27% in Q2 2023.

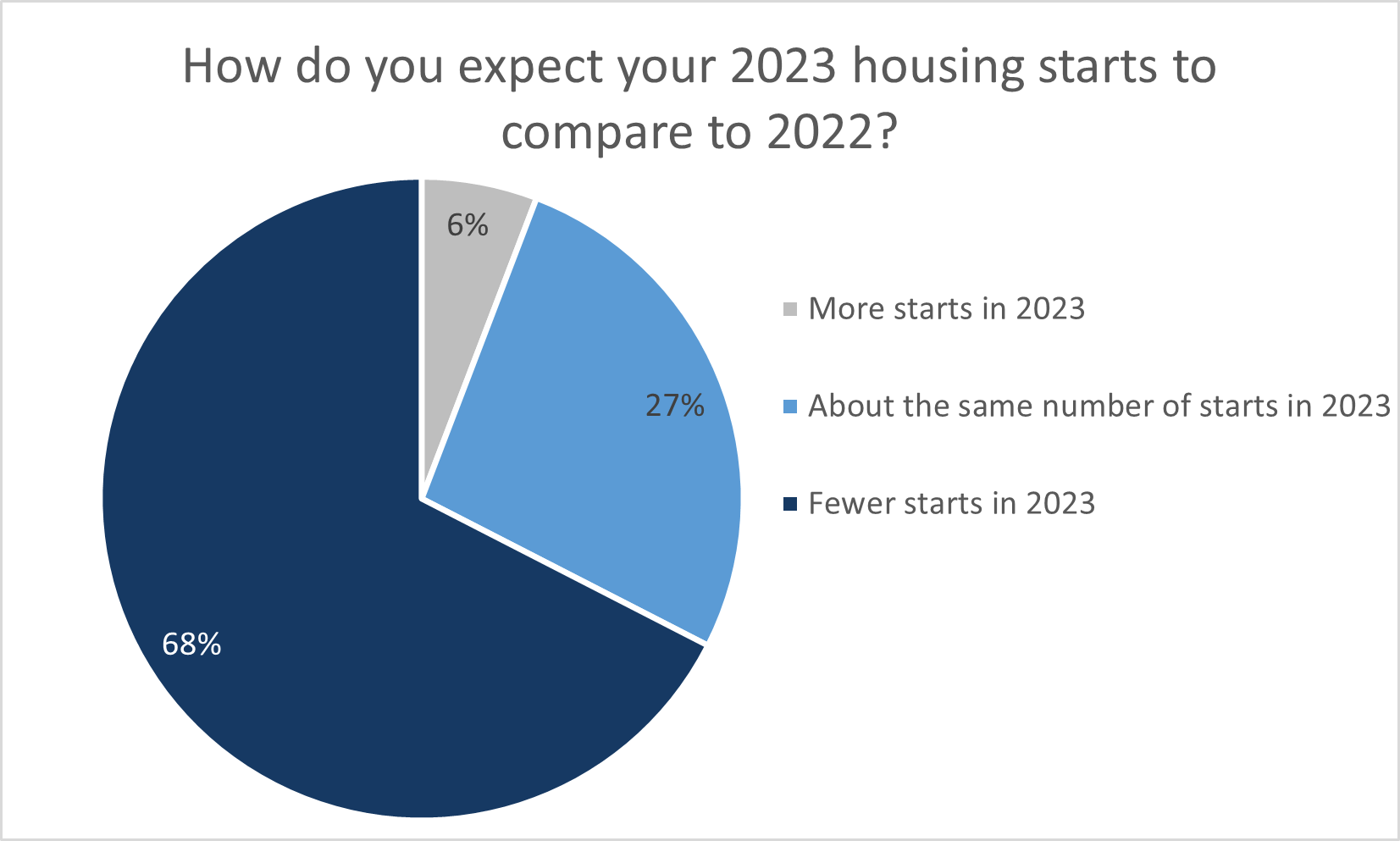

- When asked to compare their expectations for their 2023 housing starts relative to 2022, 68% of the panel stated they expect to have fewer starts this year, while just 6% stated they expect to have more starts this year than they did in 2022.

- Out of the subset of builders that expected to have fewer housing starts this year, the unweighted average percent decline was 47%— this is slightly more than the 40% average reported in the previous quarter.

- Builders were asked about their expectations for starts in 2024, which often depends on demand and conditions in the years prior. 37% of builders stated they expect to build about the same number as they will this year. Closely behind, 35% reported that they expect to start fewer homes next year.

- Comments from builders highlighted their uncertainty surrounding their expectations. Builders cited the interest rates environment as the overwhelming factor influencing their expectations of housing starts in 2024. Some builders noted that their starts will depend on presale performance, which they are not optimistic about.

- Builders were asked to select any of the most pressing factors, other than interest rates, that are causing them to build fewer homes. The question was also asked again in a hypothetical situation where interest rates and general sales conditions were better. In both instances, over half of builders reported municipal processes as a factor that is reducing their housing starts. The second most widespread factor was a lack of labour.

- Some builder comments pointed to their own cost of borrowing as a limiting factor. This issue has compounded the problem of rising construction costs and has hindered their ability to begin new projects.

- Asking about supply chain issues, builder comments suggest that supply chain issues for most supplies have improved. Yet only 12% stated that they are experiencing no delays.

- As with previous quarters, the building supplies with the highest incidence of being in serious shortage remain garage doors (13%) and appliances (11%). However, the proportion of builders reporting the shortage of these supplies as serious has shrunk from last quarter.

- Builders across the entire sample stated that supply chain or labour shortage challenges are delaying their home completions by an average of 7 weeks—the same as last quarter. 9% of builders stated they are not experiencing any delays. With supply chains issues unwinding, 31% reported construction delays of less than 4 weeks. This experience is not uniform across builders as 26% reported delays that are longer than 9 weeks.

- CHBA continued with a question posed last quarter asking about any changes to headcounts—either their own employees or their subcontractors. 42% of builders reported that they had not needed to lay off any workers and this was the most common answer—44% gave this answer last quarter. However, relative to the last quarter, there was a higher proportion of builders that reported they laid off workers without plans to rehire and a smaller proportion stating they hired more workers. According to the Labour Force Survey, the overall construction sector lost shed 58,000 in June and July and partially rebounded by 33,800 in August.

- CHBA continues to monitor factors that are adding to the cost of construction across the country. When asked to characterize their current experience with trades, 59% of builder stated trade prices are up. This was the most common answer and in line with its response rate from Q2 2023. However, this is below the 84% of builders that gave the same answer in Q3 of last year. Other common answers were that access to trades is difficult (46%) and access to trades is causing delays (40%). In both cases, these response rates were slightly above what was reported in Q2 2023 but again — less widespread than in Q3 2022.

- Nationwide, average trades wage growth since before the pandemic is 28%. This is the same average growth rate reported in both Q2 2023 and Q3 2022. Within the answers to the previous survey question, 25% of builders reported that trade prices are stable, the same proportion as last quarter.

- The cost of lumber is a significant contributor to the rise in the cost of construction relative to just prior to the pandemic. Over this time, lumber currently adds an average of $26,600 to the cost of a 2400 square foot home. 26% of builders estimated it has added over $40,000 to the units they typically build.

- Non-lumber material price increases since the onset of the pandemic continue to be both prevalent and significant. On average, non-lumber material prices have added over $45,500 to the cost of a 2400 square foot home. This average increase has relatively remained consistent since Q2 2022. Furthermore, a 51% majority of builders estimated these costs have risen by over $40,000 on their typical build.

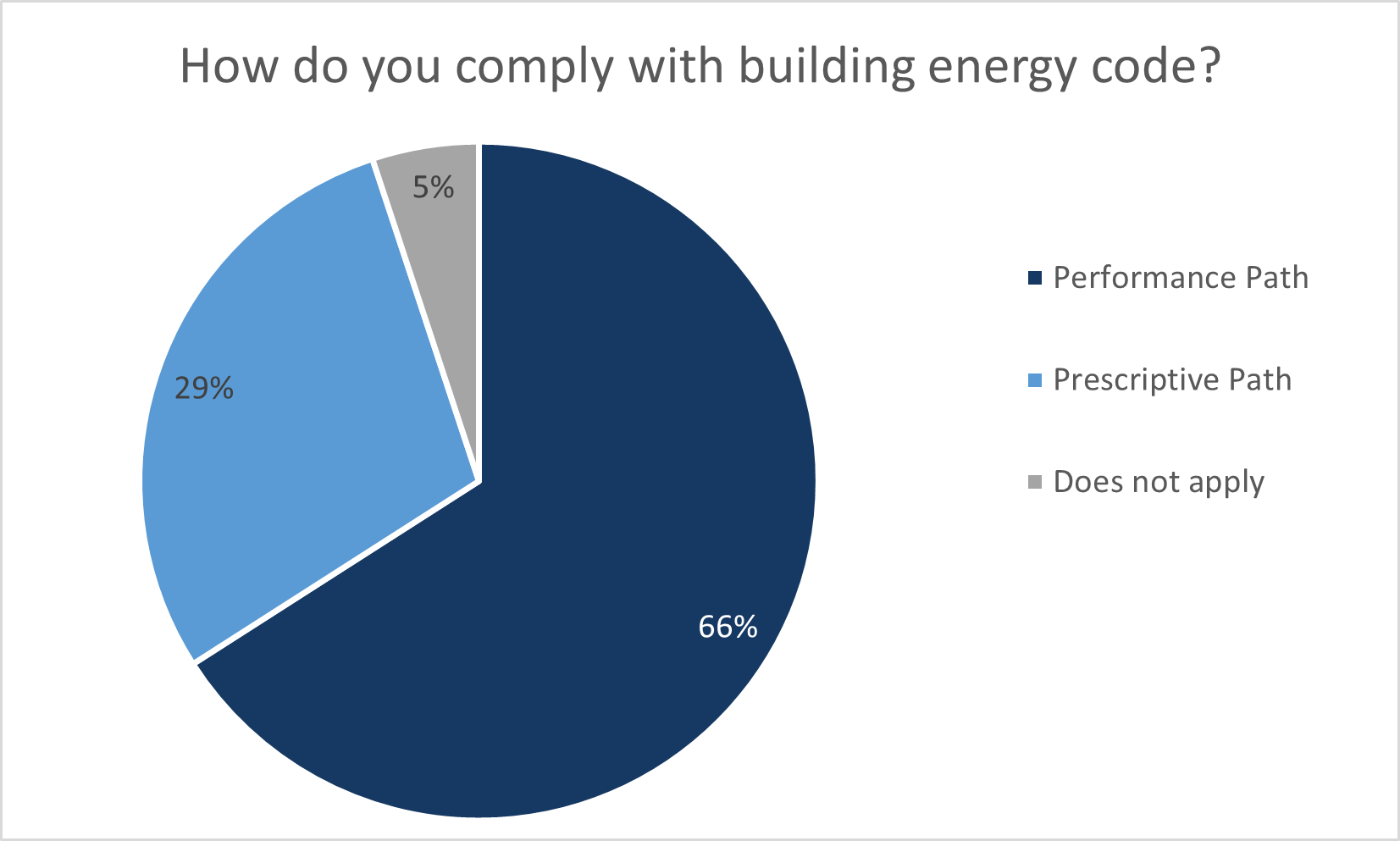

- To support CHBA’s work in building sciences and codes, builders were asked about their approach to satisfying building energy codes. 66% of builders stated they use the performance path and 29% stated they use the prescriptive path. Performance path was the more common approach even when sorting responses by builder size. Provincially, this split was driven by the performance path approach being popular among builders in western provinces. However, out of builders in and east of Manitoba, 44% stated they use the performance path and 48% use the prescriptive path.

- The CHBA HMI for single-family builders remains low at 39.9 in Q2 2023. While this represents a second consecutive increase after falling substantially between Q1 and Q4 2022, it still reflects a downbeat sentiment—well below a neutral value of 50. The single-family HMI rose 5.6 points from 34.3 in Q1 2023 but is down 25.8 points from 65.7 recorded a year ago in Q2 2022, and substantially down from its high of 89.4 in Q1 2022 before interest rates started rising.

- Although interest rates created a challenging environment to qualify for a home purchase, the Bank of Canada pausing its successive rate hikes helped improve builder sentiment with some improvement in the downtrodden market. Additionally, the index was given a boost from the traditional busy season coming out of winter.

- 48% of respondents characterized current selling conditions as Fair and 32% rated conditions as Poor.

- Regionally, half of respondents from Ontario rated current conditions as Poor. Responses from the rest of Canada were more likely to select Fair conditions.

- Looking ahead, 51%, characterized their view of future conditions as Fair. 29% of respondents reported future conditions as Poor. These proportions were similar to the previous quarter. Relative to a year ago, Q2 2022 the proportion of respondents expecting poor sales conditions rose 15 percentage points from 14%.

- All regions were most likely to rate future conditions as Fair, which was the case in the previous quarter as well. While still sensitive to interest rates, builders are assuming these conditions will persist for the foreseeable future and are adapting accordingly.

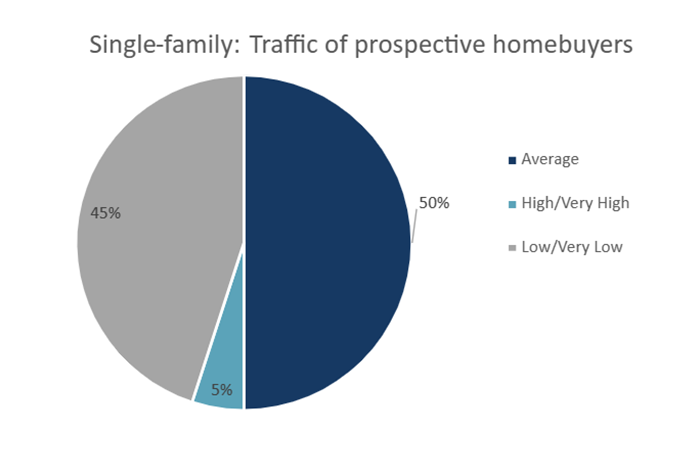

- Only 5% of respondents characterized traffic of prospective buyers as High or Very High. This proportion is the same as last quarter but far below the 24% that reported High or Very High sales traffic in Q2 2022. 45% of single-family builders gave a rating of Low or Very low. This is 8 percentage points lower than the 53% reported last quarter but 21 percentage points above the 24% that selected this rating in Q2 2022. While prospective traffic continues to return slowly, it remains definitively below conditions seen in the same quarter last year.

.png)

- The CHBA HMI for multi-family builders remained low at 41.0 in Q2 2023, though up 7.5 points from 33.5 reported in Q1 2023. Relative to the same quarter last year, the multi-family HMI is down 18.9 points from 59.9, and well below the high of 88.8 of Q1 2022 before interest rates started rising.

- 39% of multi-family builders rated current conditions as Fair, up 2 percentage points from Q1 2023 results. 37% rated conditions as Poor, which is down 9 percentage points from the previous quarter. Both the pause on interest rate hikes and spring uptick in activity likely helped improve current conditions in Q2 2023.

- The balance of responses for the expectation of future selling conditions deteriorated from the previous quarter. 47% of multi-family builders estimated their future selling conditions as Fair, this was down from 54% in Q1 2023. The proportion of respondents rating future conditions as Poor rose 9 percentage points from 25% in the previous quarter to 34%. This deterioration is no doubt a direct reflection of the increase in interest rates after the winter pause.

- The proportion of multi-family builders expecting Poor future sales conditions grew between Q1 and Q2 2023 in British Columbia, Ontario, and Prairie provinces. In Ontario, expectations were split between Fair and Poor, both at 43%.

- Prospective buyer traffic in sales offices improved slightly from Q1 2023. 43% of respondents reported Low or Very Low traffic, which was down 12 percentage points from Q1 2023. Equivalently, 43% or respondents reported Average traffic volumes.

.png)

In addition to the survey questions that help develop the HMI, CHBA includes additional “special questions” to ask the expert panel. These special questions allow us to better understand the results of the HMI and gain insights into other industry issues. The following are some of the findings from the special questions in the Q2 survey:

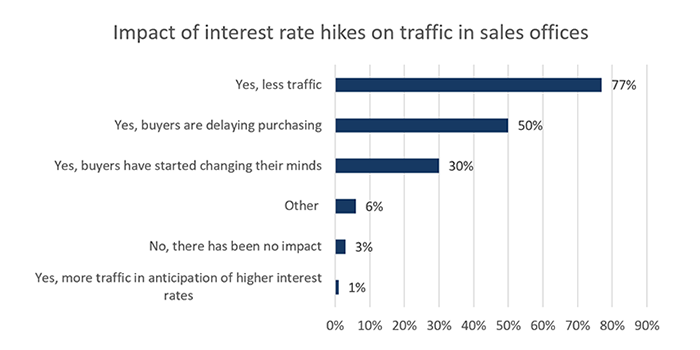

- Relative to Q1 2023, the impact rising interest rates had on traffic in sales offices was quite similar in Q2 2023. 39% of respondents noted that while they were negatively impacts, that traffic had rebounded somewhat. However, 36% stated that traffic was still down as a result from monetary tightening. Some builders commented that while traffic was average, that conversions to sales were down likely due to financing challenges. Some builders commented that traffic slowed after the rate hike in early June.

- Builders were asked about their level concern about their business for the second half of 2023, with 52% of panelists were somewhat concerned. 11% stated that they were extremely concerned about wellbeing of their business, while 14% were not concerned.

- In relation to the concern about their business, CHBA asked about recent changes to a builder’s employment levels—including subcontractors. Despite a slower market, the shortage of workers and tight labour market are reflected in the fact that 44%, builders did not need to lay off any workers. Still, 20% reported having laid off workers without plans to rehire later. Meanwhile, 17% had increased their headcount.

- As with previous quarters, we asked about the level of concern specifically over current and future closings of previous sales due to interest rates. 49% of builders stated that they have buyers that are having to seek alternative lending solutions. 34% reported that they needed to make accommodations for some buyers to close. Only, 22% reported that it was not a concern.

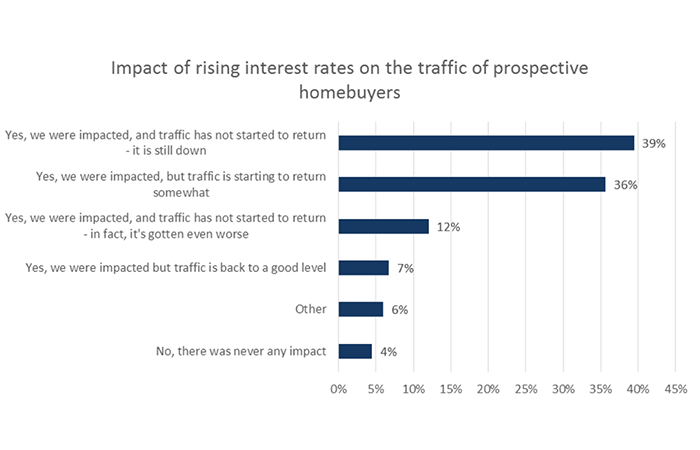

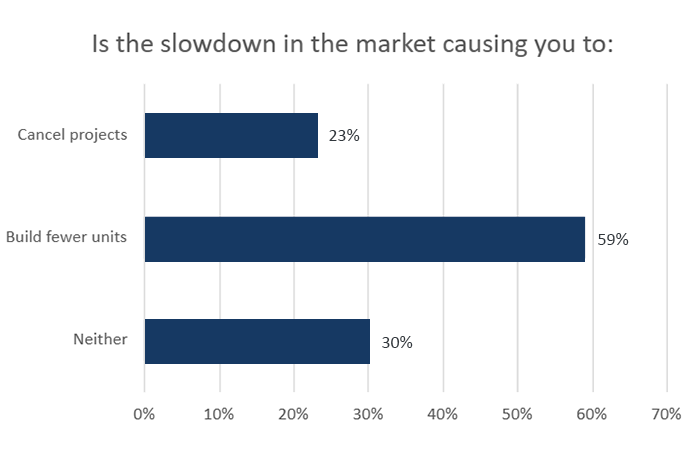

- 67% of CHBA’s expert industry panelists stated that the slowdown in the market is causing them to build fewer units, deteriorating from 59% reported in the previous two quarters. 22% said that the slowdown is causing them to cancel projects entirely (similar to the 23% of panelists in Q1 2023).

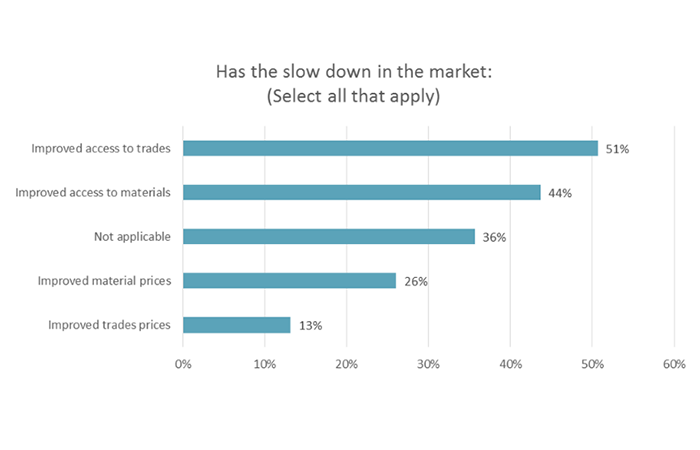

- While labour shortages remain a significant problem industry wide, the slower 2023 market has helped 47% of respondents with access to trades. In addition, 52% reported that access to building material has improved as a result as well.

- We asked builders if they expect to have the same number of housing starts this year as they did in 2022. Halfway through 2023, 59% of builders expect fewer starts, 30% expect their starts to remain about the same, and 10% said they anticipate more starts than last year.